For Howell, financial flows and the risk-taking behaviour of investors drive the real economy and asset prices, not vice versa.

Michael Roberts is an Economist in the City of London and prolific blogger

Cross-posted from Michael Roberts Blog

We’ve had the argument that the major global issue of the 21st century is the growing trade and technology war between the US and China. In their book, Trade Wars are Class Wars, Klein and Pettis reckon that the trade imbalances are cause by inequality and income and consumption in the two powers: China has ‘excess savings’ and the US has ‘excess consumption’. I have argued that this argument is false in previous posts.

Now we have Capital Wars as an alternative scenario for the rivalry between China and the US. The rivalry between the US and China in the economic sphere has so far been on trade and technology. There has been little comparable friction in financial markets. Indeed, as more Chinese stocks are incorporated into global indices, US investors have been pouring capital into China via their investment in index-tracking funds.

Yet that is unlikely to last, according to Michael Howell, a former research director of investment bank Salomon Brothers who now runs his own ‘boutique’. In Capital Wars he points out that the swap lines extended by the US Federal Reserve to other central banks after the 2008 financial crisis — an exercise repeated since coronavirus struck — have been extended to friendly nations, while China has been pointedly excluded. So the Fed’s role as a global lender of last resort has been both partial and politicised.

Howell reckons the nature of the relationship between these two powers is unbalanced. Despite its declining share of global output, the US is the main provider of the dominant reserve currency to world markets. But its economy is marked by low productivity growth along with highly developed financial markets. China has enjoyed high productivity growth as it catches up, but it has underdeveloped financial markets. Persistent trade surpluses have contributed to a huge accumulation of foreign exchange reserves: the majority is in dollar assets. All this creates a fractious interdependence.

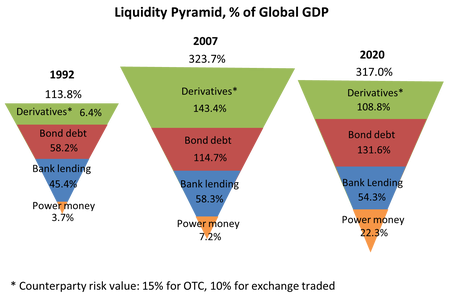

China’s economic rise coincided with a long period of liberalisation in international financial markets. A central theme of Howell’s book is the ballooning of global liquidity — gross flows of credit, savings and international capital that facilitate debt, investment and cross-border capital flows. In 2019, this international pool of funds was estimated at $130tn, two-thirds larger than world GDP. China’s contribution was close to $36tn.

There is nothing new in Howell’s insight here. Indeed, several authors, including myself, have pointed out the huge rise in ‘liquidity’ ie money supply, bank credit, debt (both public and private) and debt instruments like derivatives, particularly since the early 2000s.

What is new is Howell’s emphasis on what new ways the financial system has found to expand what Marx called ‘fictitious capital’, ie financial assets supposedly representing future new value and profits. Whereas banks used to rely on customer deposits to lend and speculate with; now the chief source of funds is not deposits, but repurchase agreements or ‘repos’, a form of borrowing that has to be backed by ‘collateral’ in the form of “safe” assets such as government bonds.

Howell argues, like others, that the financial system has moved from the post-war model, where banks were the main facilitators in lending. They borrowed from their retail depositors and lent to individuals and companies. Today, wholesale markets predominate; and the main providers of funds are financial institutions and large companies such as Apple or Toyota. Users range from companies and banks to hedge funds and governments: non-bank finance or ‘shadow banking’.

Howell’s main argument is that the chief source of instability in the modern financial system has been a shortage of safe assets for these liquidity creators to hold as there was not enough government debt and the return was low anyway. Indeed, before the 2008 financial crisis, investment bankers tried to invent new ‘safe assets’ such as collateralised mortgage obligations. Of course, we now know that such assets were not ‘safe’ at all, but nothing but a giant Ponzi scheme of credit that turned out to be very ‘fictitious’ indeed in the global financial meltdown in 2007-9.

The question that Howell hints at is whether the huge injection of credit money by the Federal Reserve and other central banks to bail out companies and governments in the COVID pandemic slump will lead to a similar financial ‘shock’ in due course. The difference now is that it is the state that is buying up these ‘safe assets’ directly, rather than the banking or shadow banking system as in 2008-9. Nevertheless, the size of central bank purchases of corporate and mortgage bonds, as well as government paper is so huge that, if there were to be substantial explosion of bankruptcies, the lender of last resort (central bank) – now turned into the first buyer for fictitious capital – may end up with huge losses for governments to absorb.

One merit of Howell’s book over others of the same ilk is that he offers an explanation of why there was this drastic change from ‘traditional banking’ to the ‘financialisation’ of government and corporate assets. He puts the cause squarely at the collapse of profitability in the productive sectors of the economy.

Howell reckons that falling profitability in industrial capital led to rising global ‘liquidity’ and this contributed to declining interest rates across risk assets, leading to the search for safe financial assets beyond government debt and into ‘repos’, to the detriment of productive investment.

Here Howell half grasps the story of the 30 years leading up to the global financial crash and the Great Recession. Unfortunately, despite referring to Marx’s analysis on occasion, Howell does not use it. Instead he falls back on the usual Keynesian macro-identities to explain why crises occur. Thus, as with all Keynesian macro identities, profits disappear from the equations.

Howell takes the basic identity: savings = investment and revises it into his key equation: Liquidity = fixed investment plus the net acquisition of financial assets. Liquidity is really profit plus credit in its various forms. But for Howell, the driving force of modern capitalism is not the profit part of ‘liquidity’, however, -that’s old hat. It’s the credit part. For him, financial flows and the risk-taking behaviour of investors drive the real economy and asset prices, not vice versa. More liquidity leads to more purchases of financial assets. And more purchases of financial assets require more liquidity. Thus, we move from a view of capitalism as a mode of production for profit, to capitalism as a mode of financial speculation and financial instability. This theory is akin to the Minsky approach and the modern ‘financialisation’ theories.

For Howell, the coming war between the US and China will be fought not so much through trade or technology, but through financial flows and the control of international currencies as rival powers struggle to offer the ‘safest’ financial assets to global capital: eg the dollar or the renminbi?

There is clearly some truth in this. If China were able to offer a strong and liquid currency to replace the dollar, US imperialism would be in serious trouble. But a strong currency cannot be ‘created’ by financial markets; it comes about from the relative strength of the productivity of labour and value creation in an economy. That is where the economic war is centred; with trade, technology and financial being the battle grounds. Value decides, not credit.

Be the first to comment