We are currently following the policy of a failed programme to stop inflation. Inflation stopped, but the economy was trashed.

Steve Keen is a Distinguished Research Fellow, Institute for Strategy, Resilience & Security, UCL

Cross-posted from Steve’s Blog

In my first column in this series, I gave Hyman Minsky’s explanation of what caused the stagflation of the 1970s—a credit bubble bursting when the economy was absolutely at its peak caused the stagnation, while high wage and oil price rises caused the inflation. I finished with the essence of Milton Friedman’s very different explanation: that it was due to the government trying to push the unemployment rate below the natural rate by increasing the money supply too quickly.

I’ll go into Friedman’s argument in more detail here, not for its historical interest, but because an essential part of it—the concept of “inflationary expectations”—still plays a major role in how Central Banks think they can control the economy.

One key belief of Friedman’s was that the economy had a natural rate of unemployment, to which it would return after any shock. Another was people held money primarily to make transactions, so that the cash people held was proportional to the level of output:

If we identify the money in our hypothetical society with currency in the real world, then the quantity of currency the public chooses to hold is equal in value to about one-tenth of a year’s income, or about 5.2 weeks’ income. That is, desired velocity is about ten per year.

Friedman treated the velocity of money as a constant, so if the amount of money rose, then so would the level of transactions. He imagined an economy with a constant population, and no technological progress, in which there were 1,000 $1 bills:

All money consists of strict fiat money, i.e., pieces of paper, each labelled “This is one dollar.” To begin with, there are a fixed number of pieces of paper, say, 1,000.

Given the 10 to 1 ratio between the money stock of $1,000, and the level of economic activity, this meant that, in equilibrium, GDP would be $10,000 per year. Then Friedman imagined an event which would disturb this equilibrium. Have you heard the phrase “helicopter money”? It made its first appearance in this paper:

Let us suppose now that one day a helicopter flies over this community and drops an additional $1,000 in bills from the sky, which is, of course, hastily collected by members of the community.

This would increase the amount of money people held from 1/10th of a year’s income to 1/5th. Since people were now holding twice as much money as they wanted, they would attempt to get rid of the excess by spending more. This could cause a temporary increase in real activity as people interpreted the increase in money demand as an increase in real demand, but ultimately the economy would settle back into its long-run equilibrium. Prices would double, but there would be no change in real output or employment.

Friedman extrapolated this to a continuous increase in the money supply by imagining a continuous stream of helicopters:

Let us now complicate our example by supposing that the dropping of money, instead of being a unique, miraculous event, becomes a continuous process, which, perhaps after a lag, becomes fully anticipated by everyone. Money rains down from heaven at a rate which produces a steady increase in the quantity of per cent per year money, let us say, of 10 per cent per year.

Friedman reasoned that this would result in prices rising at 10 per cent per year. The economy would be in long run equilibrium, with supply equal to demand in every market, but with rising prices—because of “inflationary expectations”. This was a crucial part of Friedman’s argument: prices weren’t rising because of demand exceeding supply, but because of inflationary expectations:

One natural question to ask about this final situation is, “What raises the price level, if at all points markets are cleared and real magnitudes are stable?” The answer is, “Because everyone confidently anticipates that prices will rise”…

In our example, prices rise, though markets are continuously cleared, because everybody knows that they will. All demand and supply curves in nominal terms rise at the rate of 10 per cent per year, and so do the market-clearing prices.

The key to getting inflation down was therefore to reduce “inflationary expectations”. Inflation was occurring simply because people expected it, and put their prices up by that much every year—both the prices they charged for their own services, and the prices they were willing to pay for others.

That could be done simply by reversing the previous policy: reduce the rate of growth of the money supply. This would initially cause a small recession, but once people realised that only nominal—rather than real—demand had fallen, the economy would converge back to the equilibrium rate of growth with a lower level of inflationary expectations. Relatively painlessly, the economy could be restored to a low inflation environment.

This is the policy that Federal Reserve Chairman Volcker put into motion in 1979. He put up the Federal Funds Rate to 20% in an attempt (to quote Volcker from the Fed’s minutes in his first meeting as chairman) to reduce inflationary expectations:

I do believe that we have to give some attention to whether we have the capability, within the narrow limits perhaps in which we can operate, of turning expectations and sentiment. I am thinking particularly on the inflationary side. [Can we] restore the feeling that inflation will decline over a period of time and that that’s a prime objective of ours?

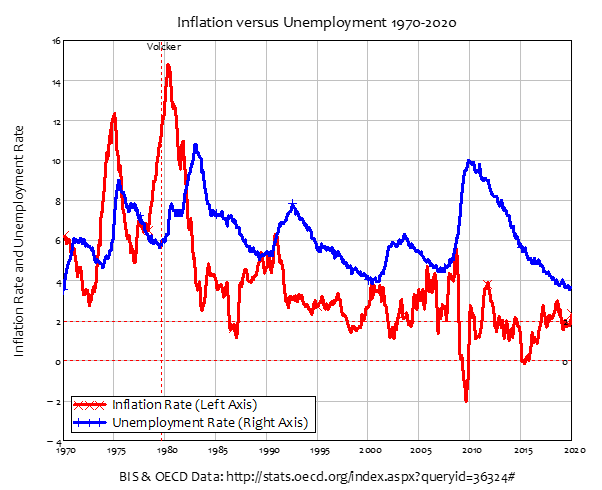

Volcker’s actions did cause the rate of inflation to fall. However, this was not via a relatively painless fall in “inflationary expectations”, but by a savage recession, the deepest the USA had experienced since the Great Depression. Inflation fell from 15% at its peak to below 2% by 1987, but unemployment rose just as sharply, from under 6% when Volcker started to increase interest rates, to almost 11% when inflation had fallen to just above 2%.

Figure 1: Chart comparing inflation to unemployment for the 50 years before Covid

The economic collapse took the wind out of both wage rises, and the price of oil. Wage rises, which peaked at 11% per year in 1981, fell to 4% per year in 1983. Oil prices, which had risen from $15 to $40 a barrel in 1980, fell gradually to $30 in 1985 and then plunged to just $12 a barrel in 1986. In addition, the negative relationship between unemployment and inflation—the disappearance of which between 1973 and 1975 had played such a large role in getting Friedman’s theory accepted—was back.

To be continued…

Be the first to comment