Little to be joyful about in France today

Michael Roberts is an Economist in the City of London and a prolific blogger

Cross-posted fromMichael’s Blog

The second round of the French presidential election returned the incumbent President Emmanuel Macron to a second term of office. Macron won with 58.5% of the vote against the opponent, Marine Le Pen of the right-wing nationalist National Rally, who got 41.5%. Sounds comfortable – but the voter turnout of 72% was the lowest since 1969. Moreover, Le Pen did better than in 2017, showing that Macron’s neoliberal policies of cutting pensions, reducing the health service and ‘liberalising’ the labour market have not been received well by a sizeable body of the electorate. In the first round, Macron polled only 28% of those voting, or about 21% of those eligible to vote, while Le Pen took 23%. Left-wing candidate Jean-Luc Melenchon polled 22% and nearly made the run-off, despite the ecology and other socialist candidates splitting the vote. Melenchon’s supporters abstained in large numbers in the second round, some voted for Macron, but few for Le Pen.

Basically, France is split three ways politically. One-third backs a pro-EU, pro-capitalist France as represented by Macron; one-third backs a nationalist, anti-EU ‘Frexit’, anti-immigration France as represented by Le Pen; and one-third backs a socialist pro-labour France as represented by Melenchon. This fragmentation is likely to be further exposed in the upcoming parliamentary elections. It’s possible that Macron’s party will lose its majority in the National Assembly and Macron will have to appoint a prime minister and cabinet that is in opposition to his policies – a further fragmentation of French politics at a time when France is taking on a senior position in EU policy over the Ukraine conflict and sanctions against Russia.

France is a key G7 economy, the fifth largest in the world and represents around one-fifth of the Euro area GDP. In manufacturing, France is one of the global leaders in the automotive, aerospace and railway sectors as well as in cosmetics and luxury goods. It has a highly educated labour force and the highest number of science graduates per thousand workers in Europe. Its services sector is large, led by tourism and financial services. Additionally, France is one of the world’s largest exporters of farm and agricultural products and is renowned for its wine, spirits and cheeses. The French government provides significant subsidies to this sector and France is the largest exporter of farm products in Europe. France is linked closely to its largest trading partner, Germany, which accounts for more than 17% of France’s exports and 19% of total imports.

After the failure of the Mitterrand government’s attempt to sustain Keynesian policies in the teeth of a global slump in the early 1980s, successive governments have applied neo-liberal policies of privatisation, tax and welfare cuts to boost profitability – despite opposition by working-class movements and the trade unions. Governments either partially or fully privatized many national industries, including Air France, France Telecom and Renault, and today, France’s leaders remain committed to capitalism. However, the French government still plays a role in certain key national sectors, such as agriculture, and will intervene in the market to sustain certain ‘national interests’. For example, the energy companies are publicly owned and since the oil and gas price rises, were directed to hold price increases to just 4% this year, while the privatised UK companies have been allowed to raise tariffs by nearly 60%.

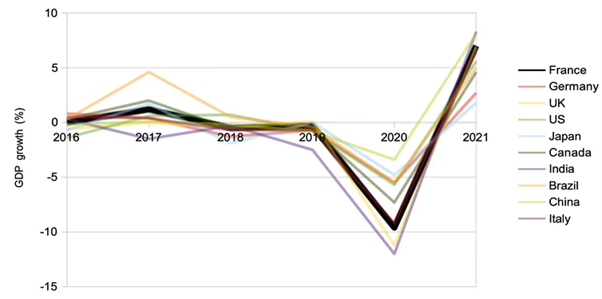

In recent years, France, similar to many western European nations, has experienced poor real GDP growth. France’s real GDP grew just 1.27% a year from 2011 to 2019, just before COVID and the unemployment rate remains high. The French economy performed better than expected after the calamitous effects of the Covid crisis, with 6% growth in 2021 – higher than Germany, Italy and Spain. Unemployment sank to 7.4% in the fourth quarter of 2021, its lowest rate since 2008. But slowing global growth and the war in Ukraine will deliver a much weaker recovery this year.

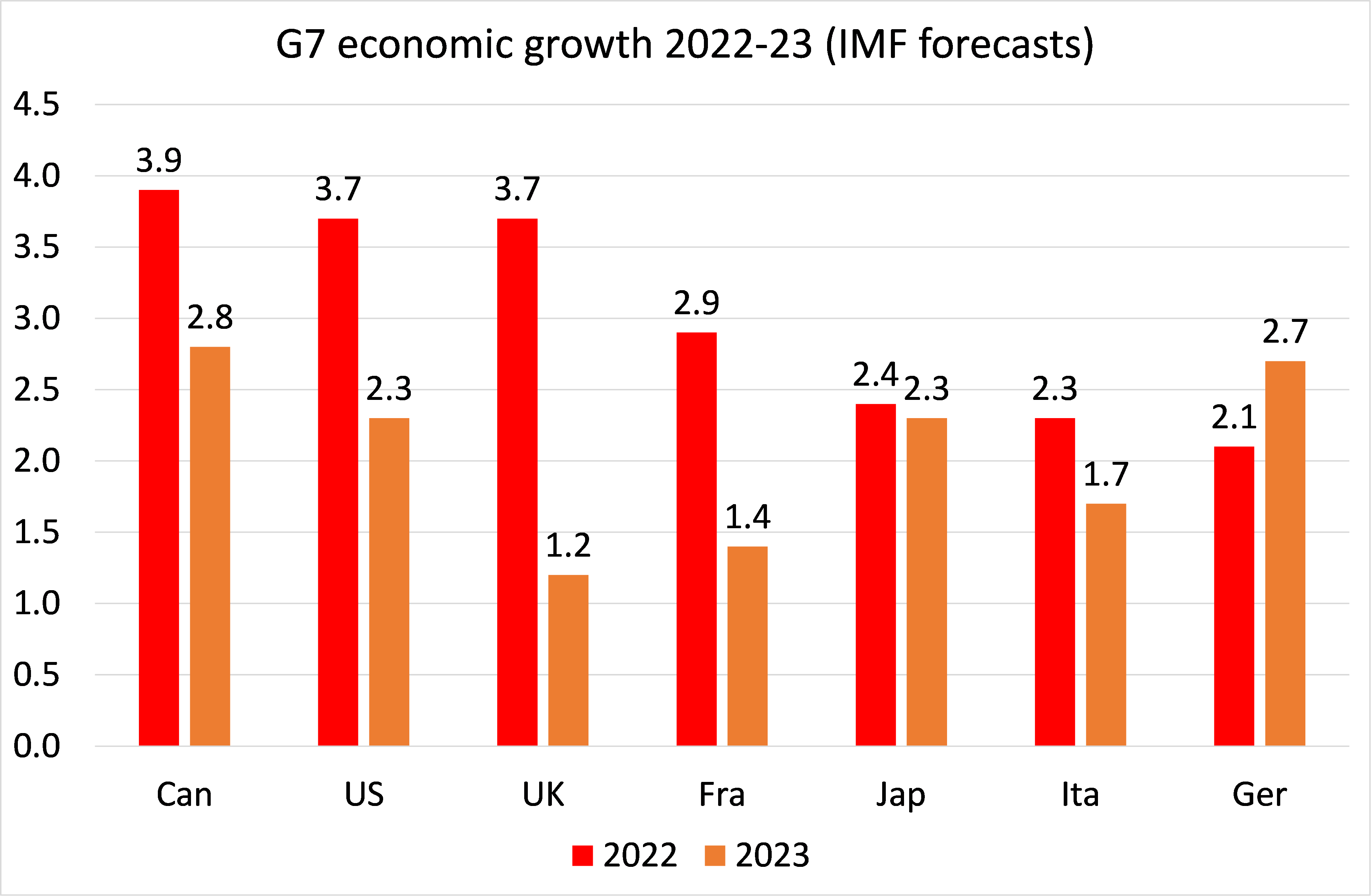

Like other G7 economies, the French economy is suffering from the global supply chain breakdown, rising energy and food prices and the Ukraine war. The IMF forecasts real GDP growth this year of just 2.9% and only 1.4% next year. Over those two years, only Italy is expected to grow more slowly in the G7.

Indeed, the French capitalist economy has followed the same pattern as the other G7 economies in the 21st century: slowing economic growth, then the Great Recession, followed by even weaker growth and investment,…

… and stagnating productivity.

As always, behind this relative stagnation lies the falling profitability of capital. French capital’s profitability peaked at the beginning of the 21st century and has trended down since. There was a sharp fall in the Great Recession and no recovery in the last decade, culminating in another sharp drop in the COVID 2020 slump.

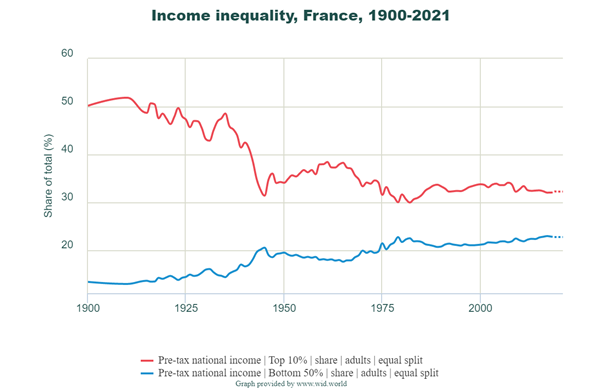

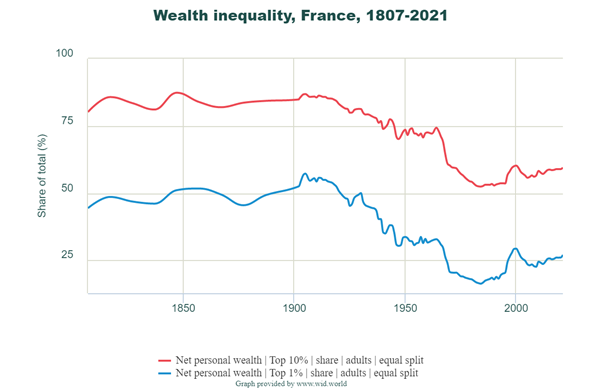

Inequality of incomes and wealth, while lower than in the US or the UK, remain relatively high and unchanged for the last 40 years.

Successive governments, whether of the centre-left or centre-right, have failed to deliver increased prosperity, full employment and a reduction in inequality. As the global capitalist economy deteriorates, with the rising prospect of a new recession, a Macron government will change nothing, except probably for the worse.

Support us and become part of a medium that takes responsibility for society

BRAVE NEW EUROPE is a not-for-profit educational platform for economics, politics, and climate change that brings authors at the cutting edge of progressive thought together with activists and others with articles like this. If you would like to support our work and want to see more writing free of state or corporate media bias and free of charge. To maintain the impetus and impartiality we need fresh funds every month. Three hundred donors, giving £5 or 5 euros a month would bring us close to £1,500 monthly, which is enough to keep us ticking over.

Be the first to comment