This week there was an article in the website “Tribune” (read here) by a supporter and earlier financial adviser of the Labour Party attacking Modern Monetary Theory (the more popular MMT becomes, the more such articles are written). Richard Murphy, a proponent of MMT, especially in conjunction with a New Green Deal, replies. Thomas Fazi and Bill Mitchell, one of the founders of MMT do the same here. This is a topic, which have you not caught onto it yet, could well play a major role in our future financial and economic policy in Europe, so it si time to get up to speed.

Richard Murphy is Professor of Practice in International Political Economy, City University of London. He campaigns on issues of tax avoidance and tax evasion, as well as blogging at Tax Research UK

Cross-posted from Tax Research UK

Modern monetary theory (MMT) is certainly getting it in the neck right now. Two articles I noticed this week were direct attacks in it. And bizarrely, they come from the left and right.

That said, they have things in common. First, they agree that MMT is right: neither can deny that what MMT says is an accurate description of how the economy works. Second, they do not like the implications of that truth. Third, to achieve their goal they do, of course, misrepresent what MMT is about.

The first of the articles is by Ian Stewart, Deloitte’s Chief Economist in the UK. It is described as a personal view. The second is by James Meadway who was, for a while, economics adviser to John McDonnell but who has now left that job to write a book in Corbynomics.

Stewart provides a summary of his view of MMT in his piece and concludes:

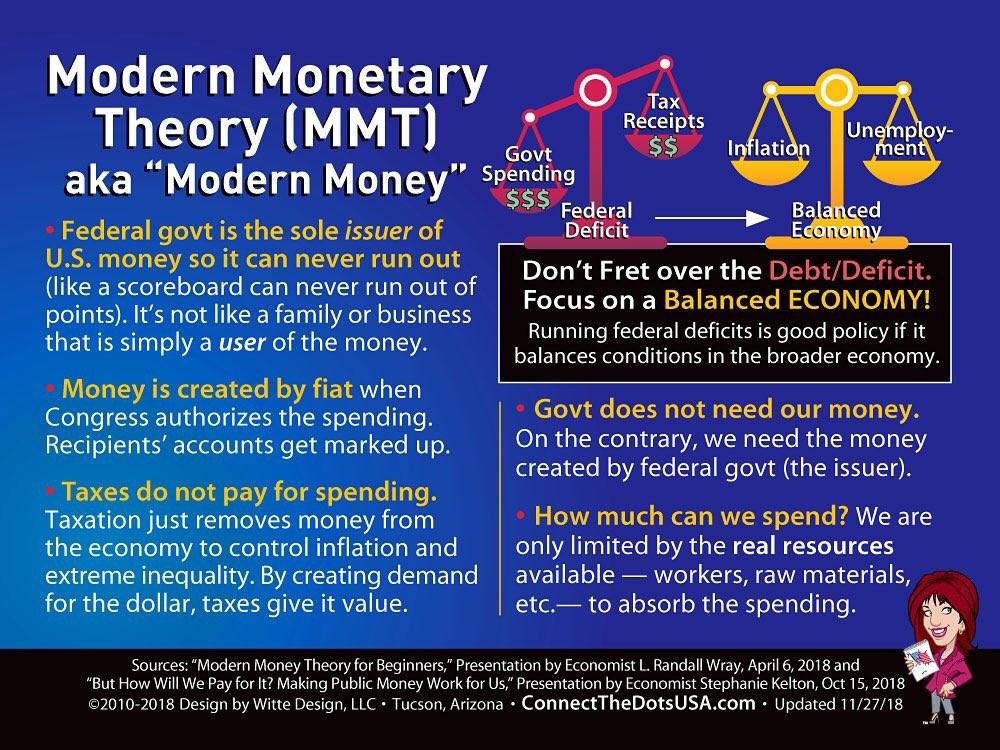

[It’s] worth noting that both MMT and QE involve the government creating money electronically – or, more graphically though incorrectly, printing it. But with QE a central bank creates money to buy assets, such as government bonds. This injection of new money into the system drives down interest rates and bolsters asset prices. Under MMT, by contrast, the government spends the money directly on public services.

In that one paragraph he does two things. He agrees QE works. Money can be created by governments at will. That means a government issuing debt in its own currency cannot go bankrupt. And since government debt is simply a by-product of government spending not funded by taxation, government created money can fund public services. Everything he seeks to portray as fantastic (in the sense of ridiculous) about MMT is then, in his own analysis, true.

James Meadway, writing for Tribune under the title ‘Against MMT’ agrees with Stewart, albeit unwittingly. He says:

There is a sliver of truth here [i.e. in MMT]. As a technical detail, modern governments do not have to collect taxes before they can spend: they can also borrow the money, or create and spend that money directly. On a day-to-day basis, these three things can (and often do) all happen at once.

So, rather as Martin Wolf did about a week ago, here we have opponents of MMT agreeing it is a fully functioning description of how the world really works. For that, I offer them my thanks. But, like Wolf, they then suggest they do not like MMT because of what they claim it means for political policy, and not because it is not true. This moves the whole debate into political arenas.

For Stewart the objections are twofold. The first is that:

[There’s] one crucial difference [between quantitative easing and MMT][, and from it a second follows. With QE, as practised in the US and Europe, central banks have promised to reverse money creation. They can do so because, unlike under MMT, the money that has been created has been swapped for assets which can be sold. The idea is that central banks will, in time, sell these assets, withdrawing money from the system and dampening asset prices and activity. This has so far convinced investors that the new money created will eventually be absorbed back into the system. The message from central banks is that QE does not represent a permanent expansion in the supply of dollars, euros and pounds. By contrast, the money created under MMT will be spent on public services and not in purchasing assets. And, since there are no assets to sell in future, the money creation is permanent.

It’s as if Stewart is saying QE works because we still believe in fairies, but MMT does not work because we don’t. Because let’s be clear that around the world more than $6 trillion has now been injected into economies by QE, and in the UK it’s £435 billion, and to pretend for a moment that most, or even very much at all, of this is going to be reversed is to live in fantasy land. It’s true, a little has been in the US. But that was only possible to reverse the dire impact of Trump’s tax cut that would otherwise have flooded money into markets, which has been mopped up by reselling back into the markets bonds previously owned by the QE programme. And that process is likely to be coming to an end. In the rest of the world nothing like that has happened, and nor is it going to do so. QE is not being reversed, and never will be so Stewart’s claim is literally fantastical and has to be dismissed as such.

But he has another:

A related concern is that government, with its infinite spending power, could hoover up people and resources and crowd out the private sector. This would reduce the tax take and could tempt the government to print more money to fill the gap.

More fundamentally, the state could end up with a far greater role in allocating capital in the economy. The market has flaws and limitations. But it tends to be better at allocating capital and raising efficiency than the government. A worry, therefore, is that MMT could enfeeble the private sector.

I think this is what he really thinks: this is where the objection lies. And it is just wrong. First, we live in a world where most larger businesses have what is in effect a zero cost of capital right now: they can borrow for near enough nothing. If, given that, they do not drive the economy to full employment at a living wage by forcing up the price of labour – and they have spectacularly failed to do so – then there is no risk whatsoever that they will be crowded out of the economy by the state. The fact is that the state has to pick up the slack they have created. And as MMT makes clear, what a government must do must be chosen to make sure that activities by the state can be ‘turned off’ if full employment is reached – which is also the moment when the private sector may be crowded out. In other words, not only has MMT got no plans to sweep the private sector aside, it has a plan in place to make sure it does not.

But in the meantime it will, indeed, allocate capital. Because the evidence is – read The Entrepreneurial State by Mariana Mazzucato – that it is really good at doing so. And at last as good as the banks who crashed the economy in 2008. The state will not enfeeble the private sector. That’s already feeble. What it will do is provide it with the contracts and work it needs to survive because it can’t think of what to do for itself. Stewart does complain too much, and with deeply feeble arguments, including this classic:

For centuries governments have taxed, borrowed or created money to pay for public spending. All carry risks. Heavy taxes dampen growth and upset voters. Excessive public borrowing triggers financial crises. Printing money to pay for public spending can look tempting. But, as rulers from Henry VIII to Venezuela’s Nicolás Maduro have discovered, creating money out of thin air and spending it tends to destroy confidence and send inflation rocketing.

There’s just one problem: Henry VIII was not using a fiat currency and Venezuela was running a currency perpetually undermined by the dollar: it was nowhere near the scenario where MMT might work in that case. But telling tall stories is where the opponents of MMT now are.

Which brings me to James Meadway. James’s argument is more considered, but is again about the politics he considers associated with MMT rather than MMT itself. If I might let me select just some of the arguments he uses and address them. The first is his argument with chartalism which is implicit in MMT. He says:

Chartalism holds that money receives its value fundamentally as a result of its use to pay taxes — that, in the words of leading chartalist Georg Knapp, ‘money is a creature of law’. This is dubious as a historical claim, since money has existed in many different forms throughout history, and only some of those forms have arrived with the stamp of the state — and dubious as a description of reality today, since most money is created by private banks when people take out loans, whose relationship to the state is (at most) indirect.

This, I am afraid is just wrong. Let’s ignore history: the money to which James refers was not fiat currency, and that is what we have now. The comparison then is, to be candid, bogus. But James is also wrong about most money now being made by banks: this is the Positive Money argument that just 3% of money is government made – and is notes and coin – and the rest is bank made. This, again, is superficial at best. Firstly this assumes anyone can create a bank, and they cannot: all banking is under government licence. And second this assumes that central banks have no influence over what banks might do, which they have, albeit they exercised it very poorly for the first decade or so of central bank independence. The reality is that private banks create money – that is government backed money given its value by the promise that the government gives to accept it in payment of taxes – but do so solely because they are given a government licence to undertake this activity and take credit risk when doing so. In principle the Bank of England could take on that role, although I would not want it to do so. But to claim that the central bank has no role in money creation when it is very obvious that it does – as QE evidences – is just wrong.

I then move to James’ claim that:

[I]t is worth keeping in mind … MMT’s greatest theoretical failing — to provide any account of power and the state, or even (like neoclassical economics) to provide a reason why it doesn’t need one.

This is interesting at a number of levels. Firstly, because neoliberalism quite clearly does not say we do not need a state: it is core to that idea that government has the essential task of preserving property rights. Second, you can argue what Keynesianism in its various guises has to say on this issue. I suspect there are about as many answers as there are Keynesians. And third, I think the claim is wrong. What MMT is effectively saying, as Weber might, is that the values projected onto the state (as Keynesians would do) are in effect what the state is: it is the tool for realising values and has value so long as it continues to secure support from the population at large for the values it believes appropriate to adopt based upon its understanding of the population it serves. The power of the state is, then, reflected in its ability to read the collective will and to seek participation in it, indicated by the willingness of the population to accept the obligation to pay tax. And since tax is at the core of MMT, despite all claims to the contrary, I believe James’ claim is wrong, again.

So let’s deal with another objection. It is this:

Unfortunately, what holds as a technical description of how governments pay for their daily operations does not apply over the longer term. The grave danger from issuing money, in particular, is that it will lead to a general rise in prices, known as inflation, something readily acknowledged by academic MMT supporters. They often argue that governments should use taxes to deal with this problem: taxes take money out of wider circulation, and by reducing the amount of money chasing goods and services, you reduce the pressure on prices.

In this scenario, far from the transformative claims made by its online fans, we have ended up in a place remarkably similar to the hated mainstream of economics. Mainstream economics also acknowledges that inflation is an issue, but instead of saying taxes should be used to control it, its adherents, known as neoclassical economists, propose interest rates as a remedy. When these go up, it becomes more expensive to borrow, people borrow less, and this in turn reduces the amount of money in circulation — so the theory goes. But as two left-wing economists sympathetic to MMT, Arjun Jayadev, and J. W. Mason, have recently argued, this means that the only meaningful difference in policy terms between MMT and the mainstream on the central issue of managing inflation is whether the government should use taxes or interest rates.

Except that is absurd. That assumes that the main object of all economics is to control inflation to maintain the value of money so that the value of the claims of the world’s assets owners, to whom debt is owed, are upheld consistently. I sincerely hope left-wing economists do not think that. I hope James does not. But that is what he implies.

Let’s be clear what the difference really is. Neoclassical economics does think that controlling inflation is what economics is about. This is why it promotes independent central banks. This is why it tolerates growing wealth inequality. This is why it has no employment target. And stagnant real wage growth is fine as far as it is concerned.

But to pretend that MMT shares these views is just wrong. I’d hope I could say that for all on the left, who I rather hope should think inflation is acceptable, to some degree, not least to erode the claims of the owners of debt precisely so that inequality is reduced, but also because the issue is secondary to the creation of long term, meaningful, productive well-paid employment which is the goal of MMT, hence the job guarantee. And it should (subject to other resource constraints which redefine these relationships but do not remove them) also be the goal of MMT when mixed with the Green New Deal. That does not mean MMT is indifferent to inflation. And rather usefully – when monetary policy is dead in the water because of zero-bound interest rates that are likely to last for the foreseeable future, where that is a very long time – it has an inflation control policy that can work when nothing else can or will. But let’s not say that makes it the same as neoclassical economics. It is not. James is wrong to suggest that it is.

And it’s absurd to suggest that MMT cannot work in an economy because governments wanting re-election cannot increase tax rates, as James also claims. If that’s a measure of the left’s commitment to a) democracy and b) honesty with the electorate and c) conviction based economic management, heaven help us, most especially when we have the bigger issue of climate change to also deal with, which is much harder to address.

And as for the claim that MMT only works for the US and the dollar, again, that’s just James and the left saying that the bond vigilantes really do rule our economy and we’ll never break them. What faith James has in the power of markets to break democracy! But he’s wrong: that power exists for a few days at a time, but not beyond. That’s largely because MMT removes bond vigilantes’ power by simply saying that if they try to disrupt markets the central bank will buy all the bonds they wish to sell using QE funds created for the purpose – which on this occasion may be quite quickly reversed, I admit. That neuters the threat from the bond vigilantes then. And then that means that real exchange rates will only move on the basis of external shocks (like Brexit, or oil price variation, and MMT cannot control them come what may) or on the basis of real variations in productivity – which MMT seeks to address like no other theory does. Again, James is wrong.

So what is James Meadway really objecting to? What is all this really about? I’d suggest it’s this:

Labour has adopted a strict set of rules for how a future government will manage its finances. The ‘Fiscal Credibility Rule’ says, first, that Labour will commit to removing the deficit on day-to-day government spending at the end of a five-year period.

I hate to say it, but the objection is that Labour thinks it needs balanced budgets. It does not. We know the result is austerity. But Labour can’t countenance anything else. As James says:

Leading MMT advocates like Richard Murphy ask why bother with a rule at all? There are three main reasons. First, a commitment to the Fiscal Credibility Rule allows Labour to put together a coalition of support for its programme from across the economics profession. The party can’t expect every economist to agree with every dot and comma, but the impact of having well-respected experts onside for at least some of that programme is significant. If we want to not only form a government, but make a difference in government, these alliances are essential.

In other words, having neoliberals onside is important. And is achieved by being neoliberal.

The second argument is no better:

The second reason is that clarity and planning help cut through some of the more obvious challenges to Labour’s programme — from journalists demanding to know Labour’s plans for the debt and the deficit, and then, later on, as a guide for civil servants expected to implement its policies.

In other words, Labour cannot be bothered to do the hard work of re-education to deliver what the country needs. Which is deeply depressing. But not as desperate as this, from his conclusion:

The problem with MMT for a genuinely transformational government is not that it is too radical. Quite the opposite: it is nowhere near radical enough. It substitutes a belief in the unlimited capacity of a sovereign government to spend money for the hard reality of the political fight needed to rebuild and transform our society. It is the expression of a deeply conservative faith in the benign nature of our economic institutions. In an increasingly class-divided society, with institutions from the Treasury to the Bank of England to the City that have failed systematically to deal with crisis after crisis, we cannot simply flush away our social problems on a tide of government-printed money.

I am really struggling here. What MMT says is that there need not be a fight for the resources to deliver transformation: they exist. The need is not to have the struggle, but to deliver the outcome. That’s what MMT permits. The demand then is not to campaign, but to do. But apparently that’s too easy for James, for whom the struggle is everything.

And yes, I do have a belief in the benign nature of government. Shouldn’t the left do so? I accept it can be corrupted but to think the government can be a force for good seems to me to be a left-wing basic. James denies it. And so I am lost as to what he is all about. And most certainly as to what his unspecified theory of government might be.

The simple fact is MMT delivers a government the chance to be free of the bogus constraints neoclassical thinking places on it. James would rather continue the ‘struggle’ to be free within the neoclassical model he believes in rather than deliver the reform we need. He makes the wrong choice whenever he’s given the chance to do so. And I confess, why he wants to do so baffles me.

We need people who can think for a new paradigm. Ian Stewart and James Meadway are not it.

Be the first to comment