The current state and future of the Chinese economy

Michael Roberts is an Economist in the City of London and a prolific blogger.

Cross-posted from Michael Roberts’ blog

The annual meeting of China’s National People’s Congress (NPC) is underway right now. The NPC is officially China’s highest deliberative body, ostensibly deciding economic and social policies each year. In reality, those policies have been drawn up by the Chinese Communist Party leaders in advance and then presented to the NPC to vote on (unanimously). Nevertheless, the NPC meeting offers the CP leaders an opportunity to spell out their policy answers to deal with the current economic and social problems of the country.

As is usual, it was the job of China’s premier to present this to the NPC. This year, there is a new premier, Li Qiang. But Li’s speech was very much in line with last year’s by the previous premier Li Keqiang. As last year, Li Qiang set a target for real GDP growth in 2024 of “around 5%” and said that China would be looking to “transform” China’s economic growth model.

The NPC will also be considering the annual budget. Defence spending is expected to rise by 7.2%, while public security spending is slated to rise by 1.4%, no doubt necessary given the military surrounding of China by the Western powers. Central government expenditures are expected to rise by 8.6% to reduce the burden somewhat on the highly indebted local governments. Other targets announced by Li include the creation of 12m new urban jobs and increasing consumer prices by about 3% (apparently to avoid deflation – see below). Li said these targets would “not be easy” but that “high quality development” remained the priority.

All this is pretty much in line with the targets set in China’s last five-year plan. The 14th plan agreed in 2021 was a comprehensive document covering all aspects of the Chinese economy in detail. But it had some key targets. In particular, China aimed at becoming a “moderately developed” economy by 2035 and to reduce inequality between urban and rural areas. The plan was based on the dual circulation model, where expanding manufacturing exports – the past key to China’s miracle growth -is combined with developing the domestic economy and reducing reliance on foreign imports and investment. The objective is that China can continue to grow and increase living standards despite attempts by Western governments to curb or strangle such growth.

Can China succeed in achieving both its growth target for this year and reach the longer-term objectives over the next ten years or so, taking nearly 1.4bn people up to living standards only enjoyed by a small group of nations in Europe, North America and East Asia?

If you were to read the Western press and their economists, you would conclude that the chances of China doing that are no better than a snowball surviving on being thrown into the sun. It is the almost unanimous cry of Western economists, particularly the ‘China experts’, that the China ‘miracle’ is over, and worse, China is heading into a debt deflation spiral that will mean growth targets will not be met at best, and more likely there will be a major slump. This is despite the fact that in 2023 China had an official growth rate of 5.2%, more than double that of the ‘booming’ US economy, and five times the rate of growth in the rest of top capitalist economies of the G7. (Don’t get me into the argument that China’s growth figure is fake and growth is much lower. Those that argue this have little supporting evidence.)

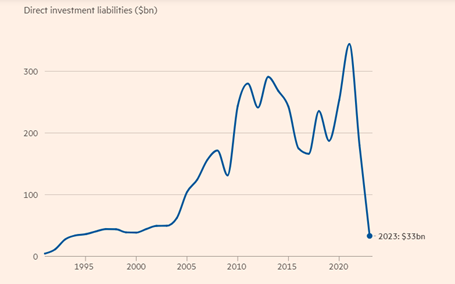

Ah, but you see, manufacturing is in recession (as measured by official surveys), consumption is weak (still below pre-pandemic levels) and foreign investment, seen as the life-blood for the Chinese economy has dried up.

And even worse, prices of goods and services are falling. Readers may be surprised to hear that Western economists, who spend much of their time demanding that inflation rates in their countries be reduced to no more than 2% a year after the post-COVID inflationary spiral of the last three years, see no merit in the lack of any rising prices (and therefore rising real wages) in the Chinese economy: it’s ‘inflation bad for the US; but no inflation bad for China’.

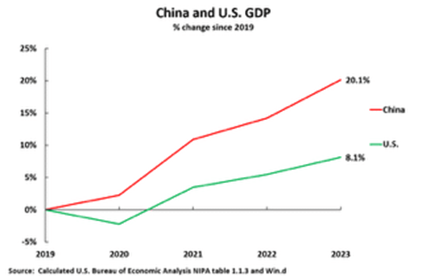

In a recent article, John Ross has shown that to achieve China’s Plan GDP target for 2025 ie a doubling GDP from 2021, it would require an average annual growth of 4.7% a year. So far, China is ahead of this goal with annual average growth in 2020-2023 of about 5%. Indeed, since the beginning of the pandemic, China’s economy has grown by 20.1% and the U.S. by 8.1%—that is China’s total GDP growth since the beginning of the pandemic has been two and half times greater than the US.

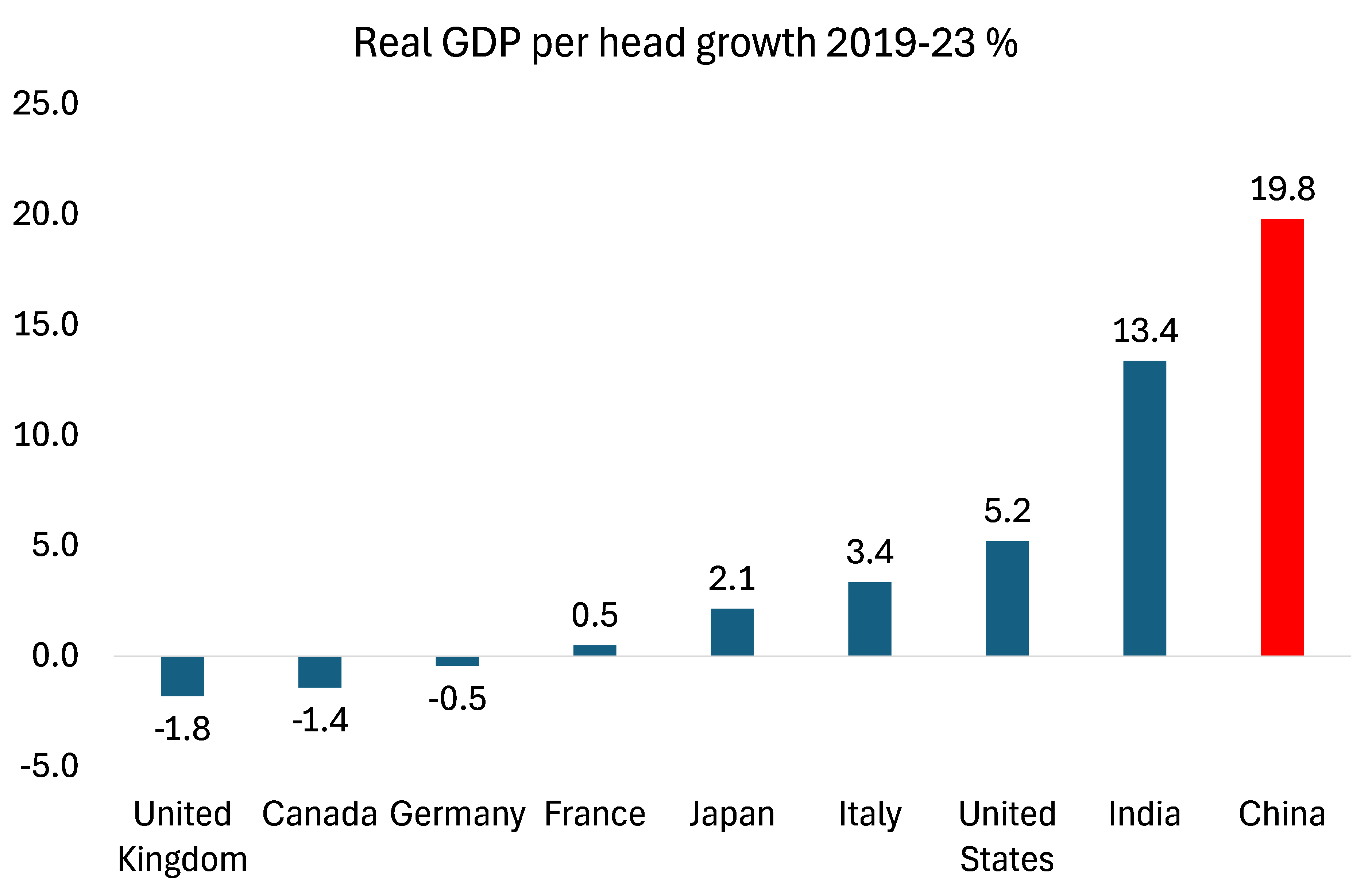

Yes, China’s annual growth rates have slowed from the breakneck pace of the 1990s onwards and the Chinese workforce is declining. But just look at the increase in GDP per person that China has achieved compared to the G7 economies since 2019, some of which have even contracted (IMF data). The rise on per capita basis is even higher against the US (nearly four times).

Yes, increasingly China cannot rely on an expansion of a cheap workforce from rural areas to achieve more output, but instead must raise the productivity of the existing labour force, especially through investment in technical innovation. And it is doing so. The Federal Reserve Bank of Dallas shows that ‘total factor productivity’ (which is a crude measure of innovation) is growing at 6% a year, while it has been falling in the US.

Despite this evidence, every year the Western ‘China’ experts (and even many in China itself) predict stagnation, given the huge debt levels in all sectors. China is going to stagnate like Japan has done in the last three decades. The only way to avoid ‘Japanification’, say these experts, is to ‘rebalance’ the economy from ‘over-investment’, ‘excessive savings’ and exports to a domestic consumer-led economy as in the West and reduce the state control of the economy so that the private sector can flourish.

This year on the occasion of the NPC, Martin Wolf, the Keynesian guru of the Financial Times, returned to this theme, echoing the arguments of other Keynesian China experts like Michael Pettis. According to Wolf, China’s growth will now slow to a trickle as in Japan because it overloaded with excessive debt and because it has not rebalanced the economy towards “the consumer”. China needs to get its consumption share up to Western levels or it will not be able to grow and so stay locked in a ‘middle income’ trap.

China generated 28 per cent of total global savings in 2023. This is only a little less than the 33 per cent share of the US and EU combined. This is all wrong, say Wolf and Pettis. What is needed is a shift from ‘excessive savings’ to consumption. There is over-investment in property and infrastructure, instead of handouts to households. China will only grow from here if consumption leads, not investment.

If you want to read more of this nonsense about consumption being the leader of growth, see my review of Pettis’ theories here.

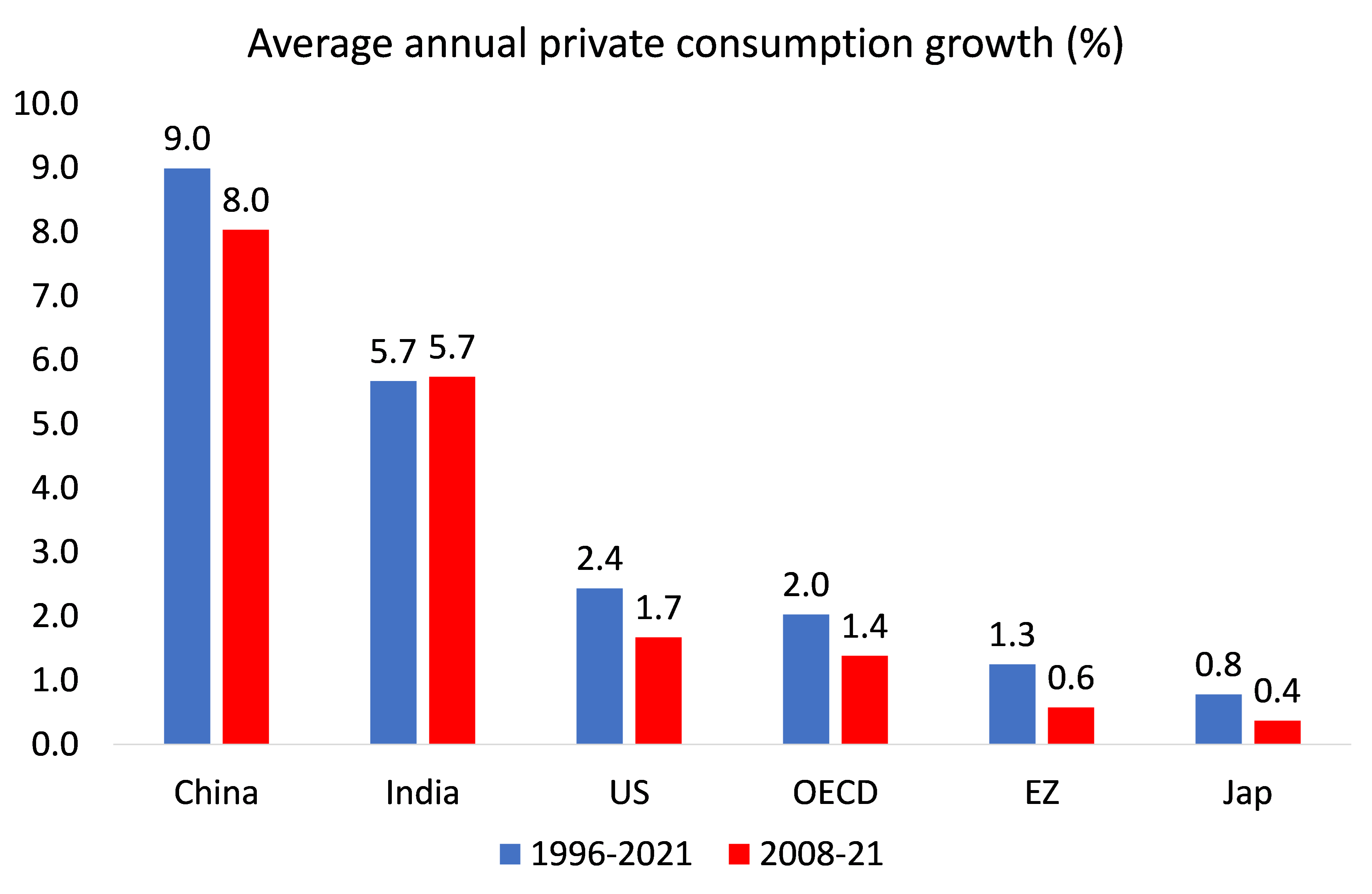

But how can anybody claim that the mature ‘consumer-led’ economies of the G7 have been successful in achieving steady and fast economic growth, or that real wages and consumption growth have been stronger there? Indeed, in the G7, consumption has failed to drive economic growth and wages have stagnated in real terms over the last ten years, while real wages in China have shot up. Moreover, these consumer-led economies have been hit by regular and recurring slumps in production that have lost trillions in output and income for their populations. The irony is that China’s consumption growth rate is way higher than in the G7 economies.

China has not had a contraction in national income in any year since 1976, while the consumer-led G7 economies have had slumps in 1980-2, 1991, 2001, 2008-9 and 2020. Much has been made of China’s ‘disastrous’ zero COVID policy. But apart from saving millions of lives, China still did not enter a slump in 2020, unlike all the G7 economies in 2020.

Yes, China has the highest ratio of gross investment to GDP among the major economies. But this supposedly ‘over-invested’, ‘excessive savings’ economy has grown more than four times faster than the consumer-led OECD economies and 40% faster than India as a result. What this suggests that if China were to ‘rebalance its economy towards the consumer and reduce investment; and reduce the public sector and ‘free up’ the private sector (the sector that provides most consumer goods in China), growth rates would fall even more than they have done in recent years.

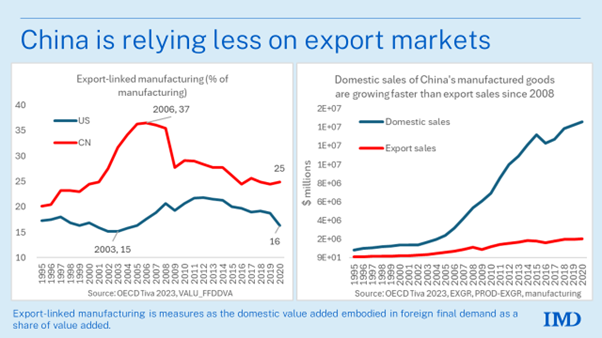

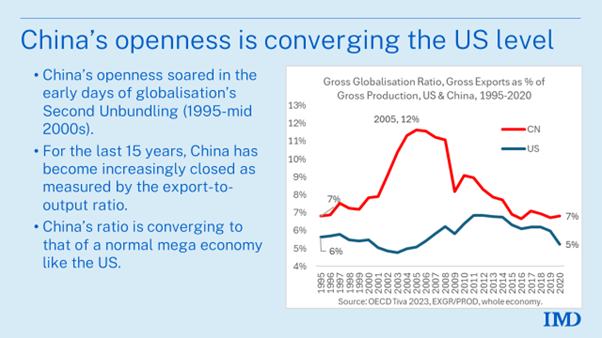

Moreover, the arguments of the Western experts that China is stuck in an old model of investment-led export manufacturing and needs to ‘rebalance’ towards a consumer-led domestic economy where the private sector has a free rein are just not empirically valid. Is China’s weak consumer sector forcing it to try and export manufacturing ‘over capacity’? Not according to a recent study by Richard Baldwin. He finds that the export-led model did operate up to 2006, but since then domestic sales have boomed, so that the exports to GDP ratio has actually fallen. “Chinese consumption of Chinese manufactured goods has grown faster than Chinese production for almost two decades. Far from being unable to absorb the production, Chinese domestic consumption of made-in-China goods has grown MUCH faster than the output of China’s manufacturing sector.”

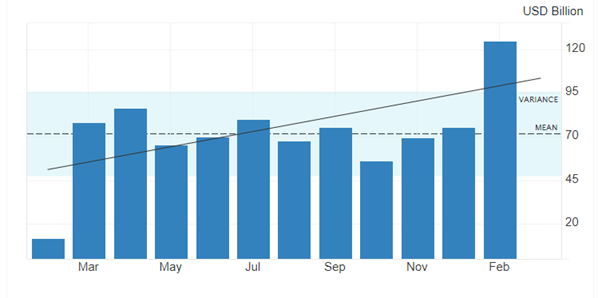

Western experts go on about the size of China’s export surplus, namely that the current account (the balance of receipts from abroad against payments), claiming that the surplus is as high as 4% of China’s GDP. And China’s exports are 15% of the world total. And just in the last month exports rose over 7% so that China’s balance of trade with the rest of the world reached an all-time high of $125bn in February.

But what that shows is that Chinese manufacturers remain highly competitive in world markets, despite all the efforts of the West to impose tariffs and other protectionist measures. China is doing particularly well in electric vehicle production, solar energy and other green technologies. But as Baldwin points out, this export success does not mean that China depends on exports for growth. China is growing mainly because of production for the home economy, like the US.

It is true is that ‘productive’ investment growth has fallen back in China. In my view, successive Chinese governments made a big mistake in trying to meet the housing needs of its burgeoning urban population by creating a housing for sale market, with mortgages and private developers being left to deliver. Instead of local governments launching housing projects themselves to house people for rent, they sold state assets (land) to capitalist developers who proceeded to borrow heavily to build projects. Soon housing was no longer for living but for speculation (Xi quote). Private sector debt rocketed – just as in the real estate bubble in the West. It all came to a head in the COVID pandemic as developers and their investors went bust.

What the Chinese government now needs to do is take over these large property developers and bring them back into public ownership, complete the projects and switch to building for rent. The government should annul the developers’ debt to foreign investors and only meet obligations to small investors; and end the mortgage and private finance system permanently. The unproductive real estate sector has got so large in China as a share of investment and output that it has seriously degraded growth. This is where the economy does need rebalancing. There needs to be a switch to productive investment in technology and knowledge industries. If the words of the Five-Year Plan mean anything, it seems that the current Chinese leadership is aware of that.

Previous CP leaders also relied too much on foreign investment and a rising capitalist sector to grow the economy. But China’s capitalist sector has experienced falling profitability (just as in the West) and so has cut back on productive investment. The state sector has had to step up to the plate. What flows from that is, contrary to the views of the Western experts, it’s not less investment and more consumption, not less public and more private investment, not more foreign and less state investment that China needs to sustain its previous economic success, but the opposite.

Be the first to comment