Are the measures being used by central banks attempting to reduce inflation effective or necessary?

Michael Roberts is an Economist in the City of London and a prolific blogger

Cross-posted from Michael’s Blog

Creative Commons Attribution-Share Alike 2.5 Generic

“The inflation that we got was not at all the inflation that we were looking for,” US Federal Reserve Chair Jay Powell said in his press conference after the Fed’s monetary policy committee decided to accelerate the ‘tapering’ of its bond purchases to zero by March 2022 and suggested that it will start to hike its policy interest rate (the ‘Fed funds’ rate) from zero soon after that.

What did Powell mean by ‘not the inflation we were looking for’? He did not mean just the level of the inflation rate. Headline US consumer goods and services inflation is now much higher than the Fed forecast back in September at its last meeting. And so is what is called ‘core inflation’, which excludes fast-rising energy and food prices. Headline inflation reached 6.5% in November, the highest rate for nearly 40 years.

But Jay Powell was also referring to the causes of that inflation rate. It seems that the Fed no longer considers the rise in inflation as ‘transitory’ but likely to hang around for some time, although its median forecast is for the personal consumption inflation (PCE) rate to finish at 5.3% for 2021 but then drop back to 2.6% in 2022 and eventually fall to 2.1% by 2024. In that sense, the Fed still reckons inflation is ‘transitory’ but it will be higher than previously thought, in the short term.

The reason that there is an ‘unexpected’ sort of inflation, Powell reckons, is due to the extraordinary circumstances of the pandemic. A normal rise in inflation, according to mainstream theory, would be too much money injected into the banking system, or the result of ‘tight’ labour markets (ie low unemployment) and strong consumer demand as the economy expands. That is happening, says Powell, but there is the pandemic factor on top of that: “These problems have been larger and longer-lasting than anticipated, exacerbated by waves of the virus.”

In other words, the pandemic has made inflation worse because of 1) pent-up consumer demand as people run down savings built up during lockdowns and 2) supply ‘bottlenecks’ arising in trying to meet that demand – these bottlenecks being created by the restrictions on the international transport of goods and components and continued restrictions on supply – because much of the world is still suffering from the pandemic.

Thus, the Fed is in a dilemma. If it ‘tightens’ monetary policy ‘too much’ and hikes interest rates ‘too quickly’, it could cause the cost of borrowing to invest or spend to rise to the point where new investment in technology slows and consumer demand for products fizzles out and there is an economic slump. This is particularly the case, given the record high level of corporate debt. Alternatively, if it does not act to reduce and stop its monetary injections and raise rates, then high inflation may not be transitory at all.

The result is the Fed is looking for a middle way. The same applies to the Bank of England and the European Central Bank, both of which met this week too. The inflation rates in the Eurozone and the UK have also hit new highs.

UK inflation rate % yoy

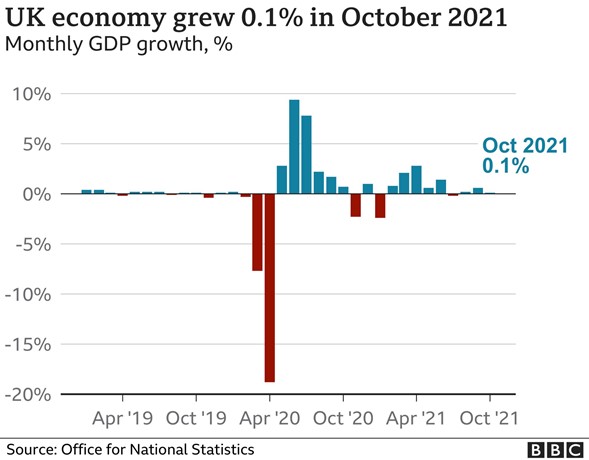

In response, the Bank of England has adopted a slightly different approach. It hiked its policy rate by 0.25% but did not reduce its bond purchases. The BoE is more worried about stagflation than the Fed. The inflation rate could stay higher for longer in Britain because of the impact of Brexit on imported goods prices and the loss of labour from EU immigrants returning to Europe. Moreover, the UK economy is slowing down already, even before the Omicron variant bites.

The ECB is staying more ‘dovish’, because inflation has risen less than in the US or the UK and economic recovery has been slower. Also, the pandemic variants are spreading fast in Europe. So the ECB did not raise rates at its meeting and only rejigged its bond purchases slightly. QE remains in place in the Eurozone and any interest rate hikes are pushed well back into 2023.

Eurozone inflation yoy %

In my view, the dilemma for these central banks is between controlling inflation and avoiding a slump is a false one. That’s because monetary policy (injecting or withdrawing credit money or hiking or lowering policy rates) is really ineffective in managing inflation or economic activity. Study after study has shown that ‘quantitative easing’ had little or no effect on boosting the ‘real’ economy or production and investment; and study after study has shown that huge injections of money credit by central banks over the last 20 years have not led to an acceleration of inflation – on the contrary. So whether the Fed, BoE or ECB speed up the tightening of monetary policy will not work to ‘curb inflation’. Monetary policy does not work – at least at the levels of interest rates that central banks are envisaging.

Of course, if the Fed were to resort to interest rates that produced a high positive real interest rate (ie after inflation), similar to what former Fed chair Volcker did to end the high inflation rates of the 1970s, that might work. The federal funds rate reached a record high of 20 percent in late 1980 while inflation peaked at 11.6% in March. But as Volcker found, it still took years to achieve lower inflation and only after suffering the deepest economic slump of the post-war period to date ie 1980-82.

Why is monetary policy ineffective? As I have argued in previous posts, it’s because inflation is not a ‘monetary phenomenon’ as the monetarist Milton Friedman argued. Nor is it the product of wage costs pushing up prices – despite attempts by UK government economists to claim so. Recently, UK treasury economists warned that “public sector pay increases” could “exacerbate temporary inflation pressure” by contributing to higher wage demands across the economy… and of a “trade off” between higher pay rises and recruiting more staff/ public services investment. This argument is more to do with avoiding paying public sector workers decent wages than dealing with inflation.

I remind readers of this blog what I pointed out before. There has never been ‘wage push’ inflation. Indeed, over the last 20 years until the year of the COVID, real weekly wages rose just 0.4% a year on average, less than the average annual real GDP growth of around 2%+. It’s the share of GDP growth going to profits that rose. Marx argued that when wages rise, that will not lead to price rises but instead to a fall in profits and that is the real reason why mainstream economics makes so much fuss about wage-push inflation.

If there is going to be any ‘cost-push’ this year, it’s going to come from companies hiking prices as the cost of raw materials, commodities and other inputs rise, partly due to ‘supply-chain’ disruption from COVID. The FT reports that “price rises have emerged as a dominant theme in the quarterly earnings season which kicked off in the US this month. Executives at Coca-Cola, Chipotle and appliance maker Whirlpool, as well as household brand behemoths Procter & Gamble and Kimberly-Clark, all told analysts in earnings calls last week that they were preparing to raise prices to offset rising input costs, particularly of commodities.”

Instead, the inflation of the prices of production depends ultimately on what is happening to the generation of new value in an economy – and that depends on the rate of accumulation of capital and the profitability of that capital. Inflation rates reached post-war lows in the 2010s despite ‘quantitative easing because real GDP growth slowed along with investment and productivity growth. All monetary policy did was weakly counteract that downward pressure on price inflation.

On the other hand, ‘monetary easing’ did fire up financial speculation and a stock and bond market boom, as the zero cost of borrowing plus unlimited supplies of money fed into financial and property markets. There was plenty of inflation there. So as the velocity of money (the turnover of transactions in the ‘real’ economy) dropped, reducing the impact of monetary injections on productive investment and prices of goods and services, prices of financial and other unproductive assets like property rocketed.

Inflation now is ‘transitory’ in the sense that after the ‘sugar rush’ of consumer and investment spending ends during 2022, growth in GDP, investment and productivity will drop back to ‘long depression’ rates. That will mean that inflation will subside. The Fed is forecasting just 2% real GDP growth by 2024 and 1.8% a year after that – a rate lower than the average for the last ten years. In Q3 2021, US productivity growth slumped on the quarter by the most in 60 years, while the year on year rate dropped 0.6%, the largest decline since 1993, as employment rose faster than output.

Some optimists argue that there will be a boom in capital spending on new technology, automation etc that will drive the productivity of labour upwards. But the profitability of capital accumulation in all the major economies remains depressed and near all-time lows despite a recovery in 2021.

As Brian Green put it in his recent post:

“It is likely that demand driven inflation has subsided. It seems with Covid Funds now used up, US consumers are joining the rest of the world in retrenching while container vessels continue to queue outside ports to load and unload. What remains is supply bottlenecks as well as gaming the system. Pipeline inflation or factory gate inflation is evident. Both the US and the UK released record or near record producer prices. When pipeline inflation cannot be satisfied by demand, it is profit margins that suffer and that is what is happening now and it will intensify in the new year.”

And the Omicron and Delta variants of COVID are affecting the production of goods and services. The latest surveys of economic activity for December (called the PMIs) showed a significant slowdown in the pace of recovery from the pandemic slump. The UK and Eurozone measures are now at nine-month lows.

Is the stagflation (low growth and high inflation) of the 1970s coming back? Well, the stag part seems very likely; the inflation part will depend on factors beyond the central banks’ control because it is not the sort of inflation that Jay Powell was expecting.

BRAVE NEW EUROPE has begun its Fundraising Campaign 2021

Support us and become part of a media that takes responsibility for society

BRAVE NEW EUROPE is a not-for-profit educational platform for economics, politics, and climate change that brings authors at the cutting edge of progressive thought together with activists and others with articles like this. If you would like to support our work and want to see more writing free of state or corporate media bias and free of charge. To maintain the impetus and impartiality we need fresh funds every month. Three hundred donors, giving £5 or 5 euros a month would bring us close to £1,500 monthly, which is enough to keep us ticking over.

Please donate here

Be the first to comment