It all sounds like the 1930s not the roaring 20s.

Michael Roberts is an Economist in the City of London and a prolific blogger

Cross-posted from Michael Roberts’ blog

Photo: Wikipedia

In the last few days, the leading central bankers of the advanced capitalist economies met at the annual jamboree in Jackson Hole, Wyoming, US. Jackson Hole is a very upmarket ski and mountain resort where average household income is near $100,000 a year. So it is a very appropriate place for central bankers to meet and discuss the world’s economic problems and, in particular, the cost of living crisis and the fall in real incomes that has hit the rest of us across the globe.

The meeting was kicked off by an eagerly awaited address from Fed Chair Jay Powell on the central bank’s progress on getting inflation down. Financial investors were hoping for a clear statement that the Fed would stop hiking its policy rate now that inflation was falling. But that hope was dashed as Powell made it clear that inflation was “still too high” and while the rate of inflation was falling, it would be necessary to keep the policy rate high for some time i.e. well into 2025, and it may be necessary to raise it again before the year is out.

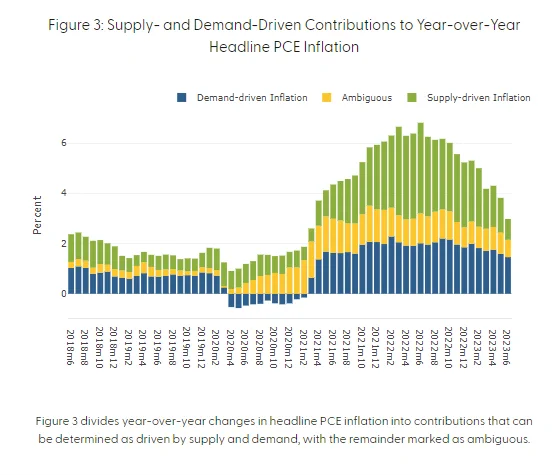

Powell sort of admitted for the first time that inflation had spiked to levels not seen since the 1980s because of “supply distortions”, but continued to claim that it was a combination of ‘excessive demand’ and weak supply. That was stating the obvious in the sense that it takes two to dance i.e. if the supply of commodities is lower than demand for them, then prices would rise and vice versa. But the question is: which was the leading the dance, supply or demand?

The evidence is now overwhelming that it was the latter, with rocketing energy and food prices caused by the collapse of supply chains internationally, very low productivity growth and the loss of skilled workers after the pandemic.

That meant that the huge rise in interest rates, supposedly to bring down ‘excessive demand’ by reducing borrowing to spend or invest, would have limited effect on inflation rates. And so it has proved. While the ‘headline’ inflation rate has fallen globally as energy and food price inflation subsided (at least for now), ‘core’ inflation rates have remained stubbornly high.

Central banks and mainstream economists have not been able to answer why that is. Nevertheless, they have ploughed on with what they do: namely to raise interest rates and reduce money supply in order to bring the inflation rate down to some arbitrary target of 2% a year. As Powell put it at Jackson Hole: “although further unwinding of pandemic-related distortions should continue to put some downward pressure on inflation, restrictive monetary policy will likely play an increasingly important role.”

So, despite the hit to people’s living standards; despite the monstrous rise in mortgage borrowing costs; despite small banks and businesses going under, the Fed will continue to keep interest rates at record highs to ‘control inflation’, which is only coming down because the supply issues in energy and food have abated.

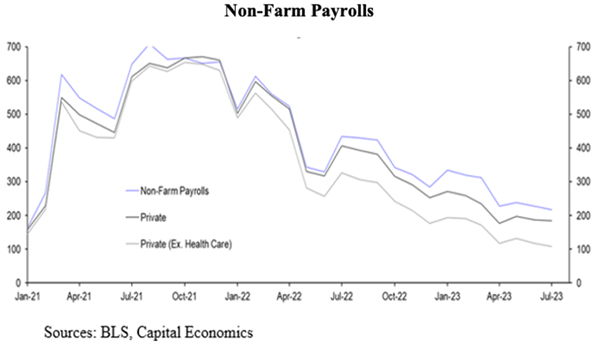

What high interest rates are doing is damaging the productive sectors of the economy, but not really affecting inflation. Powell admitted that “getting inflation sustainably back down to 2 percent is expected to require a period of below-trend economic growth as well as some softening in labor market conditions.” Indeed. The Fed and the the mainstream economists continue to proclaim how low unemployment is, not only in the US but in most of the other advanced economies.

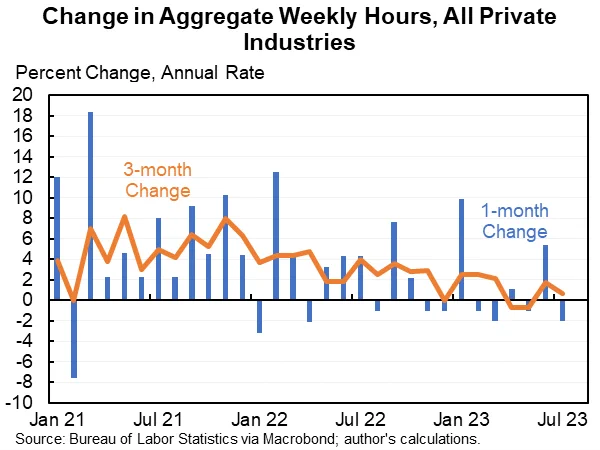

So there is nothing to worry about – a ‘soft landing’ for the economy is probable, even if unemployment ticks up a bit. But Powell had to recognised that “payroll job growth has slowed significantly. Total hours worked has been flat over the past six months, and the average workweek has declined to the lower end of its pre-pandemic range”.

He called this “a gradual normalization in labor market conditions“. More likely, it is another sign that the US economic ship, far from pulling into a safe economic harbour, is showing signs of listing with a hole appearing below the water line.

Actually, the ‘strong’ jobs data has been quietly revised down by the official statisticians just this month, with a reduction of over 350k jobs in the year to March. Moreover, a further downward revision is expected.

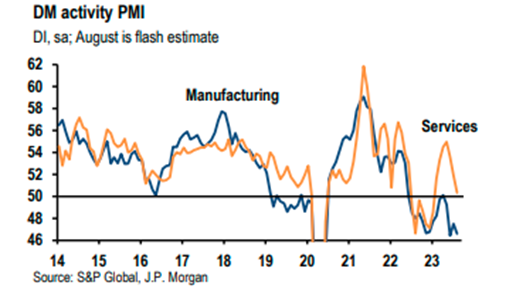

Anyway, employment is a lagging indicator of activity in a capitalist economy. The lead indicator starts with profits, then investment and production, then employment and consumer spending. Corporate profits and corporate profit margins have already been falling. Investment growth is slowing. And manufacturing is in recession. A high frequency indicator of economic activity, the JPM global PMI, is indicating that the manufacturing sector is contracting (any score below 50) and the services sector is now virtually doing so, both globally and in the US.

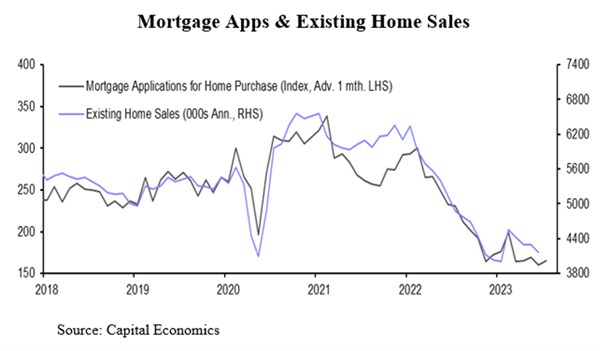

As for the consumer, housing markets in the major economies are dead in the water.

But no worries. Powell remarked: “While nominal wage growth must ultimately slow to a rate that is consistent with 2 percent inflation, what matters for households is real wage growth. Even as nominal wage growth has slowed, real wage growth has been increasing as inflation has fallen.” That sounds good, but he did not say that since the end of the pandemic, consumer prices have risen by 17-19% and wage rises have been well short of that. And these higher price levels are here to stay forever, so wages will have to rise a lot more to recoup the losses in real incomes over the last two years.

While the economic ship is showing signs of leakage, up on the bridge, Captain Powell says that he is “navigating by the stars under cloudy skies.” In other words, he does not know if the ship will make port before sinking. Indeed, “there is always uncertainty about the precise level of monetary policy restraint.” He went on: “These uncertainties, both old and new, complicate our task of balancing the risk of tightening monetary policy too much against the risk of tightening too little. Doing too little could allow above-target inflation to become entrenched and ultimately require monetary policy to wring more persistent inflation from the economy at a high cost to employment. Doing too much could also do unnecessary harm to the economy.”

Indeed, ‘managing’ an anarchic capitalist economy is not easy – indeed impossible. Even worse, the navigation guide that Powell and mainstream economics are trying to use is the so-called ‘neutral policy rate’ that supposedly tells economists when demand and supply; or more accurately, aggregate savings and investment, are in balance. But this r*, as it named, is a nonsense concept that comes from the neoclassical equilibrium economics of Kurt Wicksell. Many studies have shown up the myth of this theory. It’s less an astronomic navigation tool and more the astrology of the zodiac. Nevertheless, Powell referred to this ‘natural rate of interest’ theory as his policy foundation, but then dissed it by saying “we cannot identify with certainty the neutral rate of interest, and that assessment is further complicated by uncertainty about the duration of the lags with which monetary tightening affects economic activity and especially inflation.” Yes, indeed.

But the Jackson Hole ‘symposium’, as it is called, is not just an opportunity for central bankers to explain and defend their monetary policy. It is also when the central bankers hear from leading mainstream economists about important trends and issues in the world economy. This year’s theme was: Structural Shifts in the Global Economy – in other words, looking at the long-term economic factors rather than the success of the policy on inflation.

While Powell only defended short-term Fed monetary policy, ECB President Christine Lagarde at least addressed the theme of the symposium in her address called, Policymaking in an age of shifts and breaks. Lagarde looked at long-term trends in inflation and trade. It made sober listening and reading.

Like Powell, she pointed out that the low level of unemployment was now being accompanied by falling hours of work. Digitilisation and remote working had increased and “according to one estimate, more than a quarter of jobs in advanced economies rely on skills that could easily be automated., even if this does not necessarily lead to a fall in available jobs.”

She pointed out that trade barriers had increased tenfold in the past decade, weakening international trade growth. So-called ‘free trade’ was being replaced by so-called ‘reshoring’ and ‘friend-shoring’ in strategic industries and so global supply chains were fragmenting. The ECB’s economists reckon that this could cut international trade by 12-19%; raise the world’s core inflation by 1.0-4.8% p.a. and lower global GDP by 1.0-5.0% from where it would have been over the rest of this decade!

Also this may mean that inflation will not return to previously low levels that existed before the pandemic – as inflation is being kept higher by these supply factors, not ‘excessive’ demand’. “These shifts – especially those related to the post-pandemic environment and energy – have contributed to the steep rise in inflation over the last two years. They have restricted aggregate supply while also directing demand towards sectors with capacity constraints”. So “for a start, we are likely to experience more shocks emanating from the supply side itself.” So much for the Powell thesis of demand factors.

Lagarde also indicated that rising arms spending plus greater supply constraints would mean “we are likely to see stronger price pressures in markets like commodities – especially for the metals and minerals that are crucial for green technologies.” So the problem is not going away but may get worse. So, unlike Powell, Lagarde admitted that supply constraints and corporate price rises had been driving inflation up and were now likely to keep the inflation rate permanently higher than before. “Under such conditions, we saw that firms are not only more likely to adjust prices, but also to do so substantially.

Despite that admission, Lagarde was quick to turn the focus on wages not profits: corporate price hikes were blamed on workers demanding more wages: “as we are seeing today, when workers have greater bargaining power, a surge in inflation can trigger “catch up” wage growth which can lead to a more persistent inflation process.” You see, workers asking for more wages to catch up with inflation only forces companies to raise prices to preserve profits – and of course, the latter is sacrosanct.

Lagarde went on: “we will have to be extremely attentive that greater volatility in relative prices does not creep into medium-term inflation through wages repeatedly “chasing” prices. That could make inflation more persistent if expected wage increases are then incorporated into the pricing decisions of firms, giving rise to what I have called “tit-for-tat” inflation.“

With her tit-for-tat image, Lagarde echoed the argument of Tom Weston in 1865 in a debate with Marx that workers should not ask for higher wages when prices rise because companies would respond with higher prices to protect their profits and so workers would gain nothing.

The rest of the symposium was taken up with presentations by leading mainstream economists on different aspects of the ‘structural shifts in the global economy’. And again they did not paint a picture of prosperity ahead.

One paper found that continued high interest rates set by the Fed and other central banks were, not surprisingly, likely to force significant declines in R&D investment and innovation. For every 1% hike in the rate, R&D spending would decline by about 1-3% and patents drop off by up to 9% over the next few years.

“We have to invest ever-rising resources in R&D just to maintain a constant rate of economic growth. ◦… we have to run faster and faster to stay in the same place, i.e. to maintain 2% overall growth.” Why was not explained.

Another paper reckoned that as the US reduced its sourcing of products from China, ”it is unclear if these measures will reduce US dependence on supply chains linked to China, and there are moreover already signs that prices of imports from Vietnam and Mexico are on the rise.” So isolating China could be damaging to global growth.

Another paper commented that public sector debt had “soared to unprecedented peacetime heights”. But the authors reckoned that “high public debts are not going to decline significantly for the foreseeable future. Countries are going to have to live with this new reality as a semi-permanent state.” That would ever more emerging economies in the Global South going into debt distress. – some 60% of such countries already in trouble. Other papers worried about the decline in the prospects for world trade and growth.

It seems that if world’s major economies sink into a slump or face unsustainable debts in the rest of this decade, there would be no ‘escape hatch’ from productivity growth or increased exports because innovation was being squeezed by high interest rates; and trade was being squeezed by US sanctions on Russia and China and by the rise in trade barriers. It all sounds like the 1930s not the roaring 20s.

It is navigating the stars in cloudy skies on a sinking ship in search of a safe harbour.

Be the first to comment