What is being conveniently presented as Modern Monetary Theory by governments to save corporations is in many ways quite different than the leading MMT scholars have advocated.

Yeva Nersisyan is an associate professor of economics at Franklin and Marshall College. Senior Scholar

L. Randall Wray is a professor of economics at Bard College.

Cross-posted from the Levy Institute of Bard College

Modern Money Theory (MMT) has been thrust into the spot-light again, as numerous governments around the world respond to the pandemic. Unfortunately, those invoking MMT misrepresent its main tenets. For example, we are being told MMT calls for helicopter drops of cash or having the Federal Reserve finance government spending through rebooted quantitative easing.

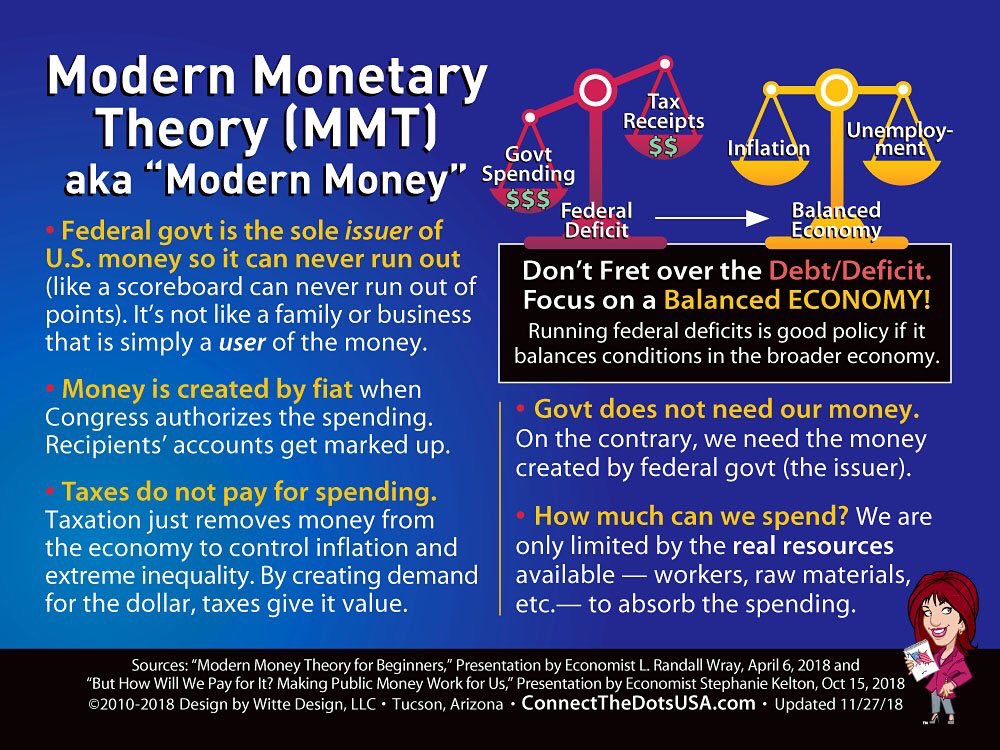

This is not MMT, which provides an analysis of fiscal and monetary policy applicable to national governments with sovereign, nonconvertible currencies. It concludes that the sovereign currency issuer (1) does not face a “budget constraint” (as conventionally defined), (2) cannot “run out of money,” (3) meets its obligations by paying in its own currency, and (4) can set the interest rate on any obligations it issues.

Current procedures adopted by the Treasury, the central bank, and private banks allow government to spend up to the budget approved by Congress and signed by the president. No change of procedures, no money printing, no helicopter drops are required. Modern governments use central banks to make and receive all payments through private banks.

When the Treasury spends, the Fed credits a bank’s reserves, and the bank credits the deposits of the recipient. Taxes reverse that, with reserves and the taxpayer’s deposit debited. This is all accomplished through keystrokes—something government cannot run out of. Both the Treasury and the Fed can sell bonds (in the new issue and open markets, respectively) to offer banks higher returns than they get on reserves.

As MMT explains, since reserves must be exchanged when purchasing government bonds, the reserves must be supplied first before bonds can be purchased. It demonstrates how the Fed provides the needed reserves even as it upholds the prohibition against “lending” to the Treasury by never buying the bonds directly. None of this is optional for the Fed. It cannot refuse to clear government checks, nor can it refuse the reserves banks need to clear payments. It is the government’s bank, after all, and is focused on the stability of the payments system.

Government can make all payments as they come due. Bond vigilantes cannot force default, although their portfolio preferences could affect interest rates and exchange rates. But the central bank’s interest rate target is the most important determinant of interest rates on the entire structure of bond rates. Bond vigilantes cannot hold the nation hostage—the central bank can always overrule them. In truth, the only bond vigilante we face is the Fed. And in recent years it has demonstrated a commitment to keeping rates low. In any event, the Fed is a creature of Congress, and Congress can seize control of interest rates if it wishes to do so.

Finally, the Treasury can “afford” to make all payments on debt as they come due, no matter how high the Fed pushes rates. Affordability is not the issue. The issue will be over the desirability of making big interest payments to bondholders. If that is seen as undesirable, Congress can tax away whatever it deems excessive.

What we emphasize is that sovereign governments face resource constraints, not financial constraints. We have always argued that too much spending—whether by government or by the private sector—can cause inflation. Below full employment, government spending creates “free lunches” as it utilizes resources that would otherwise be left idle. Unemployment is evidence that the country is living below its means. Full employment means that the nation is living up to its means. A country lives beyond its means only when it goes beyond full employment, when more government spending competes for resources already in use—which could cause inflation.

MMT rejects the analogy between a sovereign government’s budget and a household’s. The difference between households and the sovereign holds true in times of crisis and also in normal times, regardless of the level of interest rates and existing levels of outstanding government bonds (i.e., national debt). The sovereign can never run out of finance—period.

MMT does not advocate policy to ramp up deficits. A bud-get deficit is an outcome, not a goal or policy tool to be used in recession. There is no such thing as “deficit spending” to be used in a downturn or crisis. Government uses the same procedures no matter the budgetary outcome—which will not be known until the end of the fiscal year, as it depends on the econ-omy’s performance. The spending will have occurred before we even know the end-of-the-year budget balance.

An important lesson to learn from the COVID-19 crisis is that the government’s ability to run deficits is not limited to times of crisis. Indeed, it was a policy error to keep the economy below full employment before this crisis hit in the belief that government spending was limited by financial constraints. Ironically, the real limits faced by government before the pandemic were far less constraining than the limits faced after the virus had brought a huge part of our productive capacity to a halt.

We hope this pandemic will teach us that in normal times we must build up our supplies, our infrastructure, and our institutions to be able to deal with crises. We should not wait for the next national crisis to live up to our means.

Be the first to comment