Going Down the Rabbit Hole at Jackson Hole

Servaas Storm is Senior Lecturer of Economics, Delft University of Technology

Cross-posted from the website of the Institute for New Economic Thinking

In the waning days of August, in a world beset by the unending COVID19 public health crisis, by increasingly frequent extreme climate events, and by the terrible news from Afghanistan, the world’s central bankers, the rich, and the influential gathered (online) for the Federal Reserve Bank of Kansas City’s annual Jackson Hole symposium. The title of this year’s Economic Policy Symposium was “Macroeconomic Policy in an Uneven Economy.” Few observers were paying attention and most had low expectations, knowing that central bankers are caught in a catch-22: they cannot lower interest rates (already at the zero-lower bound) to boost the economy, and they cannot raise rates, because the current high private and public debts are sustainable only at very low interest rates. Likewise, central bankers are unable to discontinue their accommodative (QE) policies, because this would abruptly end the irrational exuberance in financial markets and risk another global financial crash. Indeed, Fed chair Jay Powell’s speech was predictably careful, cautiously outlining how the Fed will continue its accommodative policy, while steadily monitoring data for signs of persistent broad-based inflation. No news from the monetary policy front, in other words.

However, one of the contributions to the symposium, a paper by Atif Mian, Ludwig Straub, and Amir Sufi (2021), managed to make headlines in the New York Times and the Financial Times (amongst others). The authors argue that high income inequality is the cause, not the result, of the low natural rate of interest r* and high asset prices evident in recent years. “As the rich get richer in terms of income, it creates a saving glut,” Professor Mian told the New York Times, “The saving glut forces interest rates to fall, which makes the rich even wealthier. Inequality begets inequality. It is a vicious cycle, and we are stuck in it” (Irwin 2021). In the same New York Times article, Professor Sufi is quoted, saying “These forces pushing down r-star are probably so powerful that the Fed could never fight against them.” Thus, central bankers are “in this story, […] the equivalent of drivers on a highway who must adapt their speed to road conditions. The Fed has kept rates low for the past decade because those rates have been the ones that keep the economy stable. If it had tried to push them higher, the result would have been a recession.” (Irwin 2021) This message must have been music to the ears of the beleaguered central bankers, and balm for their troubled souls, because, if true, it absolves them from the responsibility for having landed the economy in the catch-22 of low interest rates, excessive indebtedness, and over-inflated asset prices.

The problem with the analysis by Professors Mian, Straub and Sufi (2021) is that it is incoherent on its own terms (i.e. even if we accept the deeply problematic notions of a natural rate of interest and the loanable funds market) and quite at odds with the realities of saving in modern economies. My critique comes in three parts.

The first problem concerns the empirical evidence: the authors incorrectly focus on the increase in the household saving rate, but surely what should matter for their argument is the aggregate savings rate, the rate for the economy as a whole. I will show below that the aggregate savings rate of the U.S. did not rise, which means that even if household savings increased, there was no aggregate saving glut and hence no reason for r* to decrease. This already means that the key argument makes no sense on its own terms.

Secondly, Professors Mian, Straub and Sufi argue that the increase in the average household saving rate must have been caused by a change in household preferences: U.S. households have, on average, become more patient and willing to postpone consumption (today) in favor of higher savings and higher consumption in the future. The authors thus conclude that the ‘rate of time preference’ of the average U.S. household has declined — which (in their reasoning) is also the reason that the natural rate of interest r* has declined.

Unfortunately, their own empirical findings of changes in the class-wise household saving rates contradict this conclusion. Their empirical evidence shows that “the saving rate of the top 10% group in the post-period is similar to the pre-period. [….] the saving rates of the bottom 90% fall considerably” (Mian, Straub and Sufi 2021, p. 21). With savings rates for one group unchanged and the other 90% of the population consuming more, the rate of time preference of the average U.S. household must have increased — which is the exact opposite of what the authors conclude.

However, the biggest problem of all is that there is no such thing as a market for loanable funds. The irrelevance of this old Wicksellian story has been explained many times, starting with Keynes (1936, 1939), but more recently by Lindner (2015), Taylor (2016), and Storm (2017). Banks pre-finance investment; investment creates incomes; people save out of their incomes; and at the end of the day, ex-post savings equal investment. This is what Bank of England economists Jakab and Kumhoff (2015) write:

“…. if the loan is for physical investment purposes, this new lending and money is what triggers investment and therefore, by the national accounts identity of saving and investment (for closed economies), saving. Saving is therefore a consequence, not a cause, of such lending. Saving does not finance investment, financing does. To argue otherwise confuses the respective macroeconomic roles of resources (saving) and debt-based money (financing).”

There exists no market for ‘savings’ and ‘investment’ which is cleared by an equilibrium interest rate, and, hence the savings glut story of Professors Mian, Straub and Sufi (2021) makes no sense.

This note reviews the three weaknesses mentioned above and concludes that it is incorrect to view central bankers as mere “drivers on a highway who must adapt their speed to road conditions”; instead, it makes more sense to regard central bankers as the main traffic control which regulates and enforces traffic volume, speed and road conditions, in normal times and during emergencies. Together with governments and establishment economists, central bankers carry much of the responsibility for the increased inequality, slow growth, high debts, and over-inflated asset prices, however much Professors Mian, Straub and Sufi try to persuade us to believe otherwise.

What explains the secular decline in r*?

Before proceeding to the critique, let us first consider the argument by Mian, Straub and Sufi (2021). The paper considers two explanations of low interest rates:

(1) increased household savings, driven by the baby-boom generation’s accumulation of retirement savings; this is the demographic explanation (see Goodhart and Pradhan 2020).

(2) Increased household savings, driven by higher income (and wealth) inequality, given the fact that rich people save a larger share of their income than the middle class and the poor; this is the ‘inequality’ explanation.

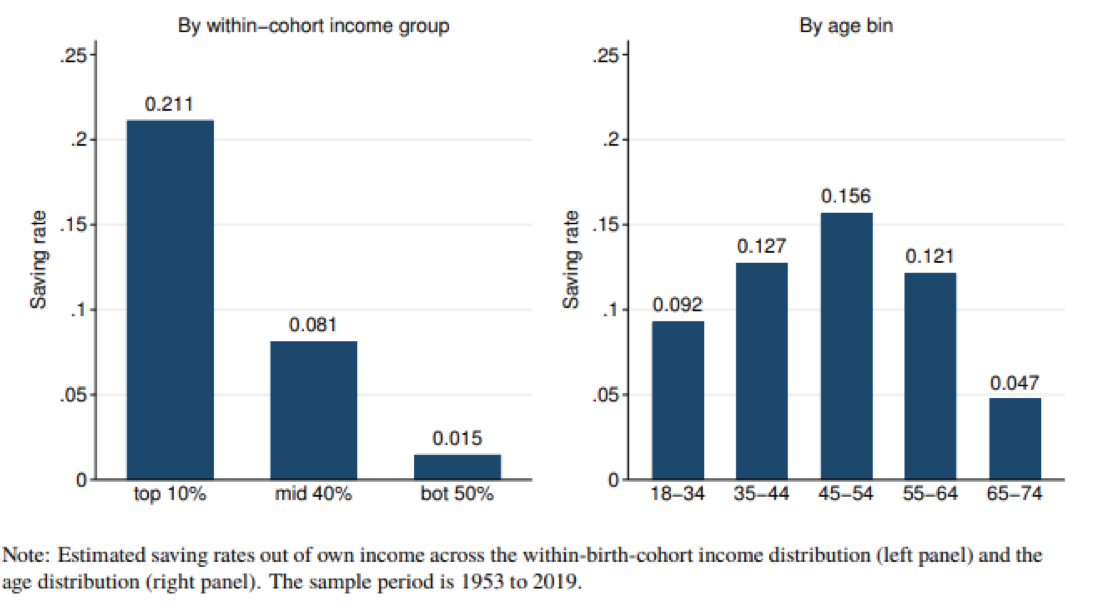

Using data for the U.S. during 1952-2019, Mian, Straub and Sufi find that the impact of higher inequality overwhelms the influence on household savings from demographics. Their evidence shows that, across all birth cohorts, higher-income households have significantly higher saving rates than lower-income households — which is a stylized fact that has been known for ages, see e.g., Saez and Zucman (2016) and Taylor (2020).

Figure 1 reproduces the findings of Mian, Straub and Sufi (2021): the differences in saving rates between age groups (birth cohorts) in the right panel are much smaller than the differences in saving rates between the top 10%, next 40%, and bottom 50% of households within-birth cohorts in the left panel. Mechanical life-cycle effects do not matter much and what is more, the findings of Figure 1 also disprove the assumption of a constant saving rate out of lifetime income across all households that underlies most macro models.

Figure 1 Saving rates across the within-cohort income and age distribution Source: Mian, Straub and Sufi (2021), Figure 3.

Clearly, inequality is not just an end-of-pipe distributional outcome, but a central determinant of macroeconomic dynamics. To see this, note that the income share of the higher-saving top 10% of households increased — from about 30% in the early 1970s to 43% in recent years — and the income shares of the lower-saving next 40% and bottom 50% declined. Given the differential saving rates (recorded in Figure 1), the increased inequality did indeed raise the overall private saving rate in the U.S. by more than 3 percentage points of national income every year. This represents more than one-third of average annual private savings in recent years, or more than $ 0.6 trillion of additional annual savings. “The rise in income inequality leads to a large rise in saving,” conclude Mian, Straub and Sufi (2021, p. 21), “and therefore is a likely culprit when assessing forces that push down r∗.”

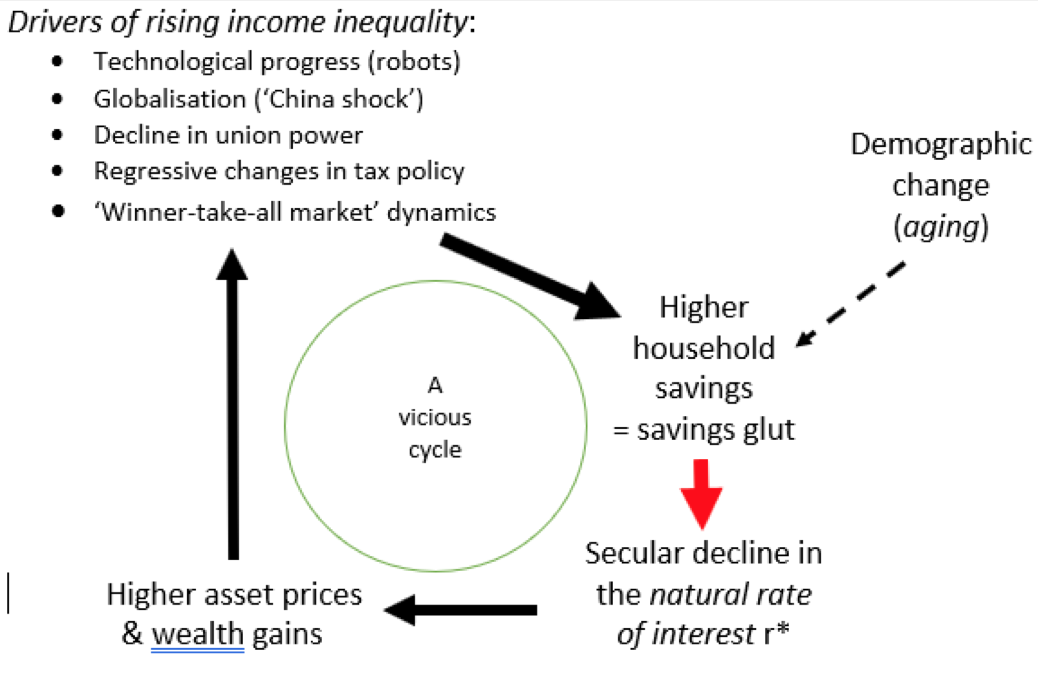

Figure 2 summarizes the argument of Mian, Straub and Sufi (2021). The fact of greater income inequality is taken as a given, perhaps as a result of technological progress, globalization, etc. – all factors beyond the control of central banks. Given differential saving rates by income classes, higher income inequality led to a pile-up of household savings, and a secular decline in the natural rate of interest r* (the red arrow in Figure 2) given this relative abundance (more on this below). The idea is that central banks had to adapt to the configuration of historical forces and thus lowered interest rates; in turn, cheap credit fuelled asset-price inflation, and with the top 10% richest households benefitting most from the resulting wealth gains, inequality spiraled up further, leading to another round of increased savings, lower r* and wealth gains.

This, indeed, is the bottom line of the paper by Mian, Straub and Sufi (2021): central bankers, even those at the Fed, the world’s most powerful central bank, have far less power in managing the macroeconomy than is commonly believed, and the best they can do is to adapt to the natural forces of technological progress and global integration, rather than attempting to go against these inexorable currents. Accordingly, the task of the ‘science’ of monetary policymaking is limited: to follow and adapt to what is happening anyway — bending along in ways that maintain economic and financial stability. The way they frame their argument, the authors manage to kill two birds with one stone: on the one hand, they succeed in de-politicizing and ‘naturalizing’ monetary policymaking by invoking the troubled notion of the natural rate of interest r* — and on the other hand, they manage to ‘naturalize’ inequality by removing monetary policy as a key driver of growing income concentration and primarily attributing it to the ‘impersonal forces’ of technological progress and globalization, which arguably are mostly beyond policy control.

Figure 2 Mian, Straub and Sufi’s (2021) savings glut hypothesis

First problem: despite the rise in inequality, there is no savings glut

If Professors Mian, Straub and Sufi are right that high inequality is the cause of the low interest rates, then we should observe an increase in aggregate savings in the U.S. Surely, the natural rate of interest r* is determined not just by household savings, but by aggregate savings.

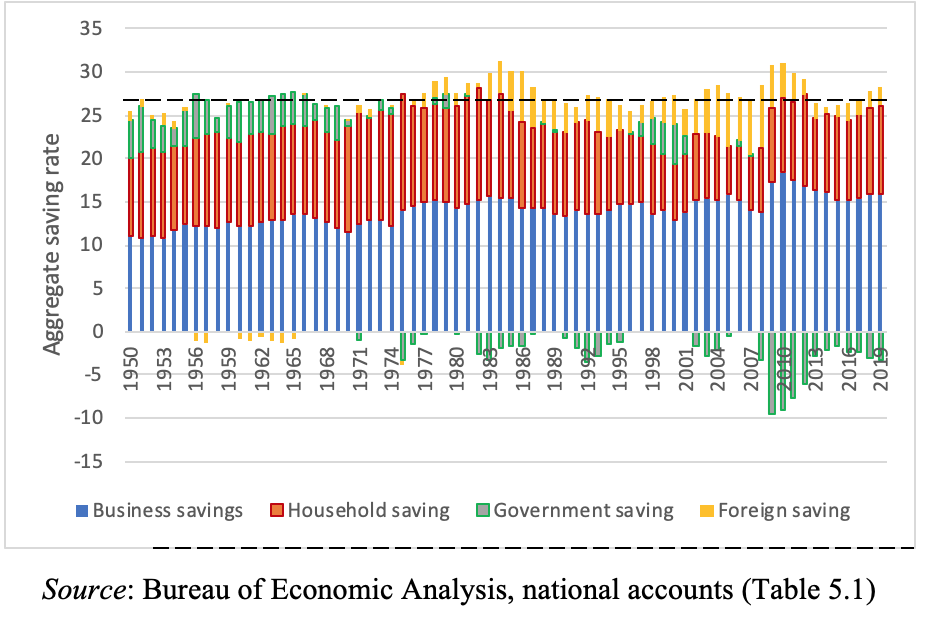

Aggregate savings, as we know from the national accounts, consist of savings by households, business, and government as well as foreign savings (which by accounting convention are equal to the difference between imports and exports). As is shown by Figure 3, the aggregate saving rate of the U.S. remained quite close to its long-term average of 25.8% (of national income) and does not exhibit a rising trend. There is no American savings glut, in other words – however much Professors Mian, Straub and Sufi would like to persuade us that there is an over-supply of savings.

Figure 3 The aggregate saving rate and its composition: The U.S. 1950-2020 (% of national income)

However, we can see in Figure 3 that the composition of aggregate savings changed. The saving rate of households averaged 11.7% (of national income) during 1980-85 and 6.7% during 2003-08; with rising income inequality, the household saving rate increased to an average of 9.7% during 2015-2019. But, all along, the aggregate U.S. saving rate remained more or less the same, because the other sources of saving offset the changes in household saving. Specifically, as the household saving rate rose during the previous decade, the government saving rate and the foreign saving rate (the trade deficit) declined; government savings even turned negative (Figure 3).

This is not surprising, because the increase in income inequality led to higher household savings, lower demand, and slow growth, which in turn contributed to an increase in public deficits and a decline in the trade deficit (because of slower import growth).

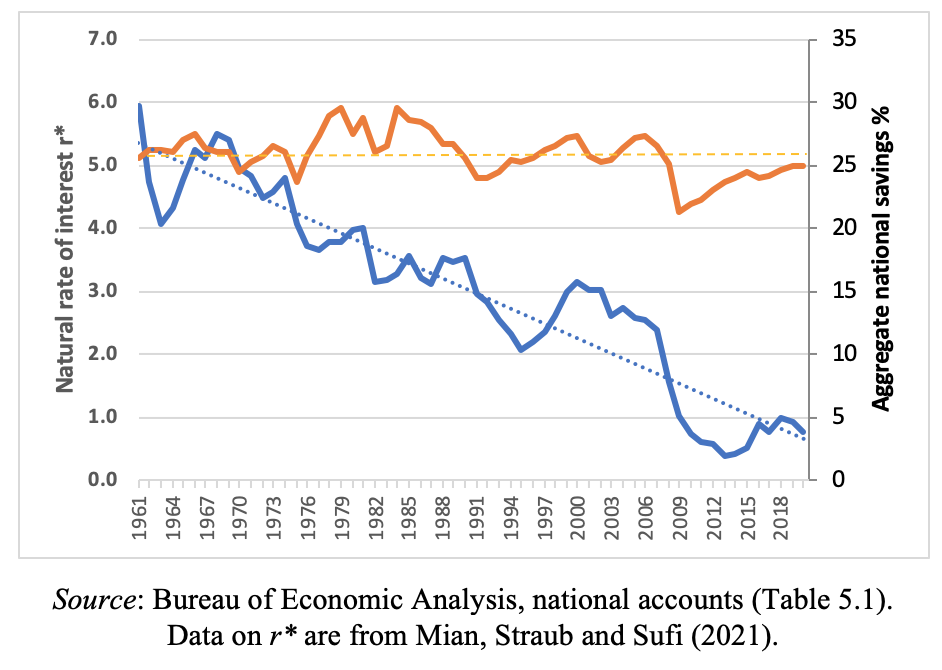

Figure 4 shows the “natural rate of interest r*”, as constructed by Mian, Straub and Sufi (2021) themselves, and the national savings rate in the U.S. during 1961-2020. Their construction of r* exhibits a statistically significant downward trend, declining from an average of 5% during the 1960s to an average of 0.68% during 2011-2020. But as we saw already in Figure 3, the national savings rate of the U.S. shows no trend: it was 26.1% in the 1960s, 26.6% in the 1970s, 27.7% in the 1980s, 25.6% in the 1990s, 25.2% during 2001-2010, and 24% during 2011-2019. Even in 2019, the national savings rate was 25%.

Three conclusions follow:

1. Changes in the supply of savings (loanable funds) cannot possibly explain the secular decline in the natural rate of interest r*.

2. To the extent that higher income inequality increased household savings, this did not lead to an increase in (aggregate) national savings, because other sources of savings (notable, public savings and foreign savings) declined. This is not surprising, because the higher average household savings depressed demand and economic growth, lowering public and foreign savings as a result.

3. The secular decline in the natural interest rate r* cannot, therefore, in any way be attributed to rising income inequality.

The key proposition of Mian, Straub and Sufi (2021) holds no water.

Figure 4 Aggregate national savings and the natural rate of interest: U.S. (1961-2019)

Second problem: the rate of time preference of most U.S. households increased rather than declined

Mian, Straub and Sufi (2021) calculate the natural rate of interest r* using the model of Laubach and Williams (2003). They determine r* as a function of potential output — the level of output supposedly consistent with stable inflation. I must note here that there is absolutely nothing ‘natural’ about r* — its value depends on the magnitude of the inflation target, set by the central bank, and also on the central bank’s understanding and measurement of ‘potential growth’. This unobservable concept is known to be slippery in the extreme (see Costantini 2015; Fontanari, Palumbo and Salvatori 2021). The argument is really that r* is just the interest rate which the central bank believes to be consistent with keeping inflation stable at its chosen inflation target.

Without much formal ado, Mian, Straub and Sufi next interpret the secular decline in r*, which is what they find (see Figure 4), within the context of the standard representative-agent Ramsey model. They do so in order to be able to give a ‘micro-founded’ explanation of the puzzle of rising household savings and a declining r*. In the Ramsey model, r* is a function of the ‘rate of time preference’ of the rational (optimizing) representative agent.[i] Hence, Mian, Straub and Sufi argue that the decline in r* (for the U.S.) could only have occurred due to a steady decline in the rate of time preference of the average U.S. household. A lower rate of time preference means that the preference of the representative agent to consume today has become less strong. As a result of this change in one of the deep behavioral parameters of average consumer behavior, the representative agent will increase her savings rate. It needs no elaboration that this ‘explanation’ involves a leap of logic because the Ramsey model has only one representative household and cannot tell us anything useful about the impact of higher inequality (between various income classes) and r*.

But things get worse. I do not see how the above reasoning why r* decreased helps explain the actual increase in savings of U.S. households. After all, the empirical evidence of Mian, Straub and Sufi shows that the increase in the average saving rate of U.S. households is caused by a significant change in income distribution in favor of the higher-saving top 10% of households, and not by a fundamental change in some deep parameter of household behavior, which then led to increases in the saving rates of the three income classes. In fact, Professors Mian, Straub and Sufi (2021, p. 21) write that “the saving rate of the top 10% group in the post-period is similar to the pre-period. [….] the saving rates of the bottom 90% fall considerably” (italics added).

This is shown in Table 1. The average annual saving rate of the bottom 50% of U.S. households declined by 9.4 percentage if one compares the periods (1963-82) and (1995-2019); their saving rate is negative (-6.8%) in the recent period. The average annual saving rate of the middle 40% of U.S. households declined by 3.8 percentage points between the two periods, whereas the saving rate of the richest 10% remained more or less unchanged.

Table 1

Saving rates by income groups, U.S. (1963-82/1995-2019)

| saving rate

(1963-1982) |

change in

saving rate |

saving rate

(1995-2019) |

|

| Top 10% | 0.253 | 0.007 | 0.260 |

| Next 40% | 0.082 | —0.038 | 0.044 |

| Bottom 50% | 0.026 | —0.094 | —0.068 |

Source: Mian, Straub and Sufi (2021), Table 1.

Hence, in terms of the concocted logic of the Ramsey model, this must mean that the rate of time preference has remained unchanged for the top 10% of U.S. households, while it must have strongly increased for the other 90% of U.S. households.[2] Oddly, Professors Mian, Straub and Sufi conclude that the rate of time preference of the representative household has declined. This shows that invoking the Ramsey model to make one’s argument look more ‘scientific’ is not without risk — because the representative household turns out to be not so representative after all.

Anyway, the fact that the average saving rate of U.S. households increased in recent times is not disputed. For Mian, Straub and Sufi, it follows that the natural interest rate r* must have fallen to allow the transformation of the higher savings into higher investment. This final step in their argument brings us, therefore, to the market for loanable funds — where savings constitute the supply of funds and the demand for loanable funds comes from business investment. The argument by Mian, Straub and Sufi boils down to a conventional ‘savings glut’ narrative, with the narrative twist here being that the glut is caused by higher income inequality.

Final problem: the loanable funds market does not exist

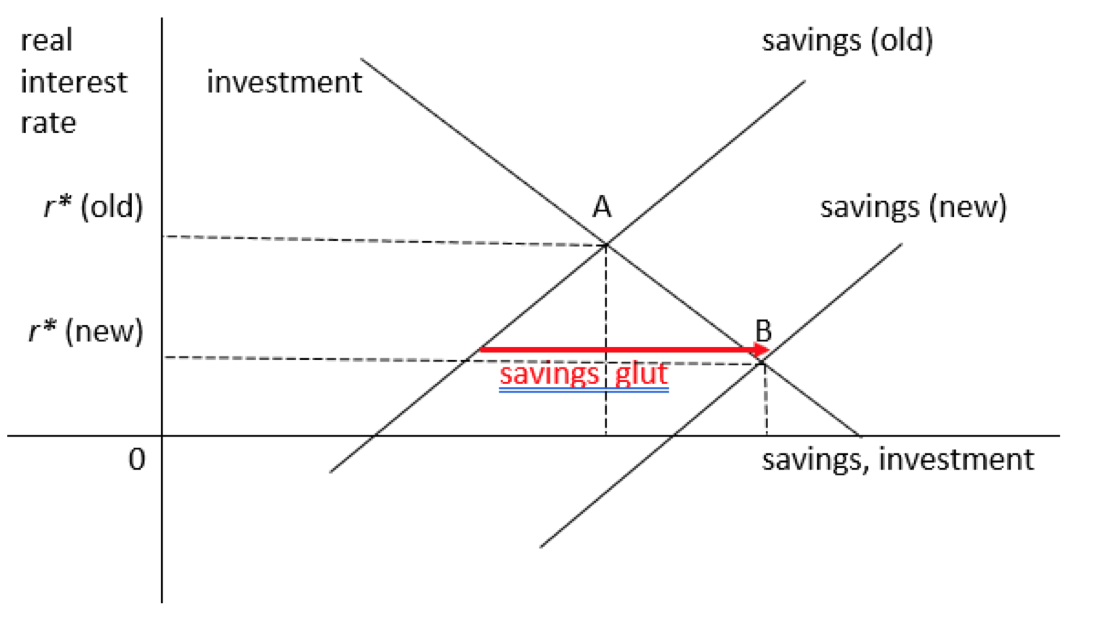

In my view, the biggest problem with the argument of Professors Mian, Straub and Sufi (2021) concerns the claim that a glut of savings causes the natural interest rate r* to fall. The simple (but incorrect) idea is that an excess supply of savings (relative to investment demand) must lead to a decline in the ‘price’ of savings, which in this story is the interest rate. Savings constitute the supply of loanable funds, while investment represents the demand for loanable funds, and similar to the market for potatoes or wooden shoes, an excess supply depresses the market price. This ‘market for loanable funds’ is illustrated in Figure 5: the curve for the supply of loanable funds shifts to right (because savings increase, at a given rate of interest, because of rising inequality), and the new equilibrium interest rate r* is lower than before. If this sounds like J. B. Say, it’s because it is. Because all savings (in this story) are converted into investment, equilibrium interest rate r* ensures that the economy is operating at its potential; hence, r* is labeled the ‘natural rate of interest’.

Figure 5 The fictional loanable funds market: savings glut

Through textbooks and papers published in the so-called top journals, the loanable funds model has been hard-wired into the belief system of most economists, even if it was shown to be a myth already more than eighty years ago by John Maynard Keynes (1936). The utter irrelevance of the loanable funds model for our monetary production economies is explained more recently by Lindner (2015), Taylor (2016), and Storm (2017). Suffice it to say that (business) investment is not financed by (already available) savings, but by (newly created) bank credit, and the volume of bank credit depends on banks’ ability and willingness to provide credit; crucially, banks are not just intermediaries pushing around existing money, but money-creating institutions which can make new money ex nihilo — a point both the Fed and private banks understand very well, as their behaviour during bailouts shows. Pointing out the loanable funds fallacy, Keynes wrote in “The Process of Capital Formation” (1939): “Increased investment will always be accompanied by increased saving, but it can never be preceded by it. Dishoarding and credit expansion provides not an alternative to increased saving, but a necessary preparation for it. It is the parent, not the twin, of increased saving.”

In sum, trying to make sense of their empirical findings on inequality and household savings for the ‘real world’, Professors Mian, Straub and Sufi end up telling us a completely fictitious story of a non-existing non-representative agent who for some unexplained reason lowers her rate of time preference and raises her savings, with the ultimate result that a non-existing natural rate of interest r* goes down in some fictitious loanable fund market. Some economists urge us to see economics as ‘storytelling’ (Shiller 2017), but surely the fact-and-fiction-blurring surrealism by Professors Mian, Straub and Sufi is taking this idea of a ‘narrative economics’ to an altogether different level.

An alternative, far more plausible explanation

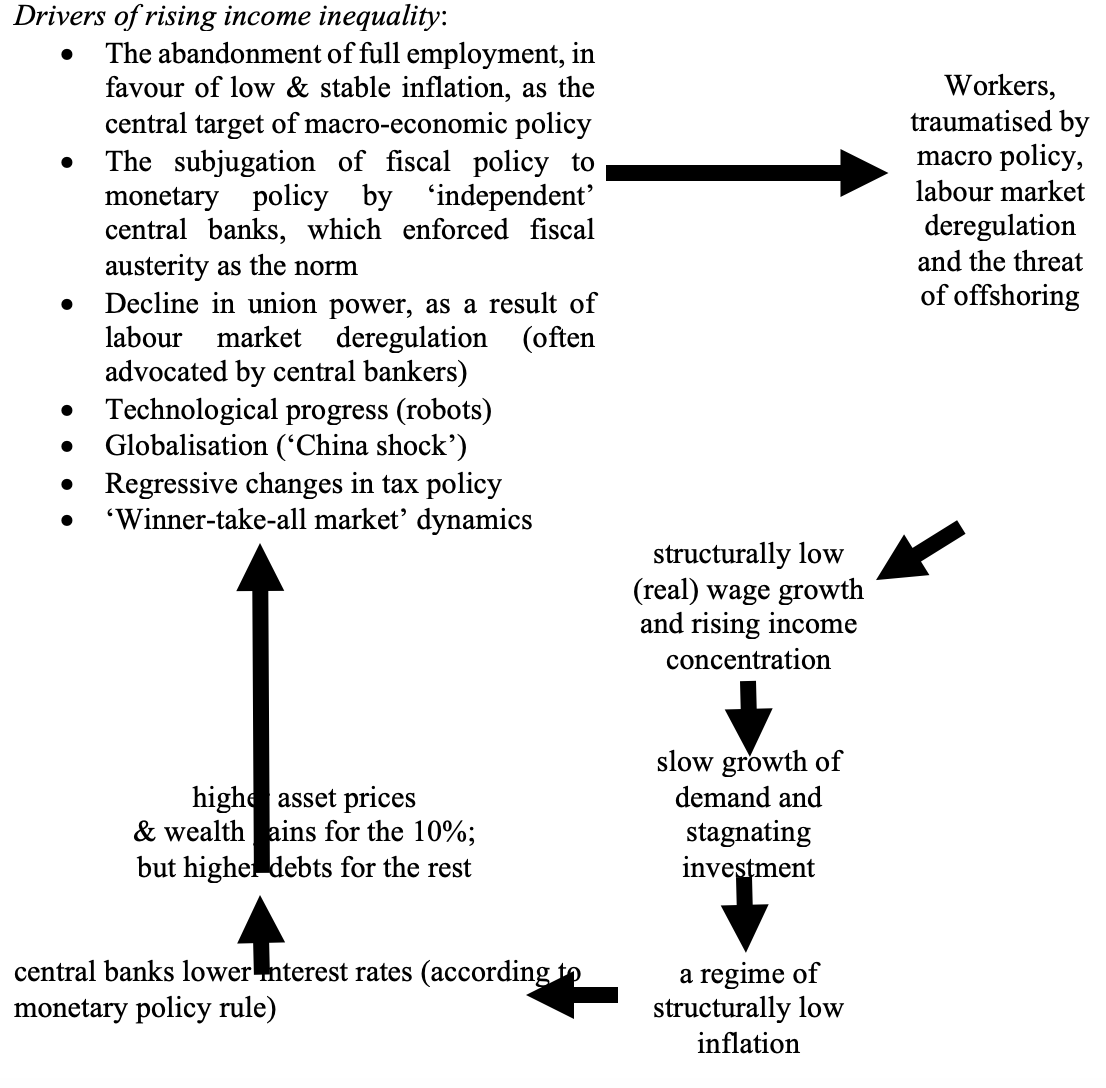

Let me conclude by offering a more plausible narrative to explain why higher inequality did cause low interest rates and over-inflated asset prices. The alternative explanation is shown in schematic form in Figure 6.

The key driver of rising income inequality is the stagnation of real wage growth for the bottom 80% or so of U.S. households (Taylor and Ömer 2020). Real wage growth was suppressed below labour productivity growth, and this led to a secular decline in the share of wages (and a rise of profits) in national income. The main cause of the wage growth suppression has been the abandonment of full employment as the primary target of macro policy-making, in favour of inflation control, at the end of the 1970s. Fiscal policy was deprioritized in favor of monetary policy, conducted by independent central banks, single-mindedly focused on building credible reputations as inflation hawks, and counter-cyclical fiscal stabilization was made anathema by subjecting fiscal policy-making to rigid and deflationary rules, irrespective of the business cycle. For a period of time after the global financial crisis of 2008, austerity zealots, dreaming of expansionary fiscal consolidations, intensified the fiscal repression, bringing about one of the slowest and most costly economic recoveries from a crisis in history.

Labour markets were enthusiastically deregulated, with the explicit and generous approval of central banks and governments, to break the structural inflationary power of unions and to create a flexible reserve of surplus workers with no choice but to work in temporary low-wage jobs in what is now known as the ‘gig’ economy. Globalization and offshoring contributed to breaking the countervailing power of organized workers because they offered corporations (the threat of) an opt-out possibility that was not available to workers. Taken together, the change in macroeconomic policy regime produced a structurally low-inflation economy, based on ‘traumatised workers’ in precarious jobs, who could not plausibly fight for higher wages and more secure employment conditions, given their daily struggles and the systemic biases they are facing. The wellspring of cost-push inflation had been radically removed.

Stagnant wages and incomes for the 90% mean that income (and wealth) inequality rises and that aggregate household savings go up (as shown by Mian, Straub and Sufi). Higher household savings reduce consumption demand, which holds up fixed business investment for the domestic market. In effect, aggregate demand growth stagnates, and pressures for demand-pull inflation evaporate. With inflation (and expected inflation) being low in structural terms, central banks lower the interest rate, in accordance with the recommendations based on the monetary policy rules proposed by establishment economics.

The low interest rates, in turn, fuel asset-price bubbles, creating wealth gains for the rich, and over-indebtedness for the bottom 90% of households, which use cheap credit to finance essential expenses on education, medical care and housing. This reinforces wealth and income inequalities, and pushes up asset prices even more, but this does not lead to higher economic growth and better jobs, because the richest 10% use their savings and wealth gains not for investments in the real economy, but to speculate in financial markets. The past two decades have made it abundantly clear that the gains made by the top 10% in financial markets do not trickle down to the real economy.

Figure 6 An alternative, more plausible explanation of high inequality and low interest rates

The low interest rate is, therefore, not a ‘natural’ rate at all, but a highly un-natural rate, which is imposed on a stagnating and highly unequal economy by central bankers who have no reason to raise rates (since structural inflation pressures have been eroded) but who cannot lower them further (because of the zero-lower bound). More than a decade ago, central bankers reached the end of the road when it comes to interest rate policy, and they were left with the option to revive the real economy by means of unconventional QE. In the present system, and given establishment thinking, this was probably the only — and therefore best — option left to central bankers, but while QE did succeed in preventing another crisis and keeping the economy on life-support, it failed to revive the real economy and enhanced the already considerable asset-price inflation. Monetary policy-makers find themselves in a catch-22, and they have themselves to blame for this.

So, what is the way out of the impasse, if there is one? The only way involves a rethinking of the dominant macroeconomic model, a reprioritization of full employment as the prime target of macro policy, and a return of active fiscal policy, supported (but not constrained) by monetary policy. Higher wages, progressive redistribution (not just of income, but also of wealth), and more public spending, financed by progressive taxes and generating balanced-budget multiplier effects, constitute essential ingredients in any sensible macroeconomic strategy.

Macroeconomists must give up the fatalism implied by using concepts such as the ‘natural’ rate of interest or the ‘natural’ unemployment rate. Central bankers cannot hide behind such metaphors and diminish themselves to being mere “drivers on a highway who must adapt their speed to road conditions.” There is nothing ‘natural’, inevitable, or preordained about economic concepts, as these are all social constructions. There is nothing natural about the current Catch-22, which was created with the active help of monetary policymakers and establishment economists, who try to shift responsibility on what they label ‘natural forces’. Instead of the fatalism of establishment economics, we must return to the work of economists who did not evade responsibility and used economic thinking to understand the world and to improve it.

Be the first to comment