So the coronavirus slump will be deep and long lasting with a weak recovery to follow and could cause a financial crash. And working people will suffer severely, especially those at the bottom of the income and skills ladder. That is the message of the head of the world’s most powerful central bank.

Michael Roberts is an Economist in the City of London and prolific blogger

Cross-posted from Michael Roberts Blog

Last week’s speech by US Federal Reserve Chair Jay Powell at the Peterson Institute for International Economics, Washington was truly shocking. Powell told his audience of economists that “The scope and speed of this downturn are without modern precedent”. One shocking fact that he announced was that, according to a special Fed survey of ‘economic well-being’ among American households, “Among people who were working in February, almost 40% households making less than $40,000 a year had lost a job in March”!!!

Powell went on to warn his well-paid audience sitting at home watching on Zoom that “while the economic response has been both timely and appropriately large, it may not be the final chapter, given that the path ahead is both highly uncertain and subject to significant downside risks”. Indeed, if the continual downgrading of forecasts of global growth are anything to go by, then the number of optimists about a V-shaped recovery are beginning to dwindle to just the leaders of governments and finance.

Another study projects that US GDP will decline by 22% compared to the pre-COVID-19 period and 24% of US jobs are likely to be vulnerable. The adverse effects are further estimated to be strongest for low-wage workers who might face employment reductions of up to 42% while high-wage workers are estimated to experience just a 7% decrease.

And Powell was worried that this collapse could leave lasting damage to the US economy, making any quick or even significant recovery difficult. “The record shows that deeper and longer recessions can leave behind lasting damage to the productive capacity of the economy.”, said Powell, echoing the arguments presented in my recent post on the ‘scarring’ of the economy.

Powell reckoned the main problem in achieving any recovery once the pandemic was over was that “A prolonged recession and weak recovery could also discourage business investment and expansion, further limiting the resurgence of jobs as well as the growth of capital stock and the pace of technological advancement. The result could be an extended period of low productivity growth and stagnant incomes.” See here.

And there was a serious risk that the longer the recovery took to emerge, the more likely there would be bankruptcies and the collapse of firms and even banks, as “the recovery may take some time to gather momentum, and the passage of time can turn liquidity problems into solvency problems.”

Indeed, last week, the Federal Reserve released its semi-annual Financial Stability Report, in which it concluded that “asset prices remain vulnerable to significant price declines should the pandemic take an unexpected course, the economic fallout prove more adverse, or financial system strains re-emerge.” The Fed report warned that lenders could face “material losses” from lending to struggling borrowers who are unable to get back on track after the crisis. “The strains on household and business balance sheets from the economic and financial shocks since March will probably create fragilities that last for some time,” the Fed wrote. “All told, the prospect for losses at financial institutions to create pressures over the medium term appears elevated,” the central bank said.

So the coronavirus slump will be deep and long lasting with a weak recovery to follow and could cause a financial crash. And working people will suffer severely, especially those at the bottom of the income and skills ladder. That is the message of the head of the world’s most powerful central bank.

But the other message that Jay Powell wanted to emphasise to his economics audience was that this terrifying slump was not the fault of capitalism. Powell was at pains to claim that the cause of the slump was the virus and lockdowns and not the economy. “The current downturn is unique in that it is attributable to the virus and the steps taken to limit its fallout. This time, high inflation was not a problem. There was no economy-threatening bubble to pop and no unsustainable boom to bust. The virus is the cause, not the usual suspects—something worth keeping in mind as we respond.”

This statement reminded me of what I said way back in mid-March when the virus was declared a pandemic by the World Health Organisation. “I’m sure when this disaster is over, mainstream economics and the authorities will claim that it was an exogenous crisis nothing to do with any inherent flaws in the capitalist mode of production and the social structure of society. It was the virus that did it.” My response then was to remind readers that “Even before the pandemic struck, in most major capitalist economies, whether in the so-called developed world or in the ‘developing’ economies of the ‘Global South’, economic activity was slowing to a stop, with some economies already contracting in national output and investment, and many others on the brink.”

After Powell’s comment, I went back and had a look at the global real GDP growth rate since the end of the Great Recession in 2009. Based on IMF data, we can see that annual growth was on a downward trend and in 2019 global growth was the slowest since the GR.

And if we compare last year’s 2019 real GDP growth rate with the 10yr average before, then every area of the world showed a significant fall.

The Eurozone growth was 11% below the 10yr average, the G7 and advanced economies even lower, with the emerging markets growth rate 27% lower, so that the overall world growth rate in 2019 was 23% lower than the average since the end of the Great Recession. I’ve added Latin America to show that this region was right in a slump by 2019.

So the world capitalist economy was already slipping into a recession (long overdue) before the coronavirus pandemic arrived. Why was this? Well, as Brian Green explained in the You Tube discussion that I had with him last week, the US economy had been in a credit-fuelled bubble for the last six years that enabled the economy to grow even though profitability has been falling along with investment in the ‘real’ economy. So, as Brian says, “the underlying health of the global capitalist economy was poor before the plague but was obscured by cheap money driving speculative gains which fed back into the economy”. (For Brian’s data, see his website here).

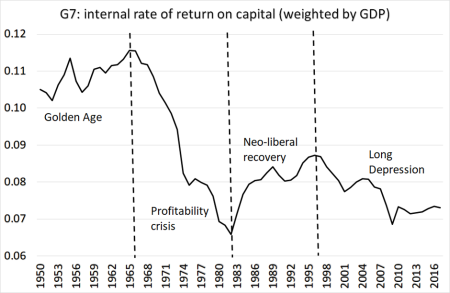

In that discussion, I looked at the trajectory of the profitability of capital globally. The Penn World Tables 9.1 provide a new series called the internal rate of return on capital (IRR) for every country in the world starting in 1950 up to 2017. The IRR is a reasonable proxy for a Marxian measure of the rate of profit on capital stock, although of course it is not the same because it excludes variable capital and raw material inventories (circulating capital) from the denominator. Despite that deficiency, the IRR measure allows us to consider the trends and trajectory of the profitability of capitalist economies and compare them with each other on a similar basis of valuation.

If we look at the IRR for the top seven capitalist economies, the imperialist countries, called the G7, we find that the rate of profit in the major economies peaked at the end of the so-called ‘neoliberal’ era in the late 1990s. There was a significant decline in profitability after 2005 and then a slump during the Great Recession, matching Brian’s results for the US non-financial sector. The recovery since the end of the Great Recession has been limited and profitability remains near all-time lows.

The IRR series only goes up to 2017. It would be possible to extend these results to 2019 using the AMECO database which measures the net return on capital similarly to the Penn IRR. I have not had time to do this properly, but an eye-ball look suggests that there has been no rise in profitability since 2017 and probably a slight fall up to 2019. So these results confirm Brian Green’s US data that the major capitalist economies were already significantly weak before the pandemic hit.

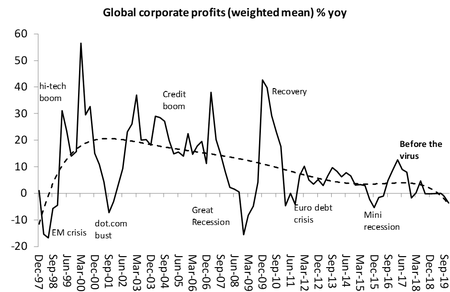

Second, we can also gauge this by looking at total corporate profits, not just profitability. Brian does this too for the US and China. I have attempted to extend US and China corporate profit movements to a global measure by weighting the corporate profits (released quarterly) for selected major economies: US, UK, China, Canada, Japan and Germany. These economies constitute more than 50% of world GDP. What this measure reveals is that global corporate profits had ground to a halt before the pandemic hit. Marx’s double-edge law of profit was in operation.

The mini-boom for profits that began in early 2016 peaked in mid-2017 and slid back in 2018 to zero by 2019.

That brings me to the causal connection between profits and the health of capitalist economies. Over the years, I have presented theoretical arguments for what I consider is the Marxian view that profits drive capitalist investment, not ‘confidence’, not sales, not credit, etc. Moreover, profits lead investment, not vice versa. It is not only the logic of theory that supports this view; it is also empirical evidence. And there is a stack of it.

But let me bring to your attention a new paper by Alexiou and Trachanas, Predicting post-war US recessions: a probit modelling approach, April 2020. They investigated the relationship between US recessions and the profitability of capital using multi-variate regression analysis. They find that the probability of recessions increases with falling profitability and vice versa. However, changes in private credit, interest rates and Tobin’s Q (stock market values compared with fixed asset values) are not statistically significant and any association with recessions is “rather slim”.

I conclude from this study and the others before it, that, although fictitious capital (credit and stocks) might keep a capitalist economy above water for a while, eventually it will be the profitability of capital in the productive sector that decides the issue. Moreover, cutting interest rates to zero or lower; injecting credit to astronomical levels that boost speculative investment in financial assets (and so raise Tobin’s Q) and more fiscal spending will not enable capitalist economies to recover from this pandemic slump. That requires a significant rise in the profitability of productive capital.

If we look at investment rates (as measured by total investment to GDP in an economy), we find that in the last ten years, total investment to GDP in the major economies has been weak; indeed in 2019, total investment (government, housing and business) to GDP is still lower than in 2007. In other words, even the low real GDP growth rate in the major economies in the last ten years has not been matched by total investment growth. And if you strip out government and housing, business investment has performed even worse.

By the way, the argument of the Keynesians that low economic growth in the last ten years is due to ‘secular stagnation’ caused by a ‘savings glut’ is not borne out. The national savings ratio in the advanced capitalist economies in 2019 is no higher than in 2007, while the investment ratio has fallen 7%. There has been an investment dearth not a savings glut. This is the result of low profitability in the major capitalist economies, forcing them to look overseas to invest where profitability is higher (the investment ratio in emerging economies is up 10% – I shall return to this point in a future post).

What matters in restoring economic growth in a capitalist economy is business investment. And that depends on the profitability of that investment. And even before the pandemic hit, business investment was falling. Take Europe. Even before the pandemic hit, business investment in peripheral European countries was still about 20 per cent below pre-crisis levels.

Andrew Kenningham, chief Europe economist at Capital Economics, forecast eurozone business investment would fall 24 per cent year on year in 2020, contributing to an expected 12 per cent contraction in GDP. In the first quarter, France reported its largest contraction in gross fixed capital formation, a measure of private and public investment, on record; Spain’s contraction was also near-record levels, according to preliminary data from their national statistics offices.

In Europe, manufacturers producing investment goods — those used as inputs for the production of other goods and services, such as machinery, lorries and equipment — experienced the biggest hit to activity, according to official data. In Germany, the production of investment goods fell 17 per cent in March compared with the previous month, more than double the fall in the output of consumer goods. France and Spain registered even wider differences

Low profitability and rising debt are the two pillars of the Long Depression (ie low growth in productive investment, real incomes and trade) that the major economies have been locked into for the last decade. Now in the pandemic, governments and central banks are doubling down on these policies, backed by a chorus of approval from Keynesians of various hues (MMT and all), in the hope and expectation that this will succeed in reviving capitalist economies after the lockdowns are relaxed or ended.

This is unlikely to happen because profitability will remain low and may even be lower, while debts will rise, fuelled by the huge credit expansion. Capitalist economies will remain depressed, and even eventually be accompanied by rising inflation, so that this new leg of depression will turn into stagflation. The Keynesian multiplier (government spending) will be found wanting as it was in the 1970s. The Marxist multiplier (profitability) will prove to be a better guide to the nature of capitalist booms and slumps and show that capitalist crises cannot be ended while preserving the capitalist mode of production.

Be the first to comment