The last time the French successfully led a European unity initiative was in May 1950. WWII still cast a heavy shadow over Europe, and France’s foreign minister Robert Schuman invited Germany’s chancellor Konrad Adenauer to join in creating a European Coal and Steel Community. Adenauer exclaimed to his aides, “Das ist unser Durchbruch” (“This is our breakthrough”), and readily agreed (Judt 2006). For Germany, Europe was a way to regain international legitimacy.

Later the same year, when the Americans insisted on allowing Germany to rearm, the French reluctantly proposed a European Defence Community (EDC), which would merge national armies into a European army supported by a European budget. The EDC Treaty, signed in May 1952, remains to this date Europe’s farthest-reaching attempt at political union. Adenauer reluctantly agreed to the arrangement, which would have placed German soldiers in clearly inferior ranks in the European army. But, in August 1954, the French National Assembly backed out of the agreement. The unity drive had run out of steam. French Prime Minister Pierre Mendès-France complained, “In the EDC there was too much integration” (Judt 2006).

The Netherlands and Belgium led the next phase of European integration, culminating in 1957 in the Treaty of Rome, Europe’s greatest postwar achievement, which opened national borders to trade within Europe. German authorities were unhappy because they believed that borders should be opened to all countries, not just European nations. French leaders opposed the Treaty of Rome because they believed that borders should not be opened at all, even to European nations. As the price for agreeing, the French installed the egregious Common Agricultural Policy (CAP), a system of subsidies for European farmers that helped undercut farmers in developing countries and even today remains a financial drag on the meagre EU budget.

A narrative of Franco-German friendship first emerged in the lead-up to the Franco-German Treaty of Friendship, the Élysée Treaty, signed in January 1963 (Figure 1). French President Charles de Gaulle viewed the Élysée Treaty as a way of creating a united European front against the US’s economic and political might. But Adenauer needed the reassurance of the US’s political and military support; and US President John F. Kennedy was anxious to retain Germany as an important political ally. Thus, in May 1963, the German Bundestag, while ratifying the Élysée Treaty, introduced in the Treaty’s preamble language that recognised Germany’s special relationship with the US. Upon hearing of the Bundestag’s changes, de Gaulle famously moaned, “Treaties, you see, are like girls and roses. They last while they last” (Deutsche Welle 2012). Kennedy, on the other hand, travelled to Germany in June and won the hearts of adoring West Berliners when twice in a short improvised speech he declared, “Ich bin ein Berliner”(“I am a Berliner”).

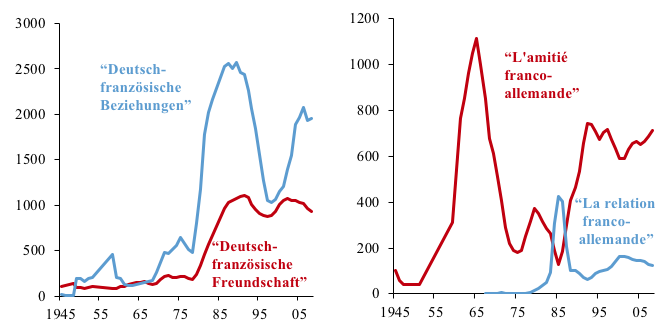

Figure 1 The narrative of Franco-German friendship ebbs and flows

(frequency of reference to “Franco-German relationship” and “Franco-German friendship” in books digitised by Google)

Note: The figure was created using the Google Books Ngram Viewer (https://books.google.com/ngrams/info). It reports the frequency with which the phrases “Franco-German relationship” and “Franco-German friendship” are mentioned in English-language books scanned by Google.

Although the impetus from the Élysée Treaty faded, a narrative evolved that, if not friendship, at least a constructive transactional ‘relationship’ existed between the two European nations. The phrase “Franco-German friendship”, although relegated to secondary status, remained alive and was periodically recharged to temporarily mask differences in the two nations’ interests.

The narrative of Franco-German cooperation grew to a crescendo in the run-up to Europe’s single currency, the euro. In fact, however, relations between France and Germany were fraught during these years. Starting with President George Pompidou in 1969, successive French presidents – Valéry Giscard d’Estaing and François Mitterrand – pushed for a single European currency, believing that by eliminating the humiliation of regular French franc devaluations, France would gain greater equality with Germany (Mody 2018b: Chapters 1 and 2). German chancellors pushed back. Starting with Willy Brandt and continuing with Helmut Schmidt and then Helmut Kohl in his first two terms, German chancellors emphasised that a single currency was ill-suited for divergent economies. When Schmidt briefly seemed to concede ground to Giscard d’Estaing, the Bundesbank held him back.

Many have speculated that after the fall of the Berlin Wall in November 1989, Kohl agreed to satisfy Mitterrand’s obsession with a single European currency in return for France’s green light to unify East and West Germany. There is no evidence to support this speculation. Kohl was backed US President George H.W. Bush, who viewed German unity as a central objective of US foreign policy. Kohl bought the acquiescence of Soviet leader Mikhail Gorbachev with a generous financial contribution to prop up the teetering Soviet Union (Mody 2018b: 78). Elisabeth Guigou, one of Mitterrand’s closest advisors, says that she was present at every meeting between Mitterrand and Kohl, and the idea of a quid pro quo never came up (Schabert 2009: 248).

Kohl did change his position. From 1991 on, he pushed the single currency with boundless vigour for the rest of the decade. Why he did so we will probably never know, because he operated with great autonomy, relying on a close circle of advisors. Superficially, Kohl gave the French the euro, but he did so on German terms. The French wanted a European central bank under political supervision; Kohl, following the Bundesbank model, insisted on a hyper-independent central bank. The French wanted a European fiscal framework that allowed national policy discretion; Kohl insisted on a rigid framework centred on a budget deficit limit of 3% of GDP. At the Amsterdam summit in June 1997, French leaders pleaded to have the fiscal framework also reflect the goal of fostering economic growth. Kohl agreed only to a name change – the system of fiscal rules would be called the Stability and Growth Pact, rather than the Stability Pact. Philip Stephens of the Financial Times commented: “We are accustomed to Eurofudge, but rarely has it been so richly sweetened with cynicism” (Stephens 1997). A year later, Kohl made another fateful decision. Despite fierce opposition from his advisors, he insisted that Italy join the euro area with the first batch of members (Mody 2018b: 120).

After the euro’s introduction on 1 January 1999, German Chancellor Gerhard Schröder and French President Jacques Chirac continued a tense relationship, sparring at the Nice summit in December 2000 over the allocation of voting rights in the EU’s governance. The narrative of Franco-German friendship nevertheless continued, reaching a new fervour in German and French scholarship, curiously enough, around 2002–2003 (see Figure 2). Those were indeed years of rare coincidence in German and French national interests. Both countries were struggling to bring their fiscal deficits below the 3% of GDP limit. Hard pressed by the intrepid European Commission President Romano Prodi, Schröder and Chirac pushed back against any imposition of penalties specified under the rules. Prodi recognised that the rules were “stupid,” but he felt compelled as European Commission president to implement them. German and French leaders, rather than making an effort to undo the rules, merely waved them aside.

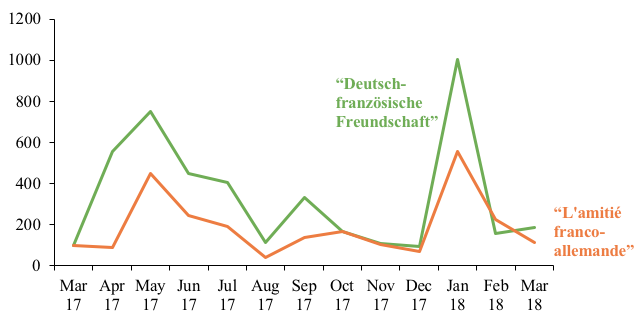

Figure 2 The Germans believe in a relationship with France; the French seek friendship

(references to “friendship” = 100 in 1945)

Note: Three-year moving average. “Deutsch-französische Freundschaft” and “L’amitié franco-allemande” in 1945 equals 100. The figure was created using the Google Books Ngram Viewer (https://books.google.com/ngrams/info). It reports the frequency with which the phrases “Deutsch-französische Freundschaft,” “Deutsch-französische Beziehungen,” “L’amitié franco-allemande,” and “La relation franco-allemande” are mentioned in German- and French-language books scanned by Google.

When the Global Crisis reached its most fearsome phase after the fall of Lehman Brothers in September 2008, US authorities established a $700 billion financial rescue fund, the Troubled Assets Relief Program (TARP). Under pressure to take an equivalent initiative, French President Nicolas Sarkozy proposed a similar European fund. German Chancellor Angela Merkel and her finance minister Peer Steinbrück peremptorily dismissed the idea. In December 2012, at the height of the euro area crisis, Herman Van Rompuy, president of the European Council (the gathering of European heads of government), proposed a euro area budget to assist countries in trouble. At the Brussels summit later that month, an annoyed Merkel asked: “Where is the money supposed to come from?” When French President François Hollande helpfully suggested that the intention was to create a “solidarity mechanism,” Merkel nixed the idea, repeating: “And where is the money supposed to come from?” (Mody 2018b: 324).

Through the global and euro area crises, Merkel ensured that the German taxpayer was called on only to do the bare minimum to prevent the euro area from imploding. She firmly squashed fanciful ideas such as euro area budgets and eurobonds (bonds that would carry the joint guarantee of repayment by euro area governments).

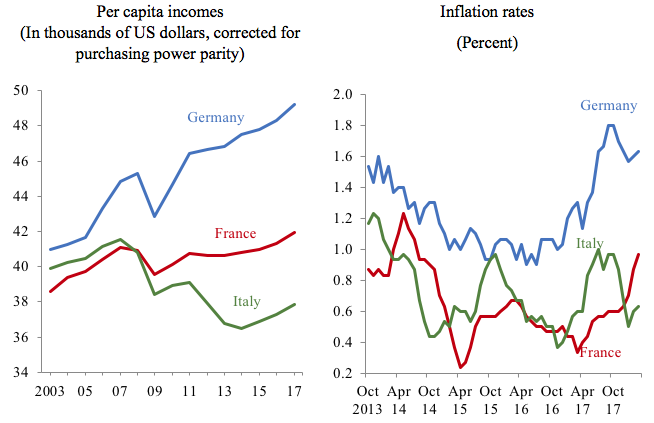

In May 2017, Emmanuel Macron became French president with a promise that he would persuade a reluctant Germany to agree to a euro area budget. A new hope was kindled. The media quickly revived the narrative of Franco-German friendship (see Figure 3). Macron gave stirring speeches in Athens and at the Sorbonne in Paris (Macron 2017a: 2017b). He invoked warm but fuzzy themes, especially a call for European sovereignty. The narrative of Franco-German friendship quickly began to fade, but it was reinvigorated in January 2018, the 55th anniversary of the Élysée Treaty. A romantic view of that treaty bolstered the sense that Germany’s substantial economic lead over France and the differences in the two countries’ national interests could be overcome by a common desire to promote European unity.

Figure 3 Macron’s election revives the Franco-German friendship narrative

(monthly, March 2017=100)

Source: Factiva. This figure reports the frequency with which the phrases “Deutsch-französische Freundschaft” and “L’amitié franco-allemande” are mentioned in Factiva’s global news database.

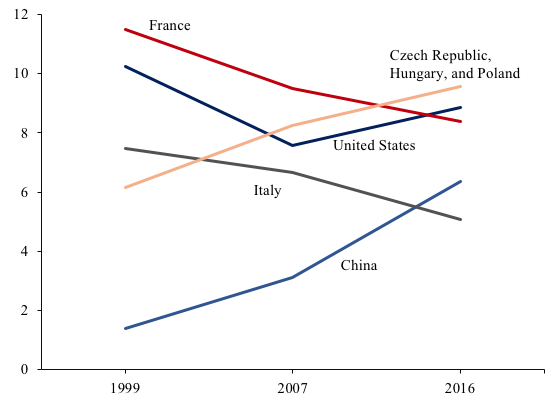

The prospects don’t look good. However daring and appealing Macron’s European vision may be, France has fallen so far behind Germany that any partnership between the two countries is unrealistic. While the German economy recovered quickly from the Global Crisis, the French economy stalled and the country’s inflation rate fell into near deflationary territory (see Figure 4). France’s economic woes during the crisis years reflect deep-rooted economic weaknesses. France is one of the few advanced countries with an expanding ‘informal’ or ‘shadow’ economy. The shadow economy’s expansion reflects a weak governance system, with France substantially below Germany in the World Bank’s governance metrics. Weakness in such metrics is associated with low long-term growth rates, as a ECB study shows (Masuch et al. 2017). As further evidence of the French economy’s weakness, the innovative energy of French firms is dissipating (Mody 2018b: 393).

Figure 4. The great divergence in euro area incomes and inflation

Sources: Conference Board, “Total Economy Database (Adjusted Version)“; Eurostat.

Note: Core inflation is the annual percentage change in the Harmonized Index of Consumer Prices excluding unprocessed food and energy.

The German economy has its own troubles, as Marcel Fratzscher (2018) highlights. But set against Germany’s, France’s challenges are staggering. The French government’s extraordinarily high expenditures have been stuck above 55% of GDP. Soon after Macron was elected, the inimitable European Commission President Jean-Claude Juncker said, “We have a real problem with France. The French spend too much money and spend it on the wrong things” (Saeed 2017). Because of its high expenditures, the French government struggles to rein in its budget deficit below 3% of GDP. Its debt-to-GDP ratio remains stubbornly close to 100% of GDP. In contrast, the German government spends about 45% of GDP, now runs a budget surplus, and its debt-to-GDP ratio at 65% of GDP is quickly falling.

Even more worrisome for France are its long-standing social problems. The traditionally high youth unemployment rate rose during the crisis. And for a country that boasts such a large government expenditure outlay, France has amongst the lowest rates of upward intergenerational mobility in Western democracies. Annie Genevard, who served on the French Parliament’s committee for cultural affairs and education, said in December 2016, “France retains its sad title as champion of social inequalities at school” (France 24 2016). Such social divisions ultimately are a drag on long-term growth prospects.

The widening economic gap between France and Germany is starkly evident in international trade flows. Two decades ago, France was the prime destination for German exporters (see Figure 5). Since then, the share of exports to France has fallen sharply, while exports to three non-euro area European economies – the Czech Republic, Hungary, and Poland – have steadily increased. With German exporters looking increasingly to China, Franco-German trade ties are set to weaken further.

Figure 5 German exporters shift their sights away from the euro area

(percent of total German exports to the various countries)

Source: IMF data.

Although Macron seems to recognise France’s handicaps, the measures he has taken so far barely make a dent in addressing the country’s enduring problems. Indeed, to the extent that his labour market reforms create more temporary and precarious jobs, the level of social anxiety will remain high. His promise to create greater social insurance is restricted by the realities of French budgetary stresses. And education reforms have so far remained caught in bureaucratic tangles.

A new vision for the future of Europe – even if stirred rhetorically by a mythical Franco-German friendship – cannot be based on a redesign of the euro area. The single monetary policy under the euro will always favour either Germany or France, and, hence, will continue to divide rather than unify (Mody 2018a). For Europe to move forward, the primary tasks are at home: to rebuild economies in long-term decline, especially when measured against the most dynamic countries in the world. At the same time, governments need to sensitively address social stresses. German leaders have their own homework to do; for France’s leaders, their task at home is the monumental challenge for the next generation.

References

Deutsche Welle (2012), “The Élysée Treaty: A Model for Other Old Enemies,” 23 September.

France 24 (2016), “French Students Most Affected by Social Inequality, OECD Finds,” 14 December.

Fratzscher, M (2018), The German Illusion. New York: Oxford University Press.

Judt, T (2006), Postwar: A History of Europe since 1945. New York: Penguin Group US.

Macron, E (2017a), “Speech by the President of the French Republic,” 7 September, Athens.

Macron, E (2017b), “Initiative for Europe,” 26 September, Sorbonne University, Paris.

Masuch, K, E Moshammer, and B Pierluigi (2017), “Institutions, Public Debt, and Growth in Europe,” Public Sector Economics 41(2): 159–205.

Mody, A, (2018a), “The Euro Area’s Deepening Political Divide,” VoxEU.org, 21 March.

Mody, A (2018b), EuroTragedy: A Drama in Nine Acts. New York: Oxford University Press.

Saeed, S (2017), “Juncker: ‘The French Spend Too Much Money.’” Politico, 18 May.

Schabert, T (2009), How World Politics Is Made: France and the Reunification of Germany. London and Columbia: University of Missouri Press.

Stephens, P (1997), “The Ragbag Treaty: EU Leaders Ignored the Real Issues at Amsterdam Summitm,” Financial Times, 20 June.

Be the first to comment