After Covid19, huge numbers of households and companies are expected to have loan payment difficulties, aggravating the socially disastrous effects of the crisis and putting a serious strain on the recovery. The EU’s plans to tackle this problem are flawed and misled by the neoliberal belief that markets and financial engineering can fix this deep socio-economic problem.

Cross-posted from Positive Money Europe

Photo credit: Caroline Metz

A good part of banks’ daily business is to provide loans to people and companies. But what happens when someone cannot reimburse the money owed to their bank?

In financial jargon, when a person or a company has been unable to pay back a loan for more than 90 days, the loan is said to become ‘non-performing’. Non-performing loans (NPLs) mean trouble for both the debtors (consumers or companies) and creditors (banks). The debtor may face penalties for delayed payments, and in most difficult cases, a non-performing loan incurs losses for the bank.

In normal times, NPLs are not a big problem. In any given bank, there are always some loans that turn out not to be repaid in full, but banks make up for this by making profits on the millions of other clients in their loan books, and via financial market trading.

However, NPLs become a much bigger problem if they become a widespread phenomenon – as it usually happens in the aftermath of big economic crises.

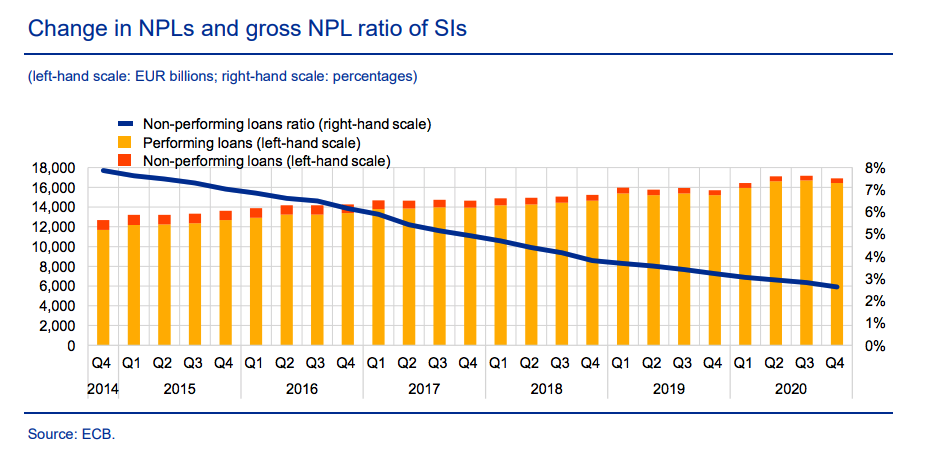

After the great financial crisis of 2008-2009, European NPLs reached a peak volume of €1 trillion, causing massive problems for banks in Italy, Spain, Greece and Ireland. Since then, the ratio of NPLs kept decreasing, and reached an average of 2.6% at the onset of the Covid19 crisis in mid-2020.[1]

Historically, European institutions have mainly addressed the issue of NPLs as a narrow banking regulation issue. However, NPLs are a much more systemic and even societal issue. A high rate of NPLs is not only a warning indicator of the (poor) state of our economic system, but their long-lasting impact should also worry us. Bad loans mean that swathes of people and companies have fallen into debt problems. Without sustainable incomes or revenues to pay their debts, how can we expect these companies and individuals to spend, invest, hire? At the macroeconomic level, rampant over-indebtedness acts as a drag on the economic recovery.

The social consequences of over-indebtedness can also be tragic. Families might be forced to decide between eating a hot meal or paying their monthly mortgage installments, all while facing soaring fees and fearing threats from creditors. Viable businesses are also left falling into debt spirals and avoidable bankruptcies, leaving more workers unemployed than it should.

The calm before the storm

How big the NPL problem will be after the Covid19 pandemic is still an open question. Last November, the ECB estimated that “under a severe but plausible scenario” NPLs could amount to €1.4 trillion by the end of 2022.

Paradoxically, non-performing loan ratios have gone down in 2020, in spite of the general rise in private debt due to Covid19. However this isn’t necessarily a good sign. Rather, it might mean that the problem has “yet to emerge” or that the bank’s own estimates of the number of upcoming NPLs are not reliable.

Hoping to prevent the Covid19 crisis from turning into a banking crisis, the ECB granted banks some flexibility around the identification and treatment of non-performing loans (for example, banks were given more time to set aside capital provisions needed to absorb future NPL-related losses). However, this regulatory backsliding also deprived regulators of key metrics of the health of banks. As of May 2021, only half of the assessed banks were meeting supervisory expectations when it comes to dealing with NPLs, notably because banks tend to rely on overly optimistic assumptions, relaxed risk models and backward looking indicators of risk.

Given the lack of reliable data, there is a huge risk that the problem will resurface abruptly at the very moment when the economy is supposed to recover at full speed. Until now, far-ranging public support such as job retention schemes, loan moratoria and guarantees have been keeping afloat millions of companies and households that would otherwise be in serious credit trouble. As governments start withdrawing their emergency support measures, it is expected that corporate insolvencies will increase. There is a serious risk that such a wave of business shut-downs will trigger a negative spiral. Business closures would further depress households’ incomes and employment prospects, heightening once again the risk of consumer over-indebtedness … itself conducive to more debt defaults.

Thus, while the range of public support by the ECB and governments has been vital, it makes it difficult to foresee the scale of the upcoming NPL problem. As ECB Supervision’s Elizabeth McCaul warned, the tardy reckoning of distressed assets is likely to backfire. This could result in a surge in unexpected losses at a later stage.

The neoliberal thinking behind the EU’s action plan

Despite the uncertainty on whether such a doomed scenario will materialise, the EU must be prepared for any eventuality. To this effect the European Commission announced last December a renewed action plan to tackle NPLs in the aftermath of the Covid19 crisis. The ECB Supervision board also made NPLs its top priority for 2021, as recently reiterated in a memo to the Eurogroup.

The Commission’s action plan, regrettably, is a mere recycling of the EU’s old ideas – and those that have been long pushed for by financial industry lobbyists. The Commission, first of all, continues to promote “the development of secondary markets for distressed assets”.

On 4th June 2021, the Council and European Parliament came to a provisional agreement in order to execute the Commission’s plan for developing secondary markets for non-performing loans. In other words, the EU wants to make it easier for commercial banks to sell their non-performing assets to other financial investors. But who would want to invest in bad loans, one may ask?

Well, believe it or not, there are investors out there whose business is precisely to turn bad loans into juicy profits. Among those are debt collection companies, but also global investors such as large banking groups, asset managers, pension funds, and private equity firms – known as ‘vulture funds’ due to their predatory methods – looking for ‘alternative’ asset classes to invest in.

A second proposal in the Commission’s action plan involves the “establishment and cooperation of national asset management companies (AMCs) at EU level”, in cases where banks exhibit critically high levels of NPLs. Also known as ‘bad banks’, AMCs are dedicated financial entities created by governments in order to enable banks to get rid of their distressed assets. In practice, banks sell their NPLs to the ‘bad bank’ that holds and manages them temporarily, often with the aim of selling the NPLs back to private investors. Increasingly, those financial transactions involve the securitisation of NPLs, a complex financial engineering technique that was one of the causes of the great financial crisis of 2008.

Rather than encouraging banks to restructure troubled loans, the market-based proposals put forward by the Commission favour the transfer of huge portfolios of loans out of banks’ balance sheets and onto global financial markets. The logic justifying the sale of NPLs from banks to third parties is that it helps to clean up banks’ balance sheets while outsourcing debt enforcement to firms specialised in debt collection.

Importantly, banks still make a loss when selling NPLs, because they sell the NPLs loans at a market-price that is significantly lower than the nominal values of the loans (which amount to the total reimbursements if debtors were solvent). However, rather than letting troubled loans linger on the balance sheets of banks, banks and their regulators might prefer to see losses realised immediately, allowing banks to start afresh with ‘cleaned up’ balance sheets and better stability and profitability prospects.

All in all, the Commission’s approach is based on the belief that markets can fix the NPL problem. But markets-based mechanisms do not improve the situation of distressed debtors, on the contrary they often aggravate the fate of indebted businesses and families, which raises serious political and social concerns. Here is why.

NPL marketisation exposes consumers to harassment

NPL sales can also be detrimental to debtors. Academic literature demonstrates that the marketisation of NPLs enhances the power imbalance between creditors and distressed debtors. The investment funds and other financial entities buying up assets at highly discounted rates pursue high returns over the short term. Their aggressive ‘asset management strategies’ in practice mean squeezing debtors hard, with evident risks and costs for borrowers.

As French consumer association UFC Que Choisir recently exposed, this logic often pushes debt collection firms to employ aggressive practices, sometimes akin to harassment. Such ‘malpractices’ are unfortunately widespread across Europe and consumers, who are often already suffering from stress and anxiety due to their financial situation, might now receive threatening letters and doorstep visits from unknown debt collectors.

Although new safeguards for consumers (whose loans are being sold off) were recently obtained by the European Parliament, however they remain very vague for now. In particular, we have little details on how these will be implemented across member states, and whether governments will have the capacity and resources to actually control and regulate the activities of debt purchasers and collectors.

The new creditors are less likely to cooperate with borrowers. Research in the US shows that private equity firms are more likely than banks to foreclose on mortgage holders in arrears. Distressed companies, for their part, sometimes receive equity injections, but this often comes with business restructures. Should they end up renegotiating their loans with their new creditors, they are likely to face tougher loan terms (e.g. higher interest rates, shorter maturities and higher collateral requirements) than if they had negotiated with their usual bank loan officer.

Who benefits from NPLs?

As NPLs are displaced, so are profit opportunities. Private equity funds, which have been among the biggest buyers of European NPLs in 2014-2019, post record profits each year, while debt collection firms see business opportunities soar as debt troubles spread. This raises very serious moral concerns, in a context where popular outrage grows in the face of neoliberal attempts to marketise and “capitalise on almost everything” and as civil society organisations must time and time again stress that “social infrastructure and services are not meant to be run for profit”. We too dispute the idea that distressed debts – and the distressed people behind them – should be treated like any other commodity or “like inanimate goods”, making for juicy profit opportunities for super-wealthy investors and booming debt recovery firms.

As highlighted by EU consumer protection organisation BEUC, NPL markets force us to confront political questions over who benefits and who loses out: should we promote market mechanisms that allow private market actors to “maximise their profits on the back of vulnerable consumers and businesses”, or should we find alternative solutions?

Neoliberal plans to build a global market where distressed assets can be ‘disposed of’ are conducive to an ever complexifying and interconnected financial sector, and overlook the risks that NPL constitute, regardless of who holds them. Indeed, the market-based ‘solutions’ put forward by European institutions do not tackle the roots of the issue: corporations and households whose loans are sold away remain indebted and distressed, only now their debts are owned by new and often far-away creditors, and managed by subcontracted debt collectors.

Even a European bad bank or network of bad banks “will not make losses disappear”, notes former Single Resolution Board Member Antonio Carrascosa, and we couldn’t agree more that focusing “on the cure rather than prevention” is dangerously short-sighted. What preventive actions could the EU and national governments take, then?

A more equitable approach to unsustainable indebtedness is needed, based on targeted debt relief, additional stimulus programmes and a wider rethinking of the EU’s fiscal and monetary rules. We will explore this alternative agenda in an upcoming article.

Be the first to comment