Tax evasion is not going away. Transnational agencies seem to have little interest in implementing rules and laws to change this. The ICRICT makes cocnrete proposals for the next step in the fight against tay evasion.

Tax Justice Network is an NGO dedicated to high-level research, analysis and advocacy in the area of international tax and the international aspects of financial regulation

The Independent Commission for the Reform of International Corporate Taxation (ICRICT) has launched a ‘roadmap’ for taxing multinationals. This important intervention not only confirms the failure of current tax rules to deliver fair outcomes internationally, but sets the course for a specific alternative that would significantly strengthen fiscal sovereignty for countries at all income levels: unitary taxation with formulary apportionment.

“ The fairest and most effective version of unitary taxation is multi-factor global formulary apportionment with a minimum corporate tax rate. We urge global leaders to adopt a roadmap towards this goal, including more short-term measures which would be more effective, easier to administer, and provide greater certainty, than the current defective methods.”

ICRICT

The commission includes a range of leading international thinkers, from Magdalena Sepulveda and Joseph Stiglitz to Eva Joly and Leonce Ndikumana. It was established by a broad coalition of civil society and labour organisations, including TJN, with the aims of:

- promoting the international corporate tax reform debate through a wider and more inclusive discussion of international tax rules than is possible through any other existing forum;

- to consider reforms from a perspective of public interest rather than national advantage; and

- to seek fair, effective and sustainable tax solutions for development.

The appointment of two new commissioners has just been announced: Thomas Piketty and Gabriel Zucman.

Comparative assessment of unitary approaches

The Commission’s earlier work led it to the conclusion that current international tax rules are simply not fit for purpose – based as they are on the economically illogical accounting fiction that each entity within a multinational group can be assessed as if it maximised profits independently by transacting with the group using market (“arm’s length”) prices.

The alternative is to treat multinational groups according to their reality, that they aim to maximise profits at the unit of the overall group. This respects the economic rationale, which is that multinational enterprises (MNEs) exist precisely because they can outperform a collection of independent smaller firms performing the same functions but without a common management control. The question then is how to distribute taxable profits that arise at the unit of the group (rather than that of individual entities in different countries), between the various countries where the group operates.

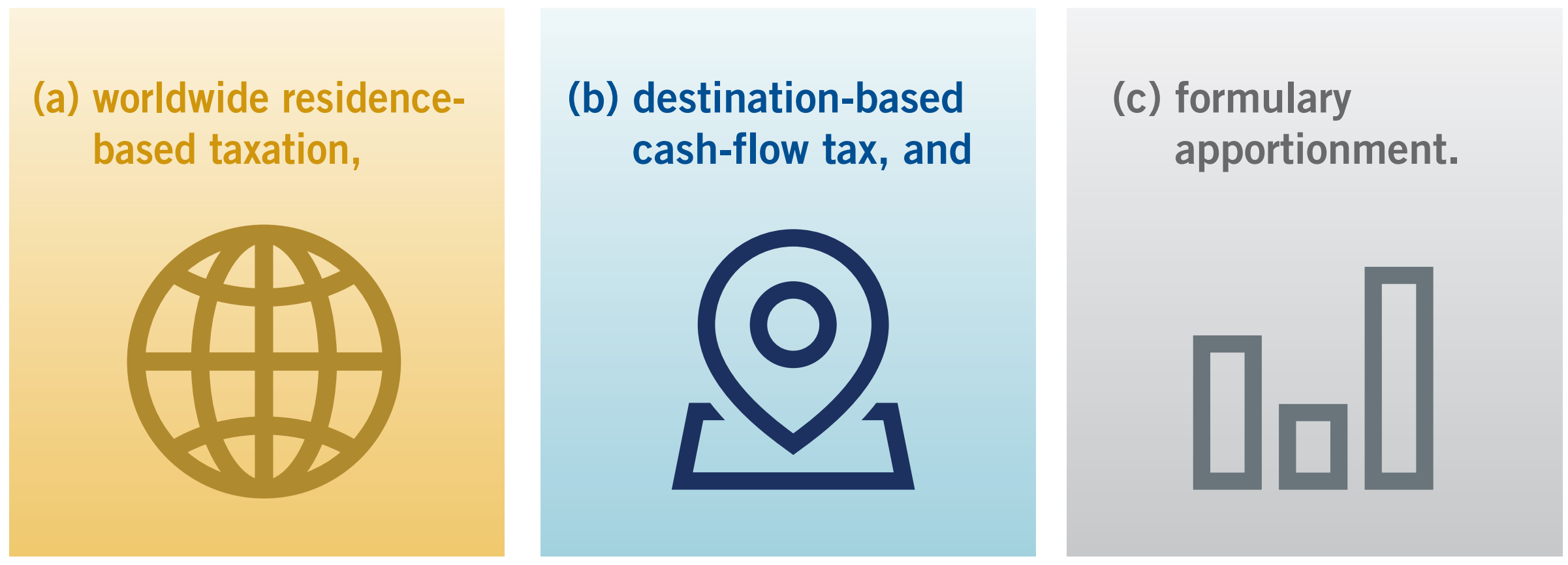

A range of unitary tax approaches exists, and ICRICT commissioners have heard evidence over the last year about each of the three leading options.

The report lays out the strengths and weaknesses of each. Briefly, residence-based taxation is found attractive in principle only: “the manipulability of the definition of the residence jurisdiction, which is central to [such a] regime, is a fatal flaw when it comes to taxing MNEs.”

The commission identifies a wide range of weaknesses for the destination-based cash flow tax (DBCFT) which for a period dominated policy discussions in the United States. First, it would require much greater cooperation between states to resolve issues around MNE operations where there is minimal physical presence in a jurisdiction. Second, the likely violation of World Trade Organisation rules would encourage protectionist conflict. And third, importantly but completely overlooked in the US debate, a global shift towards DBCFT would exacerbate rather than ameliorating the tax injustices that lower-income countries already face.

Therefore:

“It is the Commission view that global formulary apportionment is

the only method that allocates profits in a balanced way using

factors reflecting both supply (e.g., assets, employees, resources used)

and demand (sales). Neither can create value without the other.”

Steps on the road

There has for some time now been a growing sense that the arm’s length approach is finished, and that the OECD BEPS process of 2013-2015 would come to be seen as the last great defence of a set of international tax rules that were left behind by globalisation.

But change comes painfully slowly, especially when multinationals and their ‘big four’ tax advisers are so heavily invested in the status quo. Valuably, therefore, the ICRICT report does not stop at indicating the direction of travel for international rules. Instead, it lays out a series of steps along the way – recommendations for the here and now.

“While a system of formulary apportionment is the long-term aim, we are

convinced that additional measures can be adopted in the short term leading in this direction. Such reforms can move the current system away from the dysfunctional independent entity principle and use of transfer pricing rules, and realign the rules to treating MNEs according to the economic reality that they operate as unitary enterprises.”

The options discussed include profit-split and shared net margin methods, as well as my own proposal for a formulary alternative minimum corporate tax (although unthinkably, the commission eschews the acronym, FAMICT).

“In the absence of global coordination and agreement, an individual country or region could consider implementing formulary apportionment as part of a domestic alternative minimum tax regime. In such a regime, formulary apportionment would determine the income base for computing an alternative minimum corporation tax.

The country could define the local corporation tax base by applying a multi-factor formula to a MNE’s global income, and compute the minimum tax payable on that apportioned income, for example at 80 percent of the regular corporation tax rate. The minimum tax would be payable if it exceeds the jurisdiction’s regular corporation tax payable computed on the MNE’s local income as determined under conventional arm’s-length transfer pricing methods.

Such an alternative minimum tax regime could be enacted as domestic legislation without the need to repudiate existing multilateral agreements and commitments to the arm’s-length principle, including the OECD transfer pricing guidelines. This would extend the concept of ‘safe harbors’…”

Finally, the commission highlights the critical importance of changing the political context from the rich countries’ club of the OECD, to the fully inclusive UN:

“Only the UN’s universal membership and open and democratic structure can give full voice to the tax policymakers and the entire civil society from all countries. We therefore renew our call for international taxation to be brought under the aegis of the UN, which alone can provide the legitimacy for rules to coordinate such a central element in the sovereignty of all states.”

And so say all of us… The ICRICT report is available in English, French and Spanish, and the press release also in Italian and Portuguese.

Be the first to comment