There is an increasing demand for stricter regulation on centralised crypto exchanges

Lin William Cong is Rudd Family Professor of Management and Professor of Finance at Cornell University, Xi Li is Lecturer in Finance at ICMA Centre at University of Reading, Ke Tang is Professor and Director of the Institute of Economics at Tsinghua University, Yang Yang is a blockchain researcher and business owner

Cross-posted from VoxEU

Jorge Diaz/Wikimedia Commons

Cryptocurrencies suffered substantial losses in 2022, with major currencies witnessing a decline of more than half from their peak value. There is an increasing demand for stricter regulation on centralised crypto exchanges, which handle vast amounts of investor assets, yet often lack adequate disclosure, regulated custody, and customer protection. This column describers how wash trading is a prominent issue in centralised cryptocurrency exchanges, with over 70% of reported volume on unregulated crypto exchanges consists of such trades. Regulatory actions and global standards are suggested to foster a healthy and sustainable industry

As the global economy grappled with inflation in 2022, cryptocurrencies, once touted as inflation hedges, experienced their fair share of turmoil. The total market capitalisation shrank from its $3 trillion peak in 2021 to below $1 trillion, with major currencies like Bitcoin and Ethereum losing more than 70% of their peak value. 1 This dramatic downturn was characterised by the unprecedented collapse of centralised institutions within the sector, also known as CeFi (Danielsson 2022). From Three Arrow Capitals to Voyager, from Celsius to FTX, from Genesis to Core Scientific, whether you are a venture fund, a credit provider, an exchange, or a mining company, the market has proven that no entity is ‘too big to fail’. Every failure delt a devastating blow to millions of investors and customers around the globe.

While some argue that strict regulations infringe on the freedom and innovation in the blockchain space, there is little doubt about the need to tighten the leash on centralised cryptocurrency exchanges (Nagy-Mohacsi and Mandeng 2018, Zhou 2023). For one, successful centralised crypto exchanges have expanded into upstream and downstream sectors, evolving into complexes that encompass trading platforms, custodians, banks, and clearinghouses. Moreover, while they directly interact with every customer and often hold substantial user funds, proper disclosure, regulated custody, and insurance are often missing.

Among the issues concerning centralised crypto exchanges, wash trading stands out prominently. A wash trade is a form of market manipulation in which an entity simultaneously sells and buys the same or very similar financial instruments to mislead the market or regulators. This may be done for several reasons: for example, crypto exchanges or token projects may fake transaction volume to attract liquidity and customers (Baydakova 2019), sellers of non-fungible tokens (NFTs) may wash trade to create the impression that the assets are more in-demand than they truly are (von Wachter et al. 2022), and individuals may wash trade for tax-loss harvesting (Cong et al. 2022). Wash trading in most asset classes has been illegal in the US since the Commodity Exchange Act (CEA) of 1936 but remains as a grey area in the cryptocurrency sector.

Accusations of exchanges inflating their trading volume were initially speculative and anecdotal (Wong 2014). Industrial reports such as Fusaro and Hougan (2019)’s Bitwise report to the SEC fully blew the whistle and sparked extensive discussion in 2019. Nevertheless, these reports applied heuristic methodologies and their results were challenged and denied (Hill 2019) or ignored by the exchanges in question (Tamuly 2019, HitBTC 2019).

Anecdotes and industry rumours suggest that exchanges engage in wash trading in several ways. The most basic approach is to create false trading records in the trading history database, but this is easily detectable by customers and observers who monitor live trade books on exchanges’ websites. A more advanced technique is to deploy trading programmes that place fake orders into the real order book. These orders can be filled only by approved (exchange-owned) accounts or made available to the market. However, the latter approach requires greater technical expertise because it carries the risk of loss if positions are not closed in time or filled by other traders. Some exchanges also incentivise users to engage in wash trading through fee rebates or transaction-mining programmes. Additionally, exchanges can deploy wash-trading-only robots or include wash trades in other activities such as market-making or outsource it to professional market makers. They can activate or deactivate these methods as needed. Combining these actions can also be effective. Despite the complexity of the problem, wash trading has been largely neglected until several academic articles rigorously established crypto wash trading as a rampant, industry-wide phenomenon.

The most straightforward way to detect wash trades in the trading record is to identify the buyer and seller and prove that they are the same entity. However, since every operating exchange conceals traders’ identities in public trading records as a commercial secret, it is unrealistic to directly mark which transaction is a wash trade at a meaningful scale.

As the first academic study addressing the significant issues of vertically integrated crypto exchanges, we utilise a method to detect wash trading at the exchange level, without knowing the identity of each trader. The principle, commonly employed in forensic applications, is based on the concept that authentic transactions adhere to established statistical and behavioural benchmarks, while wash trades deviate from these patterns. Unless illicit traders are aware of these benchmarks and meticulously forge transactions to conform to them, they are unlikely to succeed, particularly during early sample periods. We applied Benford’s Law, rounding, and power law to examine the trading records exchange by exchange about major cryptocurrencies including Bitcoin, Ethereum, Litecoin, and Ripple.

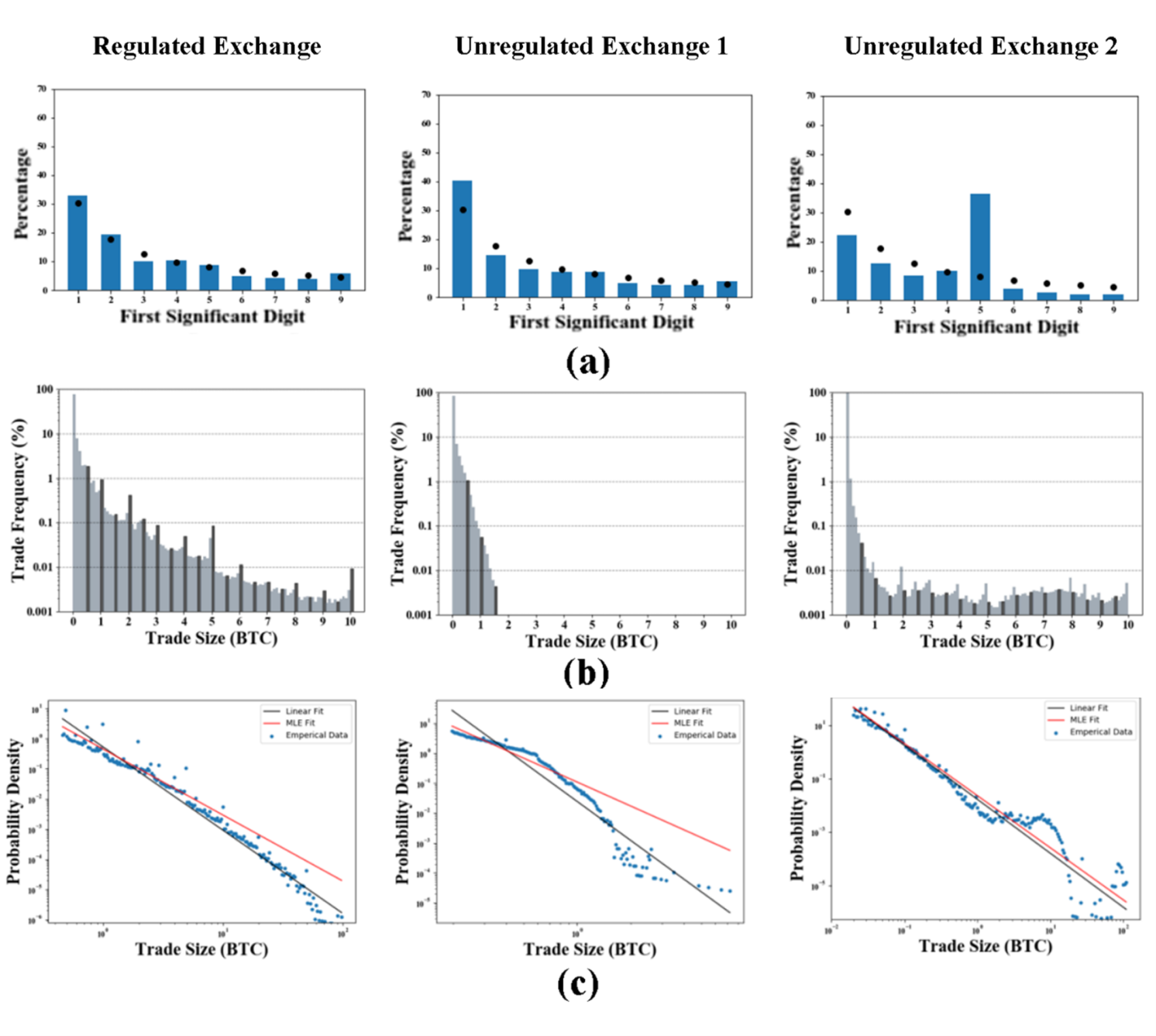

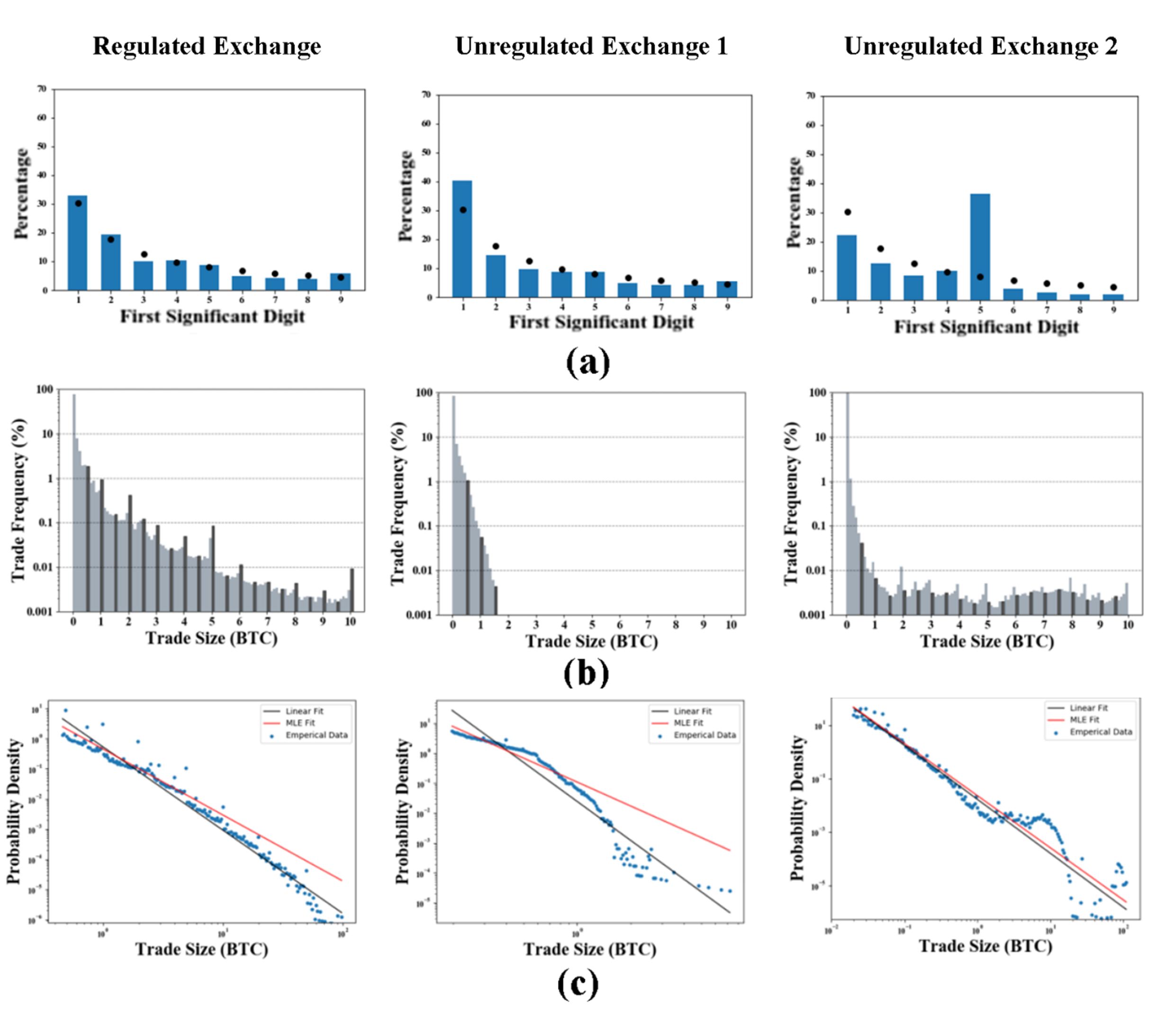

Benford’s Law is a statistical pattern that describes the distribution of the first significant digits in large datasets. It is applicable to naturally generated data in a multiplicative process, such as trading history data in regulated markets. 2 In a legitimate dataset, the digit ‘1’ will appear as the leading digit about 30.1% of the time, followed by the digit ‘2’ at 17.6%, and the probability of any digit being the leading digit decreases as the digit increases. Wash trading data typically violates Benford’s Law since it is not generated in natural multiplicative processes. Panel (a) of Figure 1 illustrates this with the abnormal bars representing the number ‘1’ and ‘5’ (in the middle and right figures respectively), which indicates that a significant amount of wash trading was conducted with ‘1’ and ‘5’ as the leading digits for the two unregulated exchanges respectively. This pattern is markedly different from the data pattern observed in regulated exchanges, which closely adheres to Benford’s Law.

The clustering effect from rounding behaviour is a classical regularity commonly observed in financial markets. 3 From a psychological perspective, several studies have found that human traders tend to use round numbers as cognitive reference points to simplify and save effort in the decision-making and evaluation process (Ikenberry and Weston 2008, Kuo et al. 2015, Lacetera et al. 2012). Therefore, in legitimate trading datasets, orders tend to cluster around round numbers in trade sizes. Wash traders are likely to use automated trading programs to mass-produce fake orders, which naturally reduces the proportion of authentic volume and results in less clustering, as seen in Panel (b) of Figure 1 where there is no significant clustering around round numbers in unregulated exchanges’ data.

Power law has been observed to capture the ‘fat tails’ of trade size distributions in regulated financial markets. 4 One possible explanation for the appearance of power-law tails in financial data is the trading behaviour of large investors who seek to avoid significant market price impacts (Gabaix et al. 2003). Other studies attribute these tails to investors’ limited information about asset values (Kostanjčar and Jeren 2013) and herding behaviour (Nirei et al. 2020). By plotting the trade size distribution on a log-log scale and fitting the data, it is possible to determine whether the trading data conforms to a power law. Results from the unregulated exchanges are showing abnormal tail distributions than the regulated ones in Panel (c) of Figure 1.

Figure 1 First-significant-digit, trade-size clustering, and tail distribution of trade size

Notes: The figure demonstrates the BTC/USD distribution drawn from sample exchanges compared with the benchmarks. Three exchanges are shown in the figure, one regulated exchange (column left) and two unregulated exchanges (column centre and right). Panel (a) are the first-significant-digit distributions and comparisons with Benford’s law. Black dots represent distributions derived from Benford’s law. Distributions of trading data are reported in bar charts. Panel (b) shows the clustering effect in trade-size distributions histograms on exchanges. In each histogram, every 5th and 10th bin are highlighted to illustrate the clustering effect around round trade sizes. Panel (c) displays tails of trade-size distributions and the fitted power-law lines on log-log plots. Fitted power-law lines are plotted with parameters estimated by Ordinary Least Square (OLS) and Maximum Likelihood Estimation (MLE), shown in black and red lines, respectively. Blue dots represent empirical data points for trade-size frequencies.

Statistical analyses were performed on all three benchmarks to confirm the significance of the results. Regulated exchanges such as Bitstamp and Coinbase exhibit normal behaviour because they are subject to regular scrutiny by authorities. In contrast, wash trades are widespread and severe among unregulated cryptocurrency exchanges. On average, it is estimated that over 70% of the reported volume of unregulated crypto exchanges consists of wash trades, with some newly established exchanges faking more than 90% of the reported volume.

It is also noteworthy that the rise of decentralised exchanges (DEX) and non-fungible token marketplaces after 2020 due to the rapid development of smart contract technology (He and Cong 2018). They were also accompanied by significant wash trading (Victor and Weintraud 2021, Cong et al. 2022). However, because trading records are mostly recorded on the blockchain, wash trades are transparent due to the nature of blockchain data publicity. Therefore, wash trading in decentralised exchanges and non-fungible token markets is arguably less misleading and harmful than in centralised exchanges and is easier to detect.

After confirming the widely existing wash trading behaviour in unregulated exchanges, we explore the incentives and factors that determine wash trading, as well as its implications. The most likely incentive for exchanges to engage in wash trading is to increase their rankings on popular web portals to attract customers. Therefore, it is not surprising that newly established and less prominent exchanges engage in more wash trading. They tend to increase wash trading volumes when the market experiences recent positive returns or decreases in volatility in the past one or two weeks.

We have shown that crypto exchanges did not seem to be aware of statistical scrutiny when they committed wash trading in the past. Therefore, we urge regulatory authorities and industry self-regulatory bodies to take actions on the wash trading problem and establish global standards. This is technically feasible with regularly published data and forensic tools. While some may worry that exchanges could implement related statistical characteristics in their wash trading matrix after studying the research, it is not a significant problem because fraud detection and frauds are in a constant race. Following the research, other researchers have proposed different tests to enhance the forensic tools against wash trading (Amiram et al. 2022, Le Pennec et al. 2021, Chen et al. 2021, Aloosh and Li 2021). With mature regulation and constantly developing forensic tools, it will eventually become uneconomical for exchanges to engage in wash trading.

Be the first to comment