After those 2023 bank runs there is a case for stronger rules on capital and liquidity, with the aim of restoring credibility to a timely intervention process and favouring the recovery of viable banks

Enrico Perotti is Founder and Director of the Research Platform ‘A Sustainable Future’ at UVA, Member of the ESRB Advisory Scientific Committee at European Central Bank, Professor of International Finance at University Of Amsterdam, Edoardo D. Martino is Assistant Professor of Law and Finance at University Of Amsterdam

Cross-posted from VoxEU

Drawing: James Gillray, 1797

The rapid escalation in uninsured deposit runs in March 2023 prompted calls for stronger ex-ante prudential measures, such as higher capital and liquidity norms, as well as an EU proposal aimed at increasing the use of the resolution process. This column reviews specific lessons from the 2023 bank runs and make a case for stronger Pillar II power for contingent measures on capital and liquidity, with the aim of restoring credibility to a timely intervention process and favouring the recovery of viable banks.

The rapid escalation in uninsured deposit runs in March 2023 led to bailouts and chaotic resolution, showing a clear limit to current prudential norms.

Since then, some reform proposals have focused on stronger ex-ante prudential measures, such as higher capital and liquidity norms (Admati et al. 2023), while others have suggested an expansion of public insurance coverage to corporate deposits (Heider et al. 2023), a view largely adopted in a current EU reform proposal aimed at increasing the use of the EU resolution process (Dewatripont et al. 2023).

In our view, higher buffers would be most effective but are likely to be resisted as costly, while extending insurance to corporate accounts has a high fiscal cost and would lead to more risk creation. In a new CEPR Policy Insight (Perotti and Martino 2024), we review specific lessons from the 2023 bank runs and make a case for stronger Pillar II power for contingent measures on capital and liquidity. Our aim is to restore credibility to a timely intervention process, to favour the recovery of viable banks.

The intervention gap

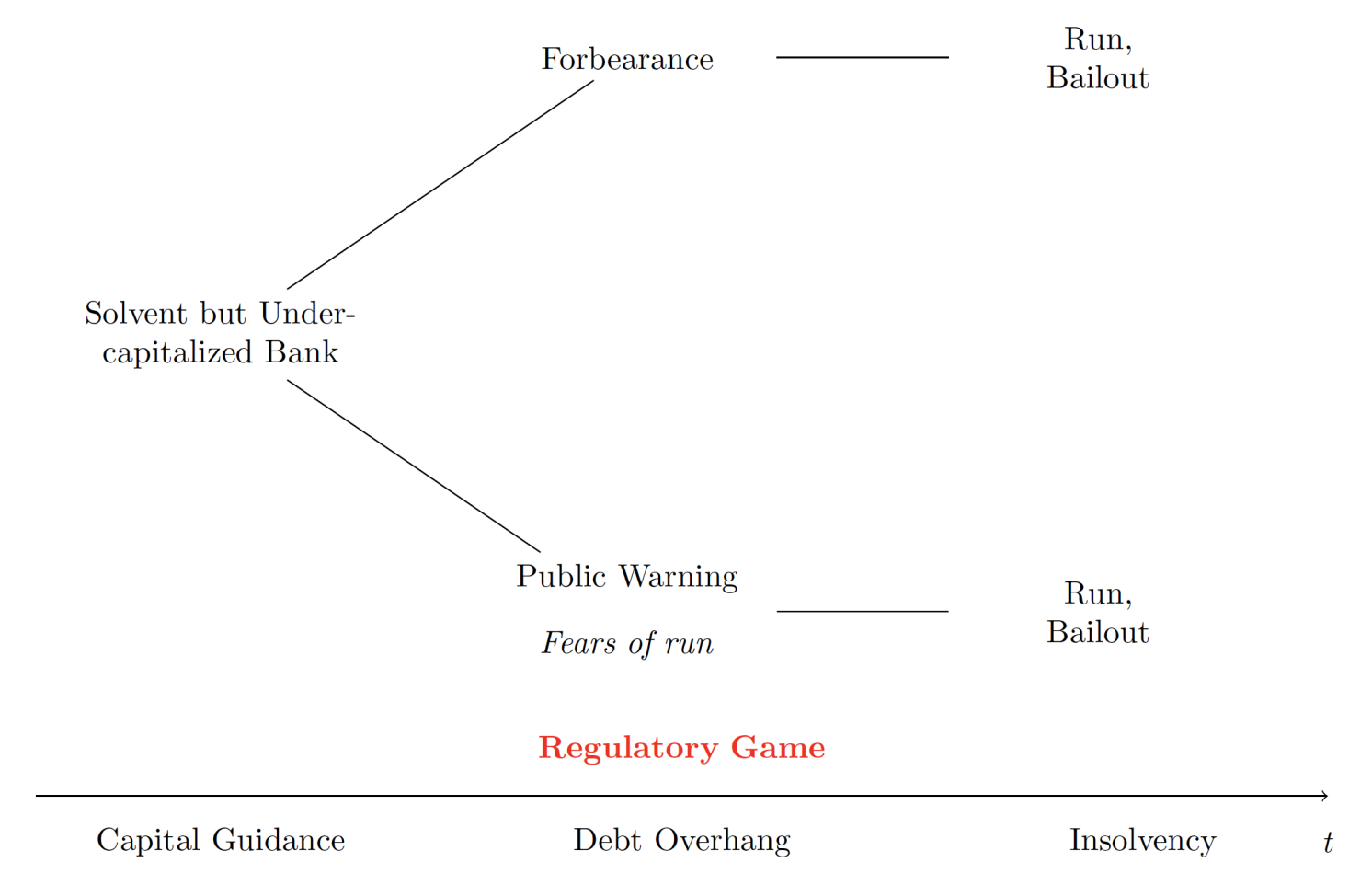

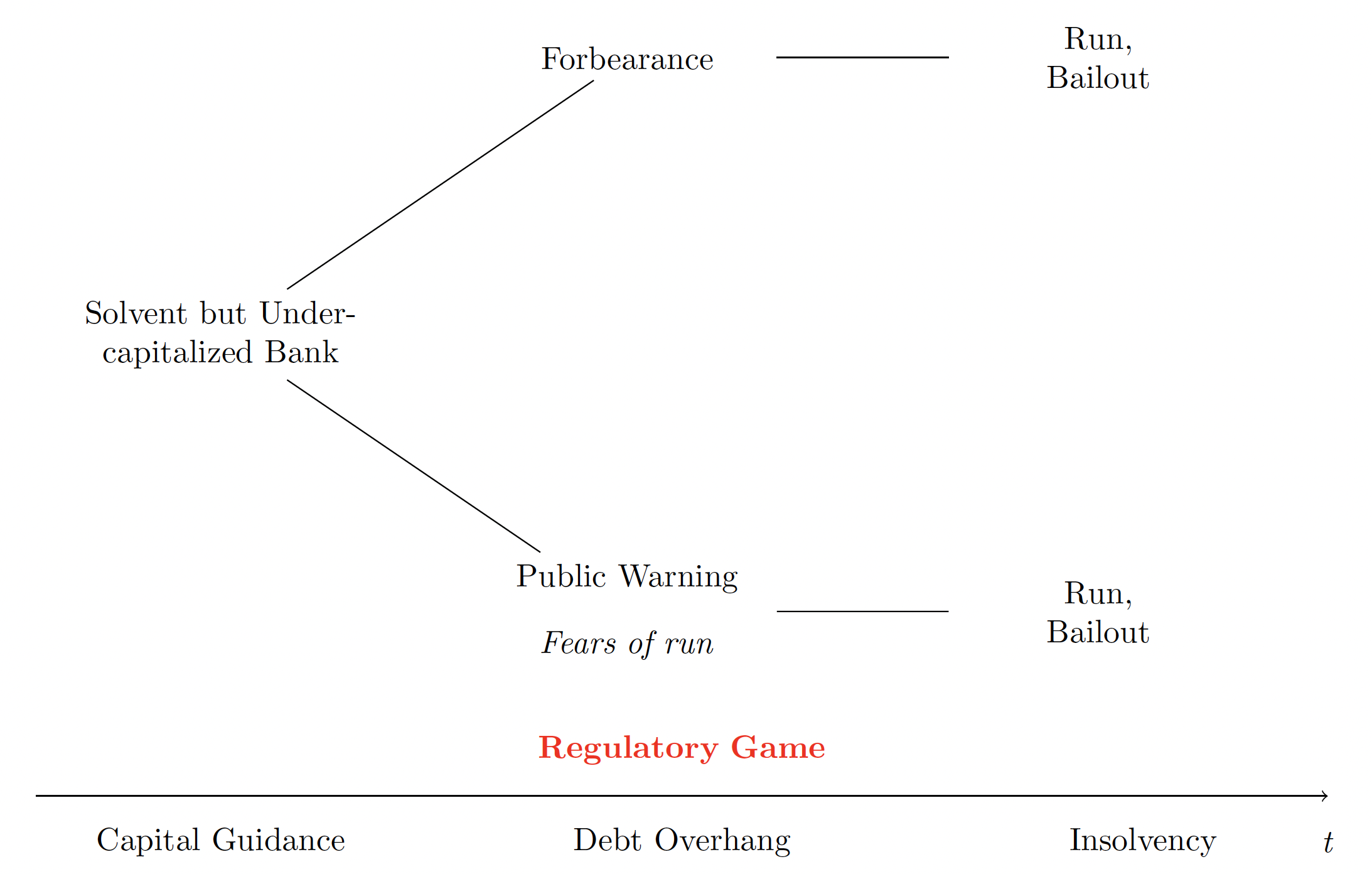

The 2023 experience showed how supervisors failed to take concrete steps as potentially viable banks slipped towards insolvency, hampered by concerns about triggering uncontainable runs (Cecchetti and Schoenholtz 2023). Such regulatory forbearance buys time but leads to a steady value deterioration and increased losses. Thus, the current regulatory framework has a major blind spot: once a bank becomes undercapitalised, there are no credible tools to promote recovery or contain run incentives.

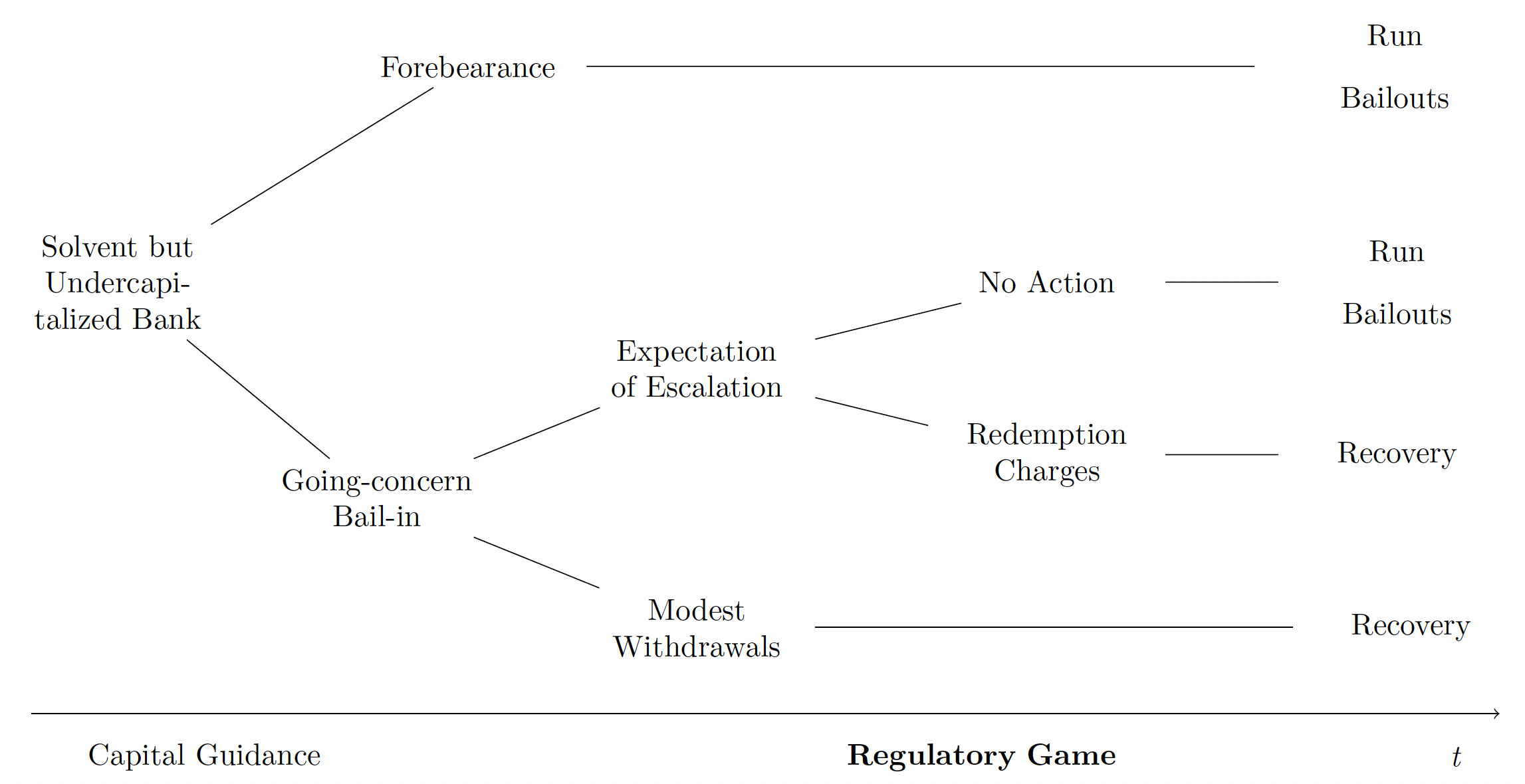

In this intervention gap, supervisors are confronted with two sub-optimal options. The available preventive tools (mostly, a suspension of payout) offer little immediate relief while sending a signal about bank losses, thus triggering a run. This gives rise to a ‘capital forbearance’ game (Martynova et al. 2022), where lack of credible measure leads share- holders to gamble along with regulators for a lucky recovery. Prolonged forbearance worsens capital deterioration, leading to rising fiscal losses (Figure 1).

Figure 1 The Intervention gap and regulatory game

Contingent measures: Favouring recovery over resolution

We propose concrete preventive measures to fill the intervention gap. Specifically, we propose an early distress measure of capital and an acute distress measure of liquidity.

On the capital side, we propose strengthening the Pillar II mandate on the going concern loss-absorption of contingent convertible debt. A timely reduction in leverage would grant immediate breathing space and remove run incentives, ensuring a going concern recovery with no bailout, as in the case of Credit Suisee AT1 conversion (Perotti 2023b). As illustrated in Table 1, we call for a large CoCo AT1 buffer to be converted at a high capital threshold along the Swiss regulatory model (i.e. at 7.00% rather than 5.125%), activated by a supervisory assessment that a bank is undercapitalised but potentially viable.

However, such a decisive going concern conversion would only be credible in combination with credible tools to contain any escalation of outflows. As in Perotti (2023a), we propose throwing some sand in the wheel by discouraging outflows from escalating into self-fulfilling runs. Redemption fees similar to the norms the SEC recently enacted for US money market funds (MMFs) would be directly triggered by high daily outflows of uninsured deposits so as to act as automatic stabilisers. 1 These would eliminate the one-sided incentive to respond to outflows by withdrawing, directly reducing run incentives. Charges imposed on a timely basis would also break expectations of further withdrawals by others, avoiding escalation driven by fear of dilution rather than solvency concerns or liquidity needs. They may be seen as a Pigouvian tax on withdrawals with no liquidity needs, and would force withdrawing depositors to internalise the liquidity externality they cause (Perotti and Suarez 2011).

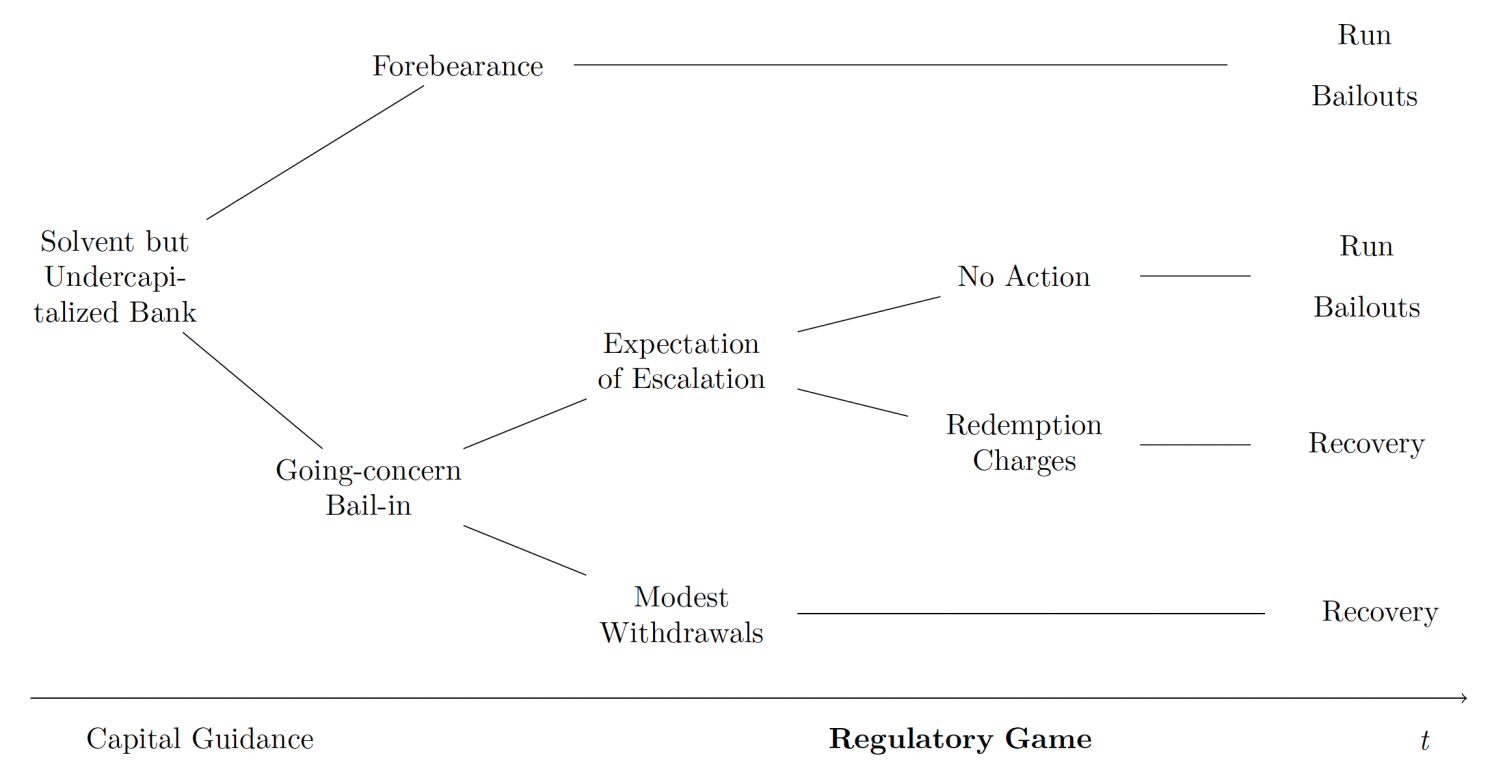

A reliable stabilising tool that discourages sudden outflows would reduce concerns over public measures leading to an inevitable escalation. Removing the threat of a run raises the credibility of recapitalisation measures and reduces forbearance incentives. Both measures represent a form of preventive partial bail-in to preserve going concern value for solvent intermediaries. Figure 2 depicts the key nodes for a solvent but undercapitalised bank when both capital and liquidity recovery measures are in place.

Figure 2 Interim interventions favouring recovery

Regulatory design and calibration

If a bank is insolvent, a prompt resolution process is the sole legitimate policy. Capital conversion measures should legitimately be targeted at banks deemed undercapitalised but potentially solvent, to prompt their recovery. However, ascertaining bank solvency is more complex than estimating book equity. A bank that has suffered losses may be viable if it has a sustainable business model and the downside risk of further losses is limited. Many banks are currently undercapitalised by losses on safe asset holdings, but higher lending rates envision better future returns (Jiang et al. 2023). These banks may be at the mercy of run expectations, as the value of its deposit franchise and some of its assets may not be realised quickly. Such banks are natural candidates for contingent measures aiming at recovery.

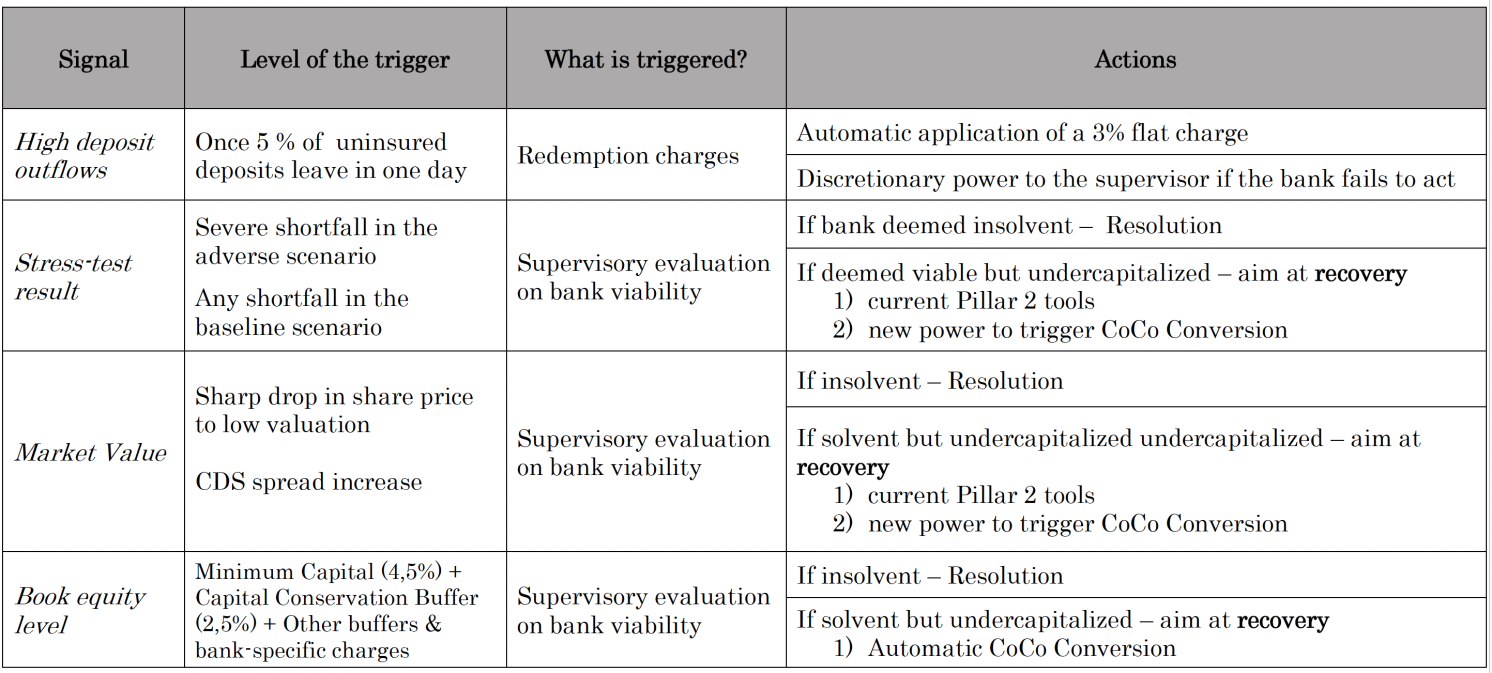

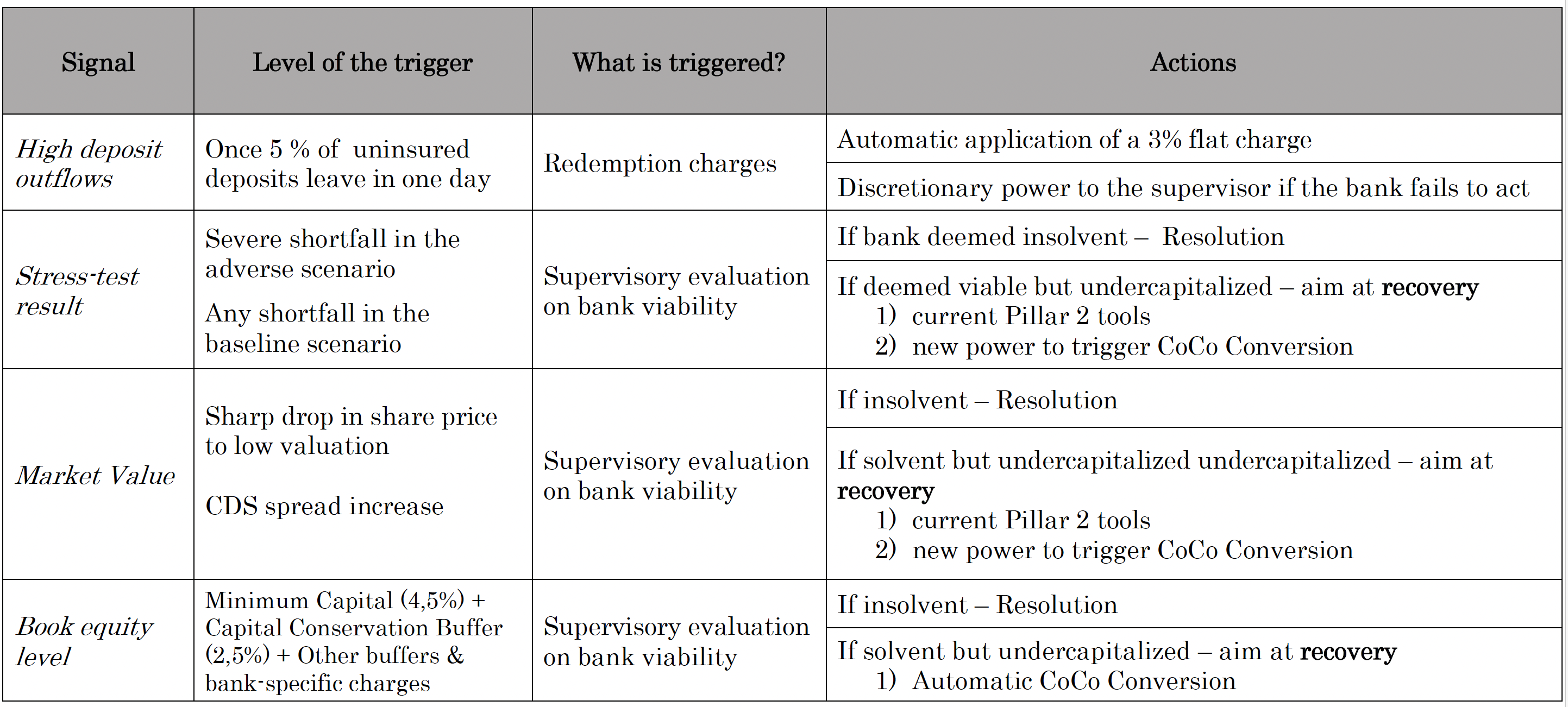

Table 1 The activation of interim measures

The activation of interim (pre-resolution) measures should, as much as possible, be automatic and based on verifiable signals. We focus on quantifiable indicators that can be considered legitimate triggers for conversion or bail-in measures. Table 1 summarises these signals, their possible trigger levels, and the effect on the activation of recovery measures.

Unlike capital conversion, redemption charges should not be seen as a supervisory action, but rather as tools of proper market functioning. They serve as automatic stabilisers maintaining access to funds at times of illiquidity while containing an unnecessary escalation. Charges would be triggered once daily outflows of uninsured deposits passes a threshold (say, 5%). Banks would need to disclose daily flows to supervisors, who would retain the right of activation if the bank fails to do so.

A legitimate trigger for going concern capital bail-in is more delicate to design and calibrate, as it is justified only for potentially solvent banks. In our Policy Insight, we consider three distinct signals as triggers for going-concern conversion and, more generally, related Pillar II recovery measures. Stress test outcomes and market value metrics offer timely signals. Market values may be valuable early signals of value deterioration. Although prone to distortion (Sundaresan and Wang 2015), they could be used as a first-level trigger for further supervisory action, such as stress testing.

Stress-test shortfalls and market value metrics must prompt a supervisory assessment of bank viability. A negative assessment implies the immediate resolution of the bank; a positive assessment of the bank’s viability would activate supervisory powers to prompt recovery by capital conversion and other current Pillar II measures, including payout restrictions. The Credit Suisse experience of delayed activation calls for a clear legal authority to be assigned to Pillar II authorities to trigger CoCo conversion.

Finally, we consider book equity triggers. This signal is notionally appropriate, but in practice opaque and prone to manipulation. Therefore, it may fail to signal deterioration early enough and should fulfil only a complementary role, given its relevance for capital regulation. We propose retaining an automatic trigger based on book equity in line with current practice, provided its trigger is raised considerably to ensure that conversion would support the recovery of a solvent but undercapitalised bank. The regulatory trigger should be set at at least 7% of book equity. This is equal to the core equity requirement of 4.5% plus the capital conservation buffer of 2.5%. If the bank is systemically important or is deemed particularly risky, the AT1 bonds should carry a correspondingly higher conversion threshold at issuance.

Conclusion

We propose a strengthened regime of contingent intervention aimed at avoiding unnecessary default (‘in loco bancaruptae’) and give a chance to recovery for banks deemed to be in principle viable. The contingent measures involve targeting run incentives by pre-emptive conversion or partial bail-in of capital investors or uninsured depositors. We argue that to overcome the regulatory gap, for a going concern recapitalisation to be credible and actionable, it needs to be complemented by measures containing run incentives. A credible threat of conversion can pressure shareholders for timely corrective actions and improve the chances of bank recovery over default. Contingent measures complement ex-ante capital and liquidity buffers, and would rely less on book equity measures. They are vastly preferable to an expansion of deposit insurance for uninsured corporate deposits, which would lead to greater moral hazard and risk creation (Perotti 2023a, Martino and Vos 2023).

Ultimately, bank run incentives can be contained by much higher buffers, just as flooding can be contained by higher dikes and levees. Yet, for flood control it is also useful to store sandbags as precautionary contingent measures against unexpectedly high water levels. 2 In contrast, relying on deposit insurance may be seen as passively accepting the inevitable breach of the levees and redirecting the flooding to a larger area.

Thanks to many generous donors BRAVE NEW EUROPE will be able to continue its work for the rest of 2024 in a reduced form. What we need is a long term solution. So please consider making a monthly recurring donation. It need not be a vast amount as it accumulates in the course of the year. To donate please go HERE.

Be the first to comment