As the newest wave of doomsday predicitions for China is in progress, Michael Roberts analyses the options China has

Michael Roberts is an Economist in the City of London and a prolific blogger

Cross-posted from Michael Roberts’ blog

In Q2 2023 the Chinese economy expanded by 6.3% year-on-year, up from 4.5% yoy recorded in Q1. Sounds strong, but quarterly growth was only 0.8%, slowing sharply from 2.2% qoq in the first quarter of 2023.

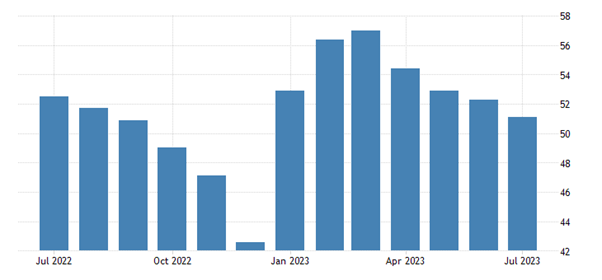

And a reliable measure of economic activity, the purchasing managers survey index for July, was down to 51.1 in July 2023 from 52.3 in the previous month (50 is the threshold between expansion and contraction). This was the lowest figure since December 2022. Factory activity contracted for the fourth month in a row.

The West’s China ‘experts’ have been quick to argue that the Chinese economy is in deep trouble, with slowing growth, falling exports, weak consumption growth and rising debt. The great economic miracle is over.

But how many times have we heard this refrain from the experts over the last 20 years? I could cite article after article, book after book, predicting the collapse of China’s state-led economy, ranging from the claim that it is locked into a ‘middle-income trap’ (ie cannot grow fast again); that an ageing population and falling workforce, alongside rising public and private sector debt, is leading to ‘Japanification’ ie a stagnant economy; and finally to forecasts of an imminent collapse in the property and finance sectors.

I have dealt with these arguments in detail in many previous posts. The last one was only in March. Please read that for chapter and verse and the previous posts cited. The data are all there, refuting this ‘expert’ analysis. But of course, it won’t go away because it is in the interests of ‘the West’ to claim that Chinese economic model cannot work and it needs urgently to make a transition, not to socialism, but to outright free market capitalism.

Let us consider the latest round of claims being put by mainstream economists (and parroted by some inside China, ie those who were nicely educated in neoclassical, free market economics in American universities). For example, here is the latest view of the Financial Times. “Government policy is largely to blame for the slowdown. Decades of relying on an investment-driven growth model has slowed China’s transition to a consumer-based economy. Poor oversight of the housing market led to an unsustainable lending boom, while political impediments have hamstrung private enterprises. Heavy-handed Covid restrictions have also left deep scars.”

So first, let’s blame the Chinese government for the slowing economy – presumably for interfering in business and the capitalist sector. But then claim that “decades of relying an investment-driven growth model” is at fault because what is needed is a “transition to a consumer-based economy”. Really? Have the consumer-based economies of the G7 done better than the awful investment-led Chinese economy in the last two or three decades? Take a look at this graph below.

But the FT and other experts might retort, since COVID things have changed in China; now the economy cannot recover. Really? Look at this graph on the growth rate of China and the US since the COVID pandemic started. Indeed, during the COVID pandemic slump year of 2020, every major advanced capitalist economy suffered a recession, but, as in the Great Recession of 2008-9, China did not. And yet China applied the most stringent and draconian series of lockdowns during the pandemic.

And while the US economists are in rapture over 0.6% growth in the US economy in Q2 this year, apparently 0.8% growth for the same quarter in China is to be considered a disaster.

The FT says that “heavy-handed Covid restrictions have also left deep scars.” Well, those ‘heavy-handed’ measures also saved millions of lives in China, when its health system was at breaking point and inadequate to the task. During 2020-21, when the COVID death rate rocketed in the West, China’s stayed at miniscule levels. Eventually, as lockdown exhaustion emerged and protests rose, the government relented and ‘opened up’ the economy, the death rate rose – but only to 85 per million compared to 3300 per million in the US, or to ‘open’ Sweden at 2325 and or even India at 375 (ludicrously underestimated). The ‘deep scars’ were and are still being felt in Europe, the US and Latin America from COVID deaths and long ‘COVID’ on the health of the workforce and economic growth. This year, the IMF forecasts China will grow 5.3%, while the advanced capitalist economies will manage only 1.5%, with the Euro area reaching only 0.9% and Germany and Sweden in outright recession.

The FT goes on that “Poor oversight of the housing market led to an unsustainable lending boom, while political impediments have hamstrung private enterprises.” Much noise has been made about the property crash in China, with several mega-property development companies going bust as the debt borrowing that they built up could no longer be serviced from property sales.

But was this down to poor regulation? We have heard the same cause presented in the property busts in capitalist economies – that it was ‘badly regulated’. But as in those economies, China’s property crisis is not because of bad regulation or ‘unsustainable lending’ but because the housing and property market in China is just that – part of the speculative capitalist market. To quote, Xi himself: ‘housing is for living not speculation’.

And therein lies the rub. Why was a basic human need, housing, handed over to the private sector to meet the needs of millions flooding into the cities over the last few decades? Housing should be done by direct public investment to build houses for all at reasonable rents and so avoid speculation, rocketing house prices and widening inequality. Indeed, the biggest reason for rising inequality in China in the last two decades was not billionaires but the inequality between urban and rural areas and property and non-property owners.

It’s what happened in the West; China should have avoided that too. But in their ‘wisdom’ the Chinese leaders, as advised by their Western-educated bankers and economists, opted for the rentier-capitalist model, which now has come back to bite them.

The government has been forced to act. First, with its “three red lines” policy introduced in 2020, it aimed to limit borrowing by developers and ultimately curtailed their access to financing. Then it started to bail out developers and take over some. But huge debts remain in local government which bore the burden of providing land to these developers and raising funds. Local government debt has spiralled and the oncoming repayment schedule is high.

Local government debt now stands at around 25% of GDP, but if you add in the financing vehicles set up by local governments (LGFVs), then total local government debt is more like 60% of GDP. Worse, faced with tighter credit criteria at home, LGFVs turned to offshore markets and raised a record $39.5 billion in dollar bonds.

I am afraid that the Chinese leaders have not learnt from this. They are now moving to provide easier credit for developers and have dropped Xi’s phrase about ‘homes for living’. The government now talks of helping out the capitalist sector. Senior party and state officials jointly released a 31-point plan earlier to shore up the private economy and improve business sentiment. Various government agencies last week also outlined goals to boost consumer spending on cars and electric appliances, though no direct subsidies for households have been unveiled.

All this is along the lines advocated by the likes of the FT, which reckons that “entrepreneurs and established businesses need stability and regulatory clarity from the government. Further monetary policy loosening by China’s central bank could help. Beijing will also need to restructure its local government debt; one option might be a fire sale of state assets to private companies. The proceeds would help local authorities to avoid a debt crisis.” In other words, the answer is not public ownership of the housing sector and taking over the indebted property companies, but instead a bailout and then a sale of state assets to pay for it ie privatisation not nationalization.

Finally, in its claimed demise of the Chinese economy, the FT returns to the old ‘Western expert’ argument that China must become a consumer-led economy like the G7, if it is to avoid the ‘middle-income’ trap and Japanese style stagnation. But it is the consumer economies of West that are stagnating, not China. Moreover, if ‘stagnation’ means no inflation of prices, then it may have merit. China has the lowest inflation rate of all the major economies in the world, including stagnating Japan which is desperately trying to create inflation!

While households in the West are suffering the biggest fall in living standards since the Great Depression because wages are not keeping up with high inflation, it is the opposite in China.

What is an issue is youth unemployment which is over 20% in China compared to average urban unemployment of around 5%.

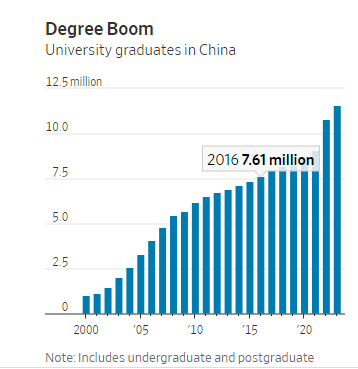

The problem isn’t that jobs don’t exist in China. They do. But the economy isn’t producing enough of the high-skill, high-wage jobs that many college students have come to expect. China is producing more and more university graduates.

But they all expect to get jobs in finance and technology, but not in manufacturing, construction and engineering. It’s a problem that has affected not just China, but also the West. Better-off families want their kids to be working for glamorous tech firms and banks (where they have to work ridiculous hours) rather than in any ‘mundane’ work that often can pay just as much. The government has offered incentives to companies take on students but it does not plan government projects that could provide training in tech and innovation that could meet important social targets.

Then there is external trade. One reason that China’s growth rate has been relatively low in the last year is the collapse of international trade which has turned negative. As a result, China’s exports to the world have dropped.

Yes, that probably means China should concentrate on domestic investment and output, not exports. But that does not mean becoming a ‘consumer-led’ economy. As I have argued before, consumption flows from investment not vice versa – as China’s economy up to now has proved.

The FT and the other experts argue that China is heading for low growth through this decade – see the IMFs latest forecasts.

But as I have argued in previous posts, that does not follow if China uses the potential it still has to invest and grow. Some ‘experts’ are now claiming that India will usurp China over the next decade. But as ex-World Bank and IMF economist Ashoka Mody puts it:

“Since the mid-1980s, Indian and international observers have predicted that the authoritarian Chinese hare would eventually falter and the democratic Indian tortoise would win the race.”

But the World Bank’s 2020 Human Capital Index – which measures countries’ education and health outcomes on a scale of 0 to 1 – gave India a score of 0.49, below Nepal and Kenya, both poorer countries. China scored 0.65, similar to the much richer (in per capita terms) Chile and Slovakia. While China’s female labour-force participation rate has decreased to roughly 62% from around80% in 1990, India’s has fallen over the same period from 32% to around 25%. Especially in urban areas, violence against women has deterred Indian women from entering the workforce.

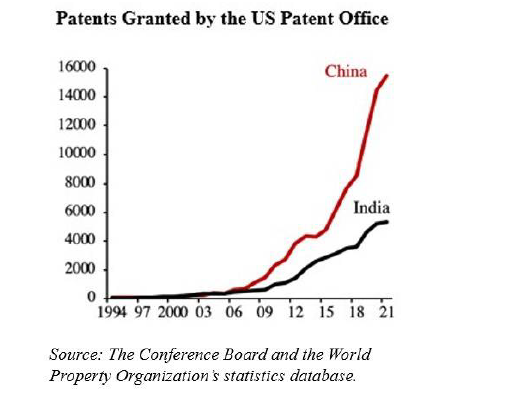

Assuming that the two economies were equally productive in 1953 (roughly when they embarked on their modernization efforts), China became over 50% more productive by the late 1980s and today, China’s productivity is nearly double that of India. While 45% of Indian workers are still in the highly unproductive agriculture sector, China has graduated even from simple, labour-intensive manufacturing to emerge, for example, as a dominant force in global car markets, especially in electric vehicles.

China is also better prepared for future opportunities. Seven Chinese universities are ranked among the world’s top 100, with Tsinghua and Peking among the top 20. Tsinghua is considered the world’s leading university for computer science, while Peking is ranked ninth. Likewise, nine Chinese universities are among the top 50 globally in mathematics. By contrast, no Indian university, including the celebrated Indian Institutes of Technology, is ranked among the world’s top 100.

China still has vast opportunities for infrastructure in its interior provinces. The challenge is turn domestic savings into domestic investment, so capital is allocated to its most productive uses. For me, that means the state must direct the allocation and not leave investment to the capitalist sector to deliver.

Indeed, the capitalist sector in China is failing. The private-sector’s share of China’s 100 largest listed companies by market value dropped from a peak of 55% in mid 2021 to 39% this June, close to its lowest levels in more than three years, according to a forthcoming research report by the Washington, D.C.-based think tank Peterson Institute for International Economics, or PIIE.

Private sector investment shrank by 0.2% in the first half of 2023 from a year earlier, the first contraction since official data collection began in 2005, with the exception of 2020, when the economy was racked by the pandemic. In contrast, investment by state-controlled firms expanded 8.1% in the same period.

The FT makes a point: “China’s central government is one of the least indebted in the world… If China is to sustain its long run of economic success, it is down to Beijing to act.” But the FT’s idea of action is for government to make cash handouts to households and ‘free up’ the private sector. But it’s not a turn to a consumer-led market economy that China needs to get the economy going again, but planned public investment into housing, technology and manufacturing.

Be the first to comment