The experience of the post-pandemic inflationary ‘shock’ exposed (yet again) the nonsense of monetarism

Michael Roberts is an Economist in the City of London and a prolific blogger

Cross-posted from Michael Roberts’ blog

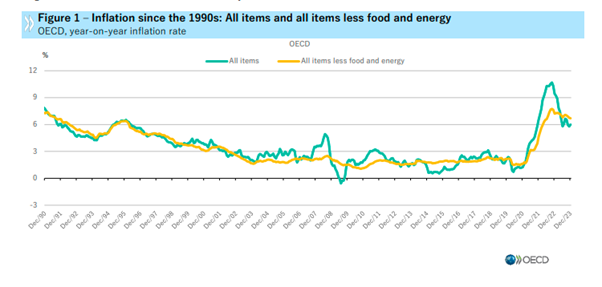

Headline inflation rates in the major economies have nearly halved since they peaked back in 2022. Average consumer price growth across the advanced capitalist economies has dropped from more than 7% in 2022 to 4.6% in 2023, according to the IMF.

The reason for the acceleration of consumer price inflation from 2020-2022 has now been well established. It was caused by a sharp fall in the supply of basic commodities and intermediate products which drove up prices of these suddenly scarce goods. This was compounded by a breakdown in the global supply chain of goods transported and trade internationally.

The inflationary spiral from the end of the pandemic slump in 2020 to the peak in 2022 was not the result of ‘excessive demand’ caused by too much government spending or wage increases driving up costs for companies. Study after study has shown that it was supply issues not wage demands that generated the price rises (an average rise of 20% over two years). Indeed, if anything, it was excessive profit rises that contributed as companies with any ‘market power’ ie a monopolistic position took advantage of rising input costs to raise their ‘mark-ups’. This was particularly the case from the energy and food majors which control the pricing in those markets.

And yet, central bankers continue to insist that inflation rates well above their policy target of 2% a year were caused by ‘too much’ demand or ‘excessive’ wage rises. They have to say this because it is their raison d’etre. Central banks are here to manipulate interest rates and money supply, supposedly in order to ‘control’ inflation and the economy. They rest their policies on the monetarist theory that it is money supply growth and the cost of borrowing (interest rates) that control price inflation. But the experience of the post-pandemic inflationary ‘shock’ exposed (yet again) the nonsense of monetarism.

Do we need to control inflation? For workers, the answer is clearly, yes; because no inflation and even deflation means that their weekly or monthly pay checks are worth the same and any increase would mean better living standards. But that is not the same for companies. They like and want some ‘moderate’ inflation as it allows room to preserve profitability when costs of production rise or wage rises offer more demand. That’s why central banks do not have a target of zero inflation, but instead something like 2% a year.

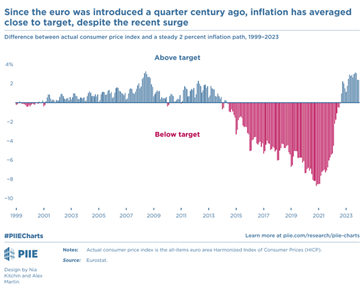

But setting a target of 2% a year is really admitting that central banks cannot control price inflation. Indeed, if we look at the history of monetary policy and its ability to achieve the (arbitrarily fixed) inflation target of 2% a year in the major advanced capitalist economies, it has been a total failure. Take the ECB’s record. In the 25 years of the existence of the euro, the ECB has only got close to achieving the 2% target once, in 2007. In every other year, inflation has been either well above 2% or well below.

Just by chance the 25-year average inflation rate is 2%, but as the chart below shows, there was a multi-year streak of undershooting the 2% from the end of 2013 (with an annual average inflation at just 0.7% to 2020, then the current overshoot (the annual average inflation since end-2020 has been 5.7%). And before 2013, the inflation rate was always well above target, despite hiking interest rates and keeping money supply growth down. In the 2010s, despite quantitative easing (monetary injections) and low and even zero interest rates, inflation did not reach 2% a year. Overall, the inflation rate had a standard deviation from the 2% annual target of 1.8 times.

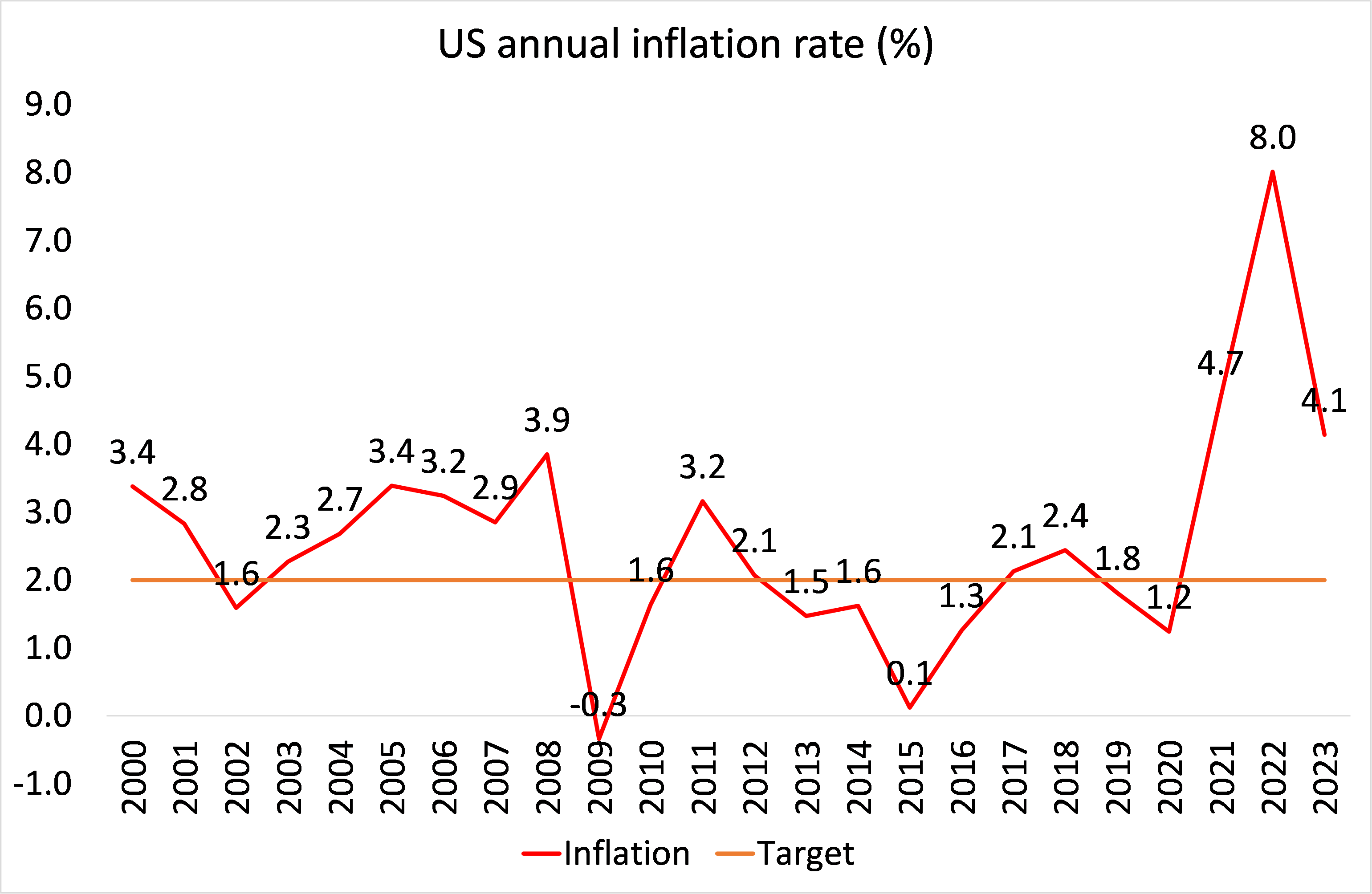

It is the same story with the US Fed. The Fed was close to its target in only two years out of the last 24, and with a standard deviation of 1.2 times. The Fed failed to keep inflation down to 2% in the 2000s and failed to get inflation up to 2% in the 2010s. Neither tight monetary policy worked in the 2000s, nor did ‘loose’ monetary policy work in the 2010s.

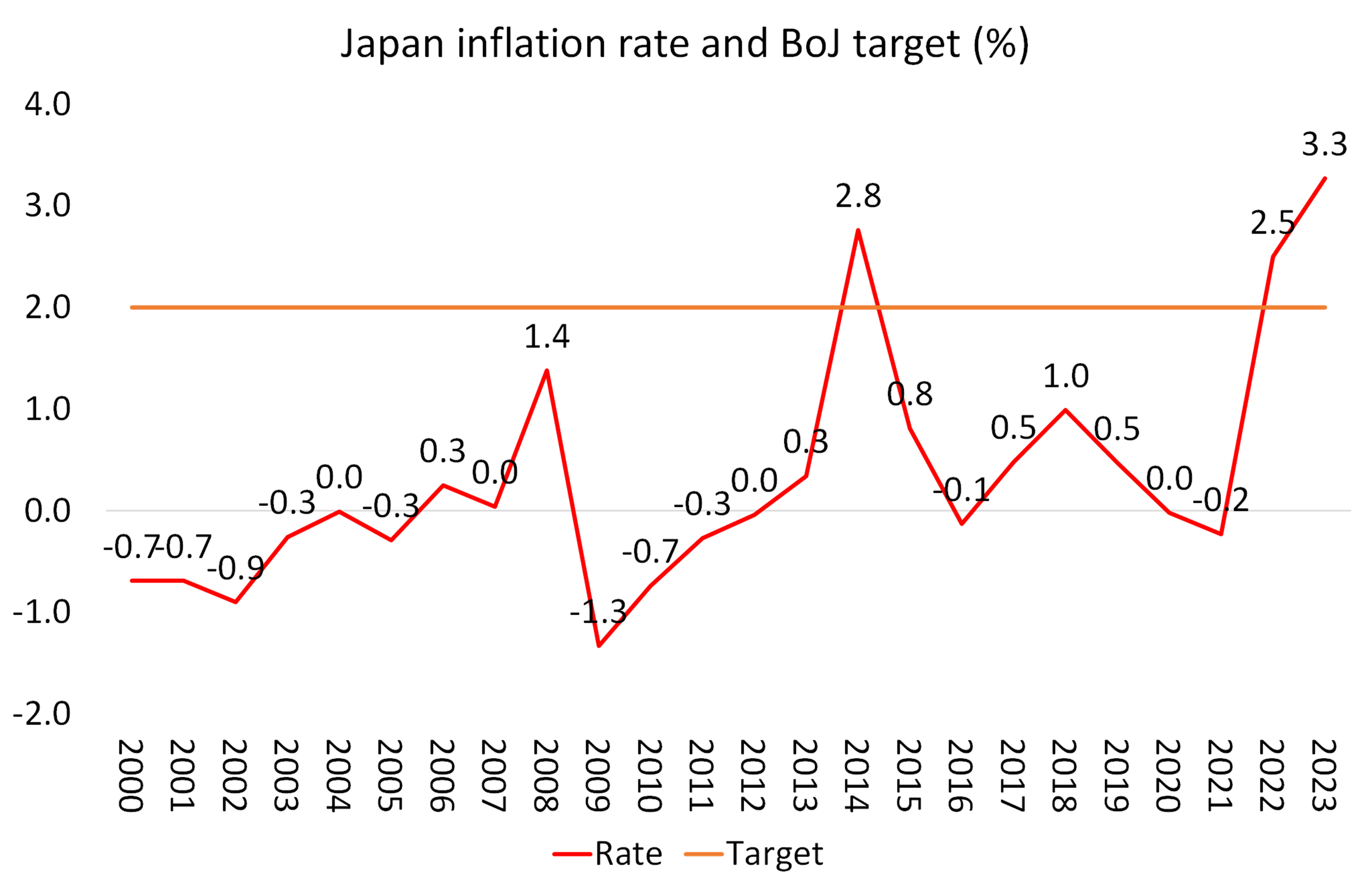

And when it comes to the Bank of Japan, it totally failed to get inflation up to 2% a year until the recent inflationary shock, despite zero interest rates and massive quantitative easing (bond purchases).

What the BoJ record confirms is that it is activity in the ‘real’ economy and the decisions of banks and companies regarding their profits (including whether to ‘hoard’ money) that decides inflation, not central bank monetary policy.

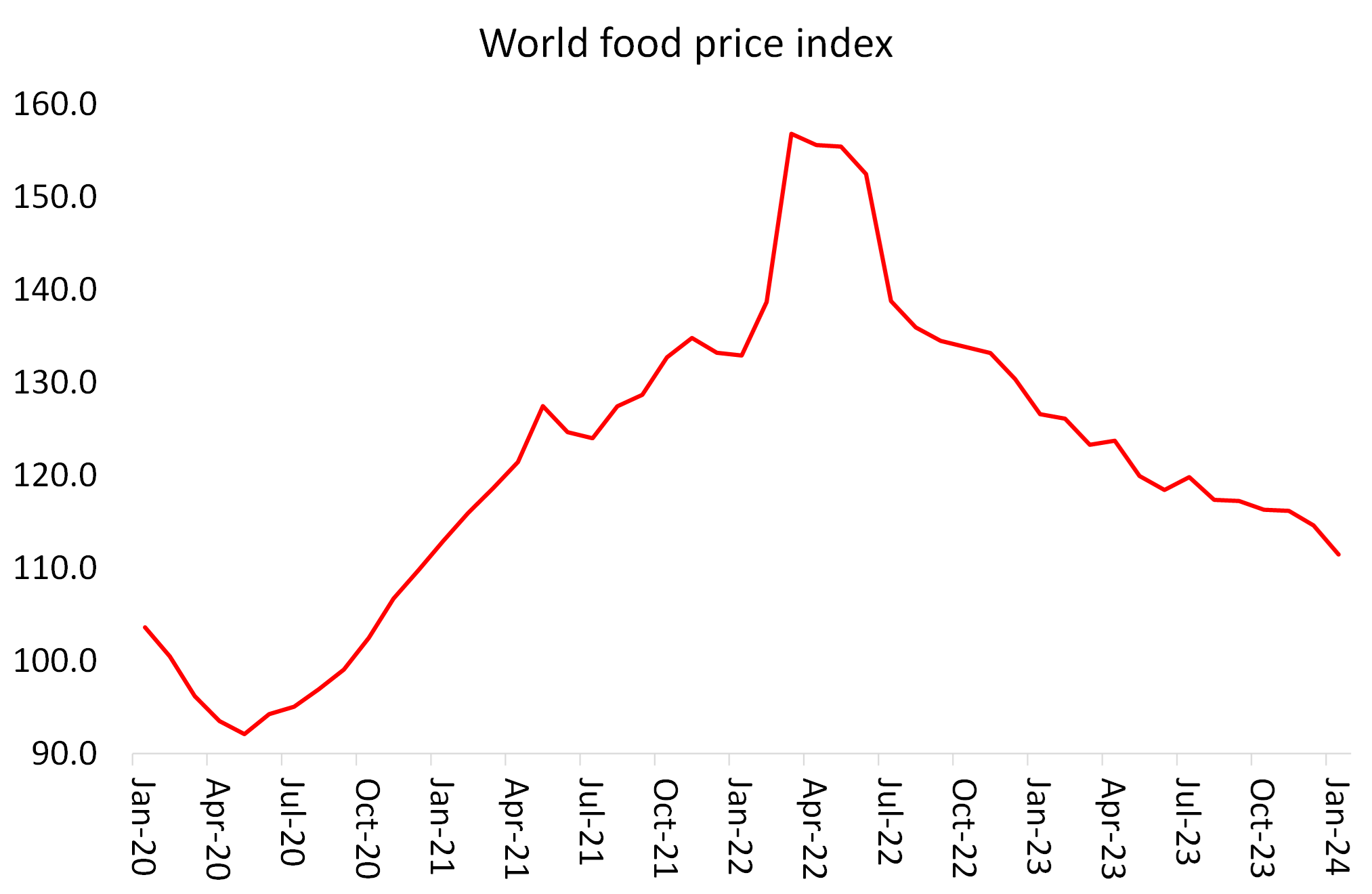

Despite the futility of their policies, central banks have ploughed on with trying to control inflation in the last two years by raising interest rates and tightening money supply. Now they are claiming their policies are why inflation rates have dropped in the last year and are still falling (for now). And yet it is clear that it is the sharp fallback in energy and food prices and prices for various intermediate products that has driven average inflation down.

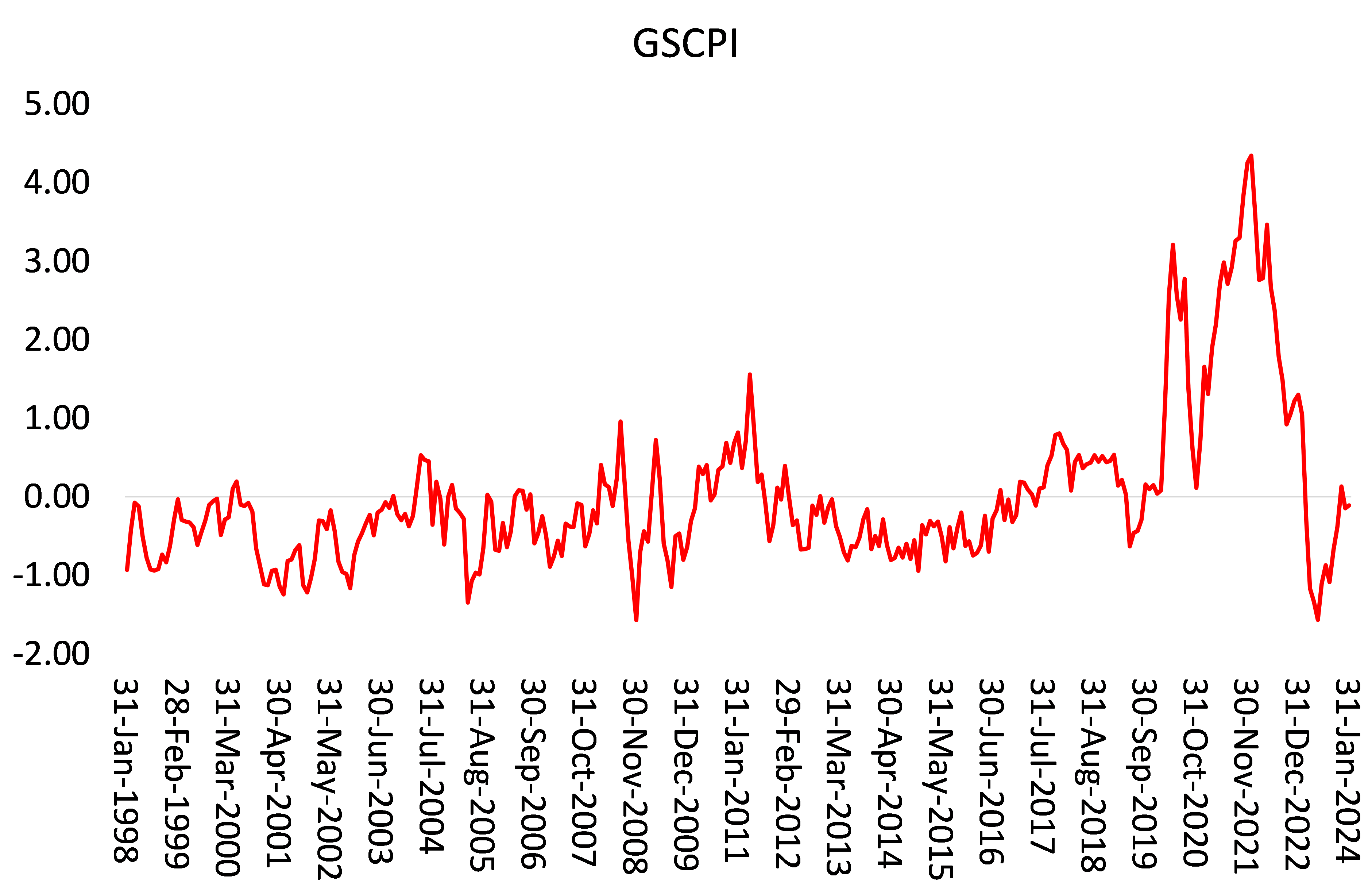

At the same time, global supply chain pressures have been reduced.

New York Fed global supply chain pressure index (GSCPI).

Central bank monetary policy has had little to do with any of this.

Isabel Schnabel is the most hawkish member of the ECB’s six-person executive board. The German economist has become one of the most influential voices on eurozone monetary policy. She continues to argue that monetary policy has been effective in controlling inflation. “Monetary policy was and remains essential to bring inflation down. If you look around, you see signs of monetary policy transmission everywhere. Just look at the tightening of financing conditions and the sharp deceleration of bank lending. Look at the decline of housing investments or at weak construction activity. And importantly, look at the broadly anchored inflation expectations in the wake of the largest inflation shock we have experienced in decades.”

Even Schnabel has to admit that, “It’s true, of course, that part of the decline in inflation reflects the reversal of supply-side shocks.” (only ‘part’?). But she continues, “monetary policy has been instrumental in slowing the pass-through of higher costs to consumer prices and in containing second-round effects.” By ‘second round effects’, she means inflation expectations.

But most of these signs are of tightening monetary policies with no causal connection to inflation. The claim that inflation was curbed by central banks ‘anchoring inflation expectations’ is really a psychological theory of inflation. Inflation expectations by consumers and companies only vary because of what is actually happening to prices. Inflation expectations have fallen because price inflation has slowed.

According to Schnabel, now the war against inflation was “at a critical phase where the calibration and transmission of monetary policy become especially important because it is all about containing the second-round effects.” This was what she has called “the last mile” in the battle to get inflation down to 2% a year.

And what is the difficulty here? Yet again, it is not supply issues or even profit mark-ups, but “the strong growth in nominal wages as employees are trying to catch up on their lost income.”. For Schnabel, it’s wage demands that are stopping inflation from falling further.

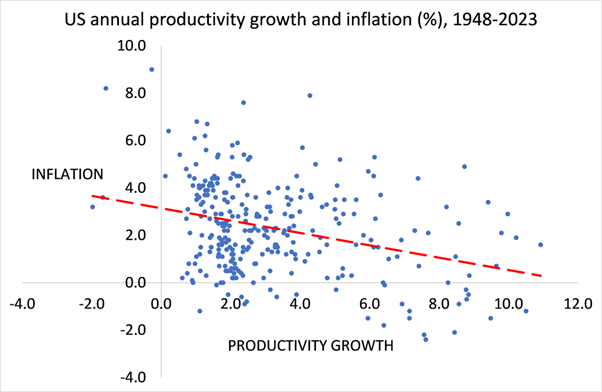

But Schnabel has to admit that if productivity growth (output per worker) were rising too, then wage costs per unit of output would not rise and profits would be secure. Unfortunately, for corporate profits, “we’ve seen a worrying decline in productivity” so “the combination of the strong rise in nominal wages and the drop in productivity has led to a historically high growth in unit labour costs.”

And indeed, there is a strong inverse correlation (0.45) between productivity growth and inflation rates over the last two decades.

Without sufficient productivity growth (more exploitation of labour), this could drive down profitability unless wage demands are curbed. “How are firms going to react? Will they be able to pass through higher unit labour costs to consumer prices?”, worries Schnabel. This is where central bank monetary policy comes in, namely to curb spending and investment by raising the cost of borrowing, she argues.

Schnabel is worried that the inflation beast has not been tamed yet and so high interest rates must be sustained. She refers to an IMF study that claims to show that when interest rates are kept high until the pips of the economic orange squeak, this not only stops inflation coming back, but also eventually gets the economy going quicker afterwards. This is the Volcker policy of the late 1970s in the US. Volcker was the Fed chief then and to ‘cure’ the economy from inflation he maintained high interest rates until the US economy dropped into a slump. Inflation then subsided but along with the economy and jobs. But this ‘cleansed’ the economy supposedly for faster growth later in the 1980s.

But the cleansing solution comes at a price (sic). The IMF report’s key finding is that the successful resolution of inflation shocks was associated with more substantial monetary policy tightening. “But those that resolved inflation with high interest rates experienced a larger decline in GDP growth than those that did not.” (IMF).

The problem with Schnabel’s monetarist theory is that it does not hold with the reality of capitalist production. Within this theory is the neoclassical concept of an ‘equilibrium rate of interest’ called R*, which is the interest rate level that supposedly keeps inflation to the set target, but also avoids unemployment and a slump. Schnabel: “The problem is it cannot be estimated with any confidence, which means that it is extremely hard to operationalize …. What we really care about is the short-run R-star, because it is relevant to determine whether our interest rates are restrictive or accommodative. The problem is we don’t know where it is precisely.” (!)

Indeed, as Minneapolis Fed President Neel Kashkari recently explained, “The concept of a neutral stance of monetary policy is critical to assessing where policy is now and what pressure it is having on the economy. While we cannot directly observe neutral, economists have models to estimate it, which are imperfect even under normal economic circumstances. Our various workhorse models for the economy have struggled to explain and forecast the pandemic and post-pandemic periods given the extraordinary changes and disruptions the economy has experienced. So I also look to measures of economic activity for signals to try to evaluate the stance of policy. In other words, the monetarist theory cannot be applied to reality and the reality is that economic activity drives inflation and money circulation, not vice versa.

Schnabel recognizes the past failure of monetarist policies. “One is the period after the launch of the ECB’s asset purchase programme in 2015. That was a time when a lot of central bank reserves — base money — were created. But we did not succeed in lifting the economy out of the low-inflation environment. Why was that?” The reason was that “the balance sheets of banks, firms, households and governments were relatively weak. You remember, after the global financial crisis and the euro area sovereign debt crisis, there was little willingness to grant loans and to invest. Inflation did not come back as much as the ECB would have hoped.” Exactly.

It was the state of the real economy, in particular profitability of capital and the low demand for credit to invest, not the price of money, not the mythical R*, that drove the economy. The ECB was ‘pushing on a string’, to use Keynes’ phrase, and getting nowhere in reaching its arbitrary 2% inflation target. Schnabel again: “the ECB’s asset purchases before the pandemic were not as successful in bringing inflation back to our target as we would have hoped, because their effectiveness depends on the economic environment.”

Indeed. The truth is that central banks have little or no influence over the investment decision of companies – it’s the profitability of investment that matters, and from that, flows how much inflation emerges in an economy. Given that profitability of capital currently remains low, investment growth is weak and productivity is not recovering much, this suggests that Schnabel’s ‘last mile’ is more like a horizon that she will never reach.

Be the first to comment