Once again we can see how MMT is being defamed with no comprehension of what it is about.

Richard Murphy is an economic justice campaigner. Professor of Accounting, Sheffield University Management School. Chartered accountant. Co-founder of the Green New Deal as well as blogging at Tax Research UK

Cross-posted from Tax Research UK

I was sent a link to an article by Michael U. Krause, Thomas A. Lubik and Karl Rhodes for the US Richmond Federal Reserve Bank which is one of the twelve regional federal reserve banks that make up the US Federal Reserve. In it the authors said:

Promoters of modern monetary theory (MMT) — including a growing number of pundits and policymakers — are toying with the idea that “deficits don’t matter.” They are tempted to believe that a government can merge fiscal and monetary policy and simply print currency to pay for its expenditures indefinitely without economic costs or constraints. This core tenet of MMT, which has permeated the public debate, worries economists of all stripes — not just “mainstream” economists, but also traditional Keynesians and heterodox economists.1

They added:

A key aspect of MMT is that it seems to present a cost-free solution to many economic and social problems. While a critique of current monetary and fiscal policy approaches may certainly be warranted, proponents of MMT go one step further. As we argue in this brief, implementing MMT would reverse the role of policy institutions and would fundamentally change the nature of U.S. currency both domestically and internationally. Arguably, implementing MMT policy prescriptions would therefore require a fundamental overhaul of the relationship between the individual and the state, and MMT’s outcomes are potentially catastrophic. Nonetheless, some aspects of MMT are perfectly consistent with the dominant monetary paradigm in economics and are, in fact, the subject of much ongoing macroeconomic research and debate. But MMT differs greatly in its policy prescriptions.

After that the said:

The idea that a government, as the monopoly issuer of currency, can always print money to cover budget deficits and fund government spending may appear reasonable. But it flies in the face of mainstream economics and historical experience. We argue that its recent prominence is a product of the economic context of the past 25 years, where both interest rates and inflation were low. But in the end, MMT provides only an untested set of statements about the consequences of monetary policy.

The old maxim that when in a hole a person should stop digging clearly passed these authors by. There claims are, to be polite, wrong, but are typical of many made by opponents of MMT.

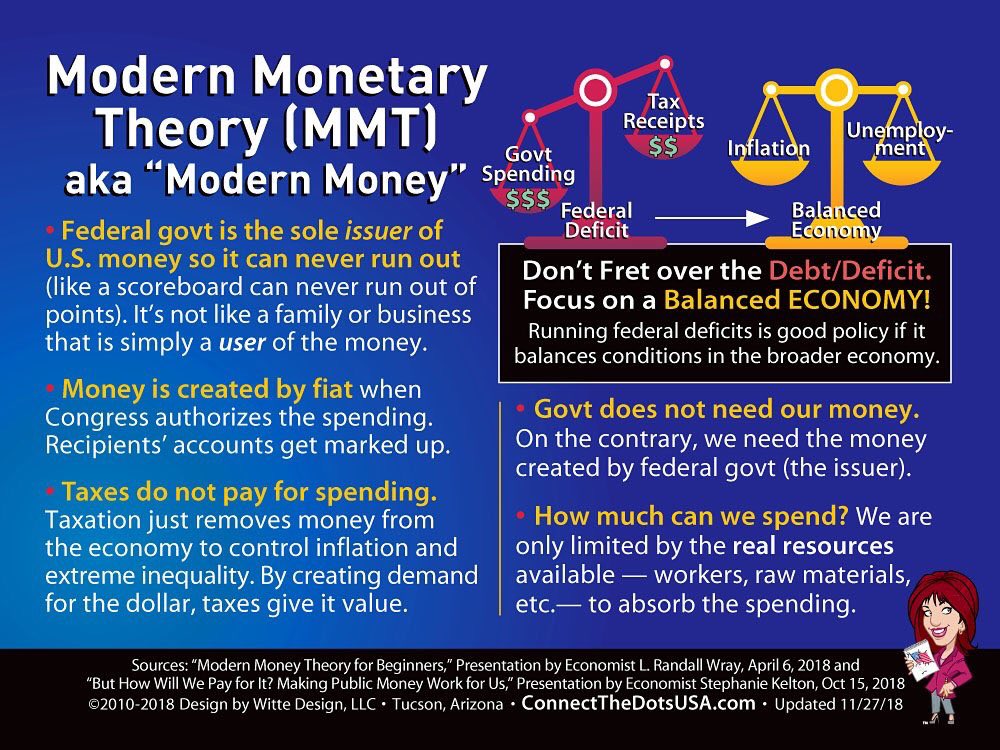

First of all, MMT need have no policy prescription attached to it. What it describes is the way that money operates in a fiat money economy. That is it.

What it most definitely adds is that there is a limit to the extent to which money may be created. That limit is reached at full employment. The idea that MMT says there may be money creation without limit is so grossly wrong it is absurd: what it emphatically says is the exact opposite. It recognises the real physical limits of the economy. The authors do not even hint of their awareness of that. It makes one wonder how much they have actually read about MMT. They only reference one MMT article by an MMT author, which is by Stephanie Kelton, but rather more by opponents.

What they have emphatically also not realised, or deliberately ignore, is that MMT has a very strong focus on inflation control.

They also, therefore, ign0re the role of tax in MMT, even though they read an edition of the Real World Economic Review where I had an article that discussed the role of tax within MMT.

And despite all their claims as to the threat to the US way of life that they say MMT represents they do not spell this out, or explain that all it enables is a New Deal in a fiat currency era.

The fact is that these authors have written about a straw man MMT that is wholly unrelated to what MMT says. This is normal, but it still is too readily believed by people like the Labour Party, who’d rather deal with false versions of MMT than real ones.

At some time when these combined neoliberal opponents of MMT realise that their prescriptions don’t work they will have to turn to what might. Then MMT will have its day.

And how do I know they are neoliberal? The authors say this:

When inflation is low and inflation expectations are well-anchored by central bank credibility, then the central bank may have more elbow room for expansionary monetary policy. Arguably, none of this analysis is controversial or inconsistent with mainstream macroeconomic thinking or MMT. What distinguishes the latter from the former is an apparent disregard, at least in the public debate, for obvious constraints on government spending.

In other words, they are wedded to the idea that democracy should not be in control of economic policy and that a coterie of central bankers, obsessed with oppressive mechanisms of control for consumer but not asset price inflation should run the economy. That’s neoliberal to the core, and they’ll make up whatever is necessary to defend it.

Be the first to comment