A concise world economic outlook to get caught up with global developments.

Michael Roberts is an Economist in the City of London and prolific blogger

Cross-posted from Michael Roberts Blog

At the weekend G20 meeting of finance ministers and central bankers in Japan, the world’s finance leaders tried to put a brave face on the situation. Tension over the intensifying trade war between China and the US was the biggest talking point at the meetings. Officials also wrangled over wording for a final communique on how to describe their concerns for world growth. While they flagged that it appears to be ‘stabilizing’, they also warned that the risks were tilted to the downside. “Most importantly, trade and geopolitical tensions have intensified. We will continue to address these risks, and stand ready to take further action”, the communiqué said.

But where is this action to avoid a new global recession going to come from? The world’s central banks, it seems. “Central banks are heroes,” OECD Secretary General Angel Gurria told Bloomberg Television in an interview during the meetings. “The question is: how much armoury do they still have, how many bullets, particularly silver bullets?”

In other words, what monetary policy weapons do the major central banks have left after ten years of keeping policy interest rates near or even below zero, and after massive injections of money through ‘quantitative easing’, buying up all the debt of governments and corporations from banks in order to encourage them to lend for investment?

Well, we are about to find out in the US. The Federal Reserve led by Jay Powell, having gradually raised its policy rate for the last four years, is now indicating that it will reverse this policy and take its rate down again in order to boost the American and world economy. Powell told markets and the G20 ministers that the Fed stood ready to cut interest rates, saying it would “act as appropriate to sustain the expansion”.

A put is financial jargon for betting on a rise in financial assets in futures markets. In the mid-1990s the then Fed chair Alan Greenspan reduced interest rates to boost the stock and property markets. The Greenspan ‘put’ ‘took the stock market to a new peak in 2000, (but it was followed by the huge ‘dot.com’ bust). We are about to have the Powell put to do the same. Financial markets are now betting that the Fed will cut rates and keep the cost of borrowing really low in order to speculate further in financial markets. Jay Powell is set to be the new hero.

Thus the fantasy world of financial markets may be extended. But will cutting interest rates avoid a recession in the ‘real’ economy? Everywhere the ‘hard data’ are showing a sharp slowdown in economic growth, a collapse of the world car industry, and outright slumps in many large so-called emerging economies. Above all, there is a significant a contraction in world trade as the trade and technology war instigated by the US against China hots up.

US economic growth had accelerated (from 2% to 3% a year) in 2018 after the Trump corporate tax cuts boosted profits – and unemployment dropped to post-war lows. But last Friday’s May employment growth figures were the lowest in years and wage growth that had been accelerating also dropped off. So there are signs that Trumponomics has been exhausted. Now Jay Powell must step up to the proverbial baseball plate (after being ‘encouraged’ by Trump).

Elsewhere in the world, two key G7 economies continue to show a significant slowdown in economic growth. German industrial production plunged 1.9% from a month earlier in April. That was the biggest drop in output since August 2015. Year-on-year, industrial production dropped 1.8% over April 2018, following a 0.9% fall in March. Manufacturing output dropped 3.4% over the year!. Both German exports and imports fell. German growth is now the slowest in five years. As a result, the German Bundesbank central bank cuts its GDP growth forecast for this year to just 0.6%, down from 1.6% at the beginning of 2019.

At the same time,the G20’s host, Japan announced that wages had fallen for the fourth consecutive month and overall household spending slowed sharply. Unemployment, currently at record lows, was now set to rise. And most important, China’s economic growth rate is at its lowest level in over a decade – even if the rate of 6%-plus is around three times the average in the rest of the G20 economies.

In its semi-annual report on Global Economic Prospects, the World Bank cuts it forecast for global economic growth (that’s all countries including China and India) for this year by 0.3% percentage points to 2.6%. “There’s been a tumble in business confidence, a deepening slowdown in global trade and sluggish investment in emerging and developing economies,” said new (Trump-appointed) World Bank President David Malpass, “Momentum remains fragile.”

World trade growth is expected to fall to its lowest level since the global financial crash of 2008. The bank also warned that risks are skewed “firmly” to the downside, citing reignited trade tensions between the U.S. and China, financial turbulence in emerging markets and sharper-than-expected weakness in advanced nations, particularly Europe. Hidden in the back of its report, World Bank economists reckon that “A sharper-than expected deceleration of activity in systemically large economies—such as China, the Euro Area, and the United States—could also have broad ranging repercussions. The probability of growth in 2020 being at least 1 percentage-point below current projections is estimated at close to 20 percent. Such slowdown would be comparable to the 2001 global downturn.”

Another sign that the world capitalist economy is turning sour is what’s happening in the smaller G20 economies. Growth in the Australian economy fell to its weakest rate in almost a decade in the first three months of this year. The economy grew by just 1.8 per cent year on year in the first quarter, and down from 2.3 per cent year on year in the preceding fourth quarter. This is Australia’s worst quarterly growth showing since the end of 2009.

Among the so-called BRICS (Brazil, China, India, Russia and South Africa), it is looking even worse. The South African economy is now suffering its worst slump in a decade. Output in Africa’s most industrialised nation dropped by an annualised 3.2 per cent in the first quarter, its largest quarterly fall since 2009. Power-intensive industries such as manufacturing and mining recorded the biggest drops in activity in the quarter. Mining activity fell by more than 10 per cent while manufacturing dropped 8.8 per cent.

Turkey went into a recession earlier this year under Turkey’s Trump, President Erdogan. Argentina was already in a slump in 2018 under the governance of the right-wing administration of President Macri. The country is now experiencing vicious austerity measures at the behest of the IMF which is bailing out the Macro government with the biggest loans in its history.

But the likely trigger of a new recession is the ongoing and intensifying trade and technology war between the US and China. Neither side appears to be ready to back down and, as a result, world trade growth is diving while there is the prospect of increased tariffs and protectionist measures that will hit world growth. Bloomberg economists reckon that if tariffs expand to cover all US-China trade in the next few months, then global GDP will take a $600bn hit in 2021. With 25% tariffs on all bilateral trade, GDP would be down 0.8% for China: 0.5% for the US and 0.5% for the world economy compared to no trade war. That spells global recession.

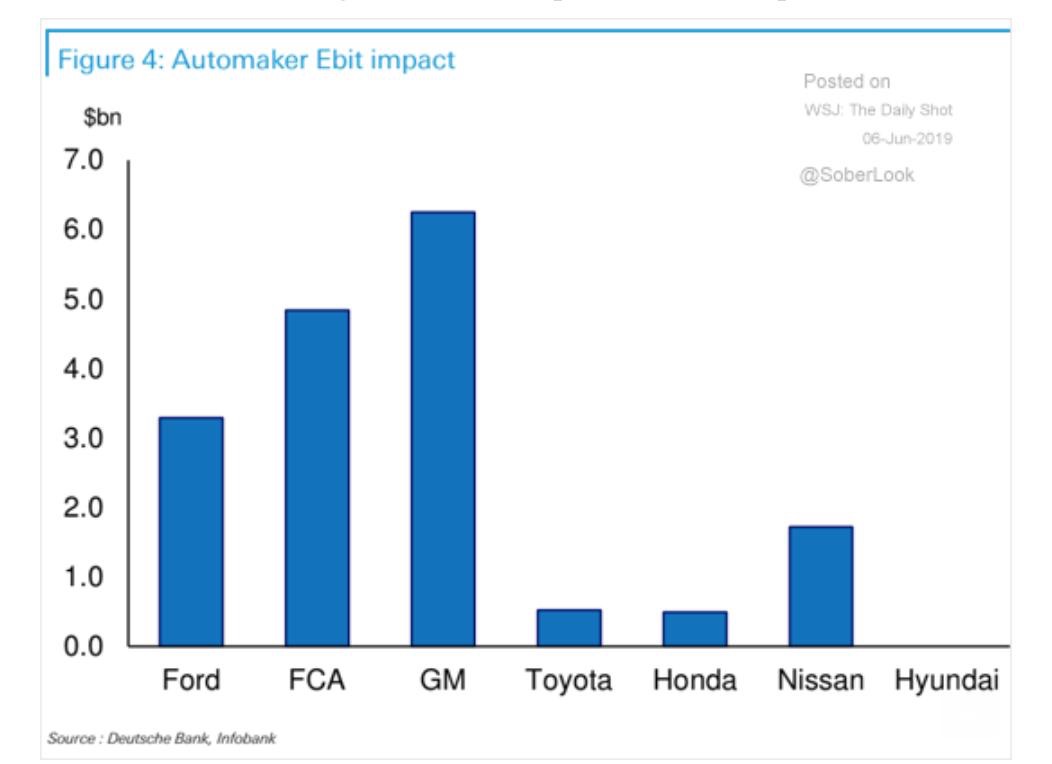

And Trump seems bent on widening the trade war to other economies. He has just temporarily delayed introducing a range of tariffs on Mexican imports, including imports of car and car parts that American companies make inside the Mexican border with the US. The world car industry is already in major crisis driven by the end of diesel and slowing demand in China, Europe and Japan. Now American car companies face new problems with Trump’s plans.

Thus while financial markets may be set to boom with the Powell put, that’s likely to have little effect on the struggling world economy. The recovery since the Great Recession ended in mid-2009 has reached its tenth year, making it the longest from a slump in 75 years. But it is also the weakest recovery since 1945. Trend real GDP growth and business investment remains well down from the rate before 2007.

The trade and technology war is settling in for the long haul. What makes it likely that the trade war will not be resolved amicably to avoid a global recession is that the battle between the US and China is not just over ‘unfair trade’, it is much more an attempt by the US to maintain its global technological superiority in the face of China’s fast rise to compete. The attack on Huawei, globally organised by the US, is just the start.

US investment bank Goldman Sachs has noted that, since 2010, the only place where corporate earnings have expanded is in the US. And this, according to Goldmans, is entirely down to the super-tech companies. Global profits ex technology are only moderately higher than they were prior to the financial crisis, while technology profits have moved sharply upwards (mainly reflecting the impact of large US technology companies). And now it is just this sector that will suffer from the technology war.

The risk of a new recession, as measured by various methods, continues to rise. Here is the New York Fed’s index of the probability of a recession based on analysing financial market and economic data.

Then there is the supposedly reliable indicator of the inverted yield curve in bond markets. Normally, the interest rate of long-term bonds (ie 10 years or more) is much higher than the short-term interest (less than one year). So the ‘curve’ of interest rates from 3m to 10 years is up (or steep). But when the 10-year rate drops below the three-month rate, this has invariably heralded a new recession within a year. Why? Because it implies that investors are so worried about the future that they want to hold ‘safe’ assets like government bonds rather than invest, to the point that long-term interest rate on these bonds falls below even the rate set by the Federal Reserve for short-term loans.

The yield on benchmark U.S. government bonds hit new 2019 lows near 2% before the G20 meeting. Yields on 10-year bonds in both Germany and Japan were below zero! About $11 trillion of bonds around the world, concentrated in Europe and Japan, carry negative yields, now account for about 20% of all debt world-wide.

And US yield curve has now inverted. The inversion has only just happened and it needs to continue for a few months to justify its reliability as a recession indicator. So watch this space. Maybe the central bank heroes can save the day.

Be the first to comment