Banks are making massive profits on European Central Bank interest rate rises, with German and French banks making the most

Cross-posted from Positive Money Europe

THE ECB is expected to pay around €40 billion in net interest income to banks on the overnight deposits that they keep with the central bank. This estimated figure will jump to €53.7 billion if the ECB decides to increase the interest rate on its deposit facility (DF) from the current 1.5% to 2% on December 15. France and Germany expected to profit the most in absolute terms. We provide the implications of these purely accounting-induced profits for the wider banking system and the real economy.

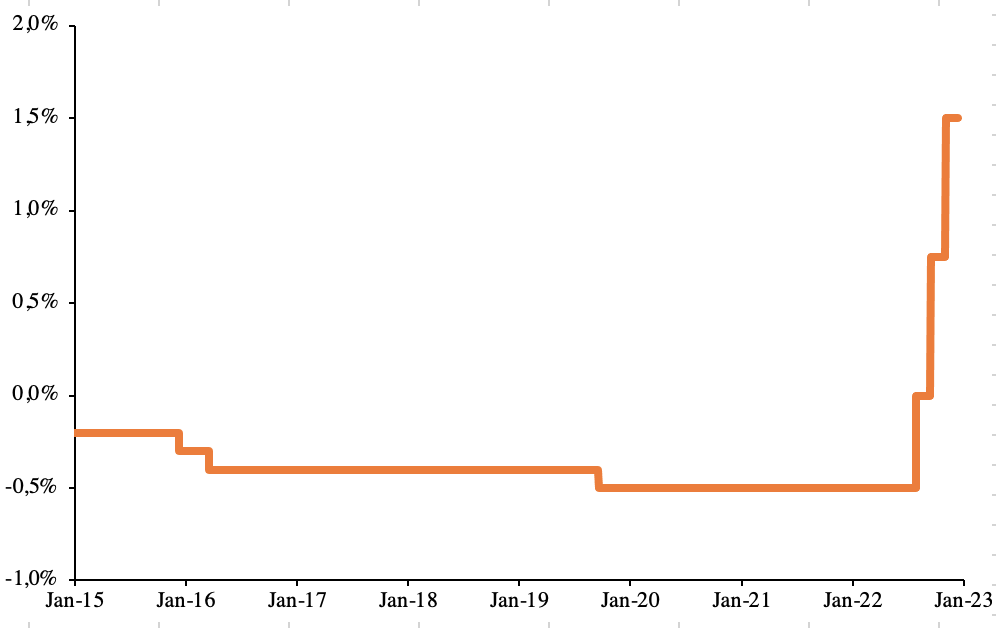

Before July 2022, monetary policy functioned quite differently from how it is now. The DF rate was negative as well as the rate set on the TLTRO III. This meant that banks in the euro area would pay the central bank to deposit their reserves, while they were remunerated positively on their TLTRO loans that they borrowed from the ECB. Since July, there have been three successive rate hikes on the DF, which increased the rate from -0.5% in July to 1.5% in November 2022. The ECB is expected to announce another rate hike, of around 0.5%, during its Governing Council meeting on December 15.

The effect of sudden and successive interest rate hikes means that the rate that the ECB pays on the funds that banks deposit with the ECB is now squarely positive. In other words, banks get a positive return on their deposit with the ECB.

Figure 1. Deposit facility rate since 2015

Source: ECB

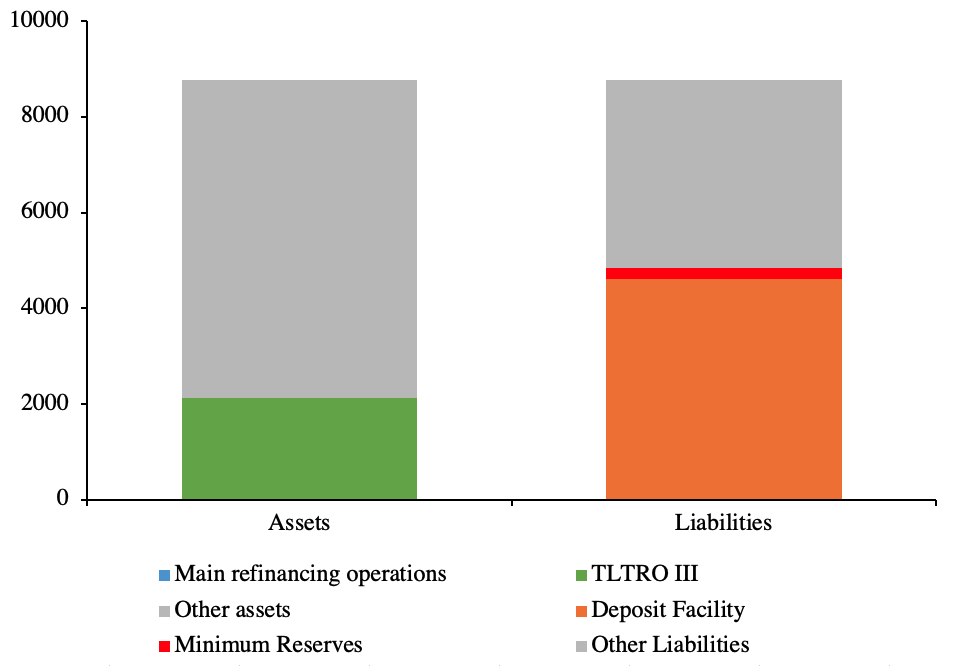

While DF rate turned positive and increased, the conditions on TLTROs were not. As such, from September (when the DF rate increased from 0% to 0.75%) until November 2022, banks profited both from the positive DF rate and what they got from the ECB on their TLTRO loans, which were loans at rates -0.5% to as low as -1%. Moreover, banks would deposit their TLTRO loans into the DF to gain from an even bigger interest rate differential between their TLTRO rate and the DF rate. Recognizing this double loss, in November the ECB changed the conditions of the TLTRO III, which means that since November 23 banks are paying the same rate as the DF on their TLTRO loans as well. This has ended the ECB’s funding subsidy to banks.

The change in the conditions of the TLTRO III programme are welcome, but they only partially address the issue of banks profiting from interest rate hikes. Because banks have a lot more deposits with the ECB (€4.8 trillion) than they have TLTRO loans (€2.1 trillion) the ECB will end up paying banks a net interest income (NII). This NII will continue to accrue if the ECB further increases the interest rate unless the remuneration conditions on the DF are changed.

Figure 2. Consolidated balance sheet of the Eurosystem, banks’ TLTRO liabilities are Eurosystem assets (in green), banks’ deposits with the deposit facility are Eurosystem liabilities (orange), € billions

Source: ECB

If we assume a current deposit facility rate of 1.5% and use the latest Eurosystem consolidated data for October 2022, banks in the euro area are set to receive NII of €40 billion from the ECB. If the interest rate rises to 2% this figure will climb to €53.7 billion and close to €70 billion if the DF rate rises by another 0.5%.

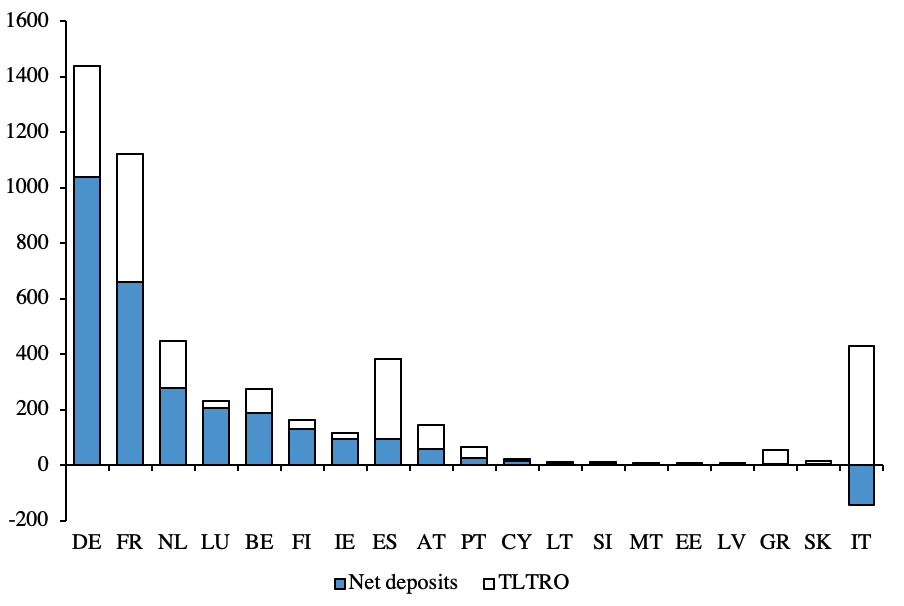

Figure 3. Net deposits, calculated as total deposits minus banks’ TLTRO liabilities remunerated at the DF rate, € billions

Source: ECB Statistical Data Warehouse, SDW

Distribution of net interest income in the Eurozone

In terms of distribution of NII, German and French banks will earn the most from their deposits with the ECB, €20.8 billion and €13.2 billion respectively. While banks in Austria, Portugal, Spain, Slovakia and Greece will benefit relatively little. In contrast, Italian banks have a net liability to the ECB. This means that the Italian commercial banks will have to pay a net interest of €2.9 billion to the central bank.

Figure 4. Net interest income assuming DF rate of 2%, € billions

Source: Own calculations

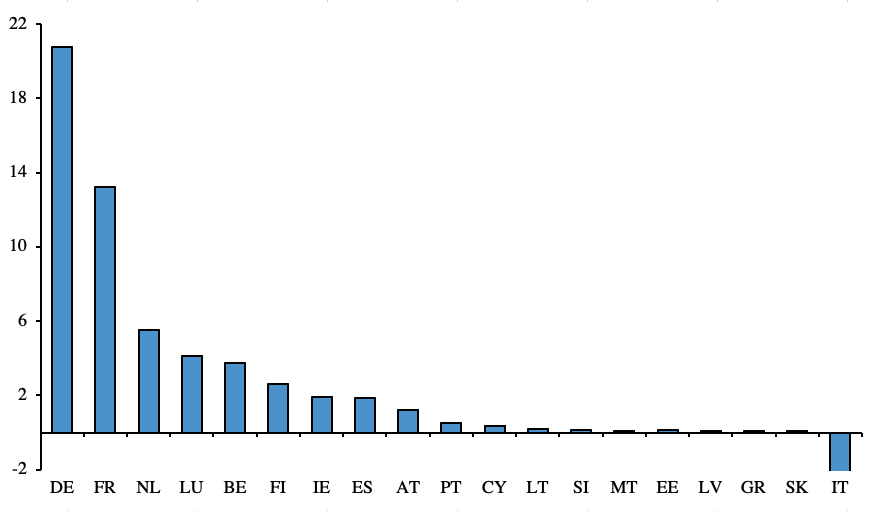

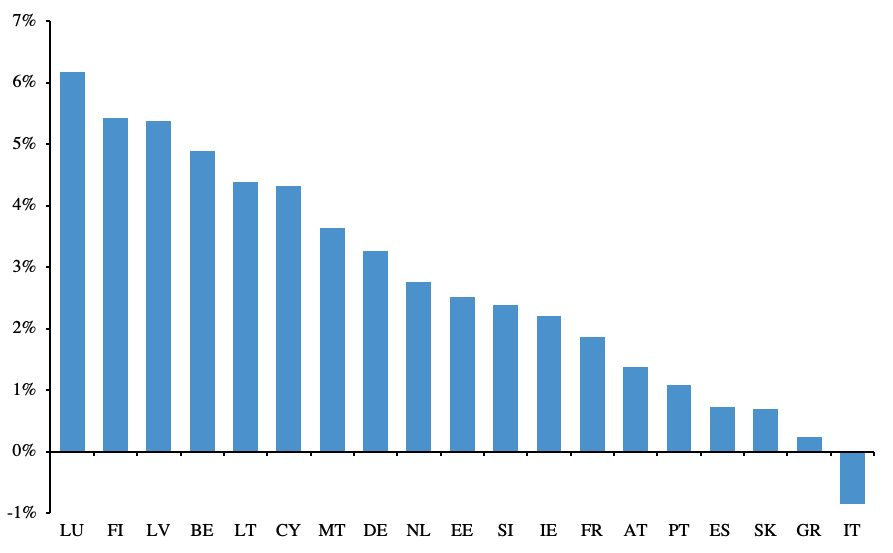

In Luxembourg, Finland and Latvia, the interest rate earned on deposits with the ECB will be more than 5% of banks’ total equity.

Figure 5. NII from the DF as a share of banks’ total equity capital, %

Source: Own calculations. Bank equity is credit institutions’ ‘capital and reserves’ from National tables – Credit institutions and money market funds balance sheets – Money, credit and banking – Reports – ECB SDW. Due to missing data, we had to estimate the equity of banks in the Netherlands, Malta and Latvia as a fraction of their total assets.

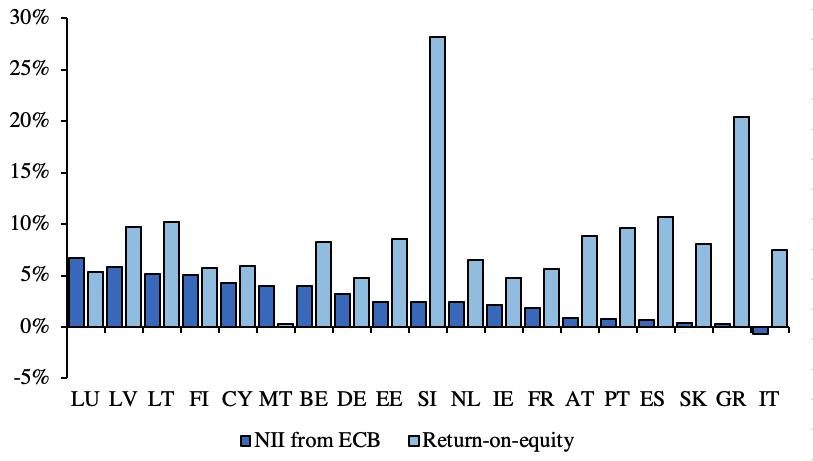

In Luxembourg and Malta, interest rates earned on the DF exceed banks’ return-on-equity, one of the main indicators of bank profitability. In Finland, Cyprus, Germany, Latvia and Lithuania, interest earnings constitute more than 50% of bank profits.

Moreover, the earnings that banks will make from a DF rate of 2% will be much larger than their “normal” return on assets, which is around 0.5%. Their average return on equity was around 8,9% in the first half of 2022. While bank profits are boosted, this comes virtually at no cost. The costs of depositing at the ECB is very low compared to banks’ “normal” operations such as issuing mortgages and administering loans and deposits.

Figure 6. NII from the ECB compared to the return-on-equity, %

Source: European Banking Authority, EBA

Note: Return-on-equity data for 1H 2022

Unless banks pass on the higher policy rate to the savings accounts of their customers, the ECB is boosting the profits of bank shareholders.

Profits earned from the deposits with the ECB, which for some banks are larger than their annual return-on-equity, are the result of an accounting trick. As such, these profits are not based on any real economic activity and should not be passed down as dividends to the shareholders.

However, currently, there is nothing stopping banks from passing down these profits to shareholders in the form of dividend payments. In 2020, the ECB recommended that banks’ dividend distribution be put on hold considering the extraordinary circumstances with the global pandemic. However, the ECB suspended these recommendations in September 2021, decided not to renew them and intends to keep it that way.

Bank shareholders should not be profiting from this while bank depositors are not.

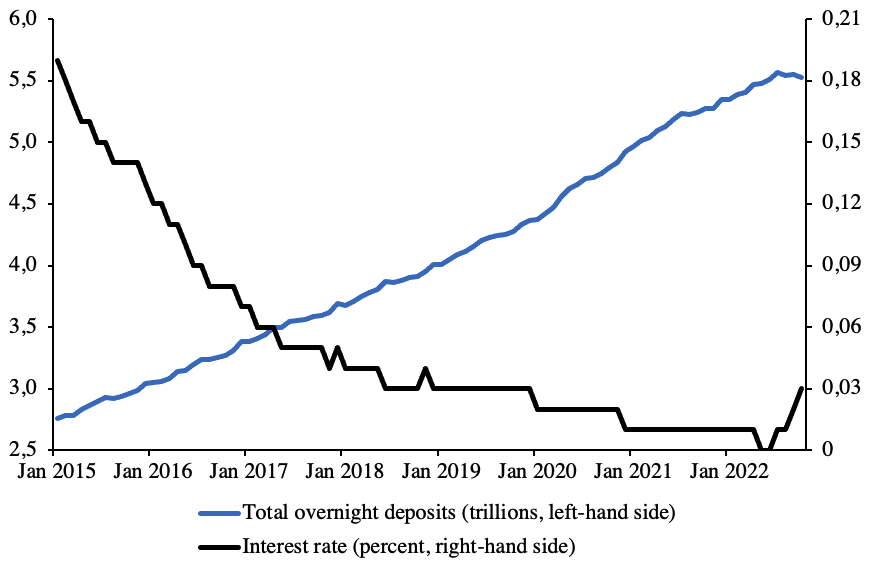

According to the data as of October 2022, banks have not passed on the higher deposit facility rate onto household savings accounts. Households in the euro area have around €9 trillion in deposits in the banking system, out of which 61% are overnight deposits and further 22% are deposits with maturity of less than 3 months. Deposit interest rates on overnight deposits is 0,03%. This further brings down banks’ funding costs, i.e. the interest rates they pay on their liabilities, to near zero levels.

Figure 7. Household overnight deposits with euro area banks and their interest rate.

Source: Euro area statistics

It would be unacceptable if profits based on a purely accounting trick are distributed to banks, while the rest of the population is going through a cost of living crisis, squeezed between demand destruction resulting from the interest rate hikes and elevated inflation resulting from the energy crisis. This is especially true since remuneration on bank liabilities remains ultra-low. That is, when banks continue to remunerate household deposits at 0.03%, while getting 1.5%-2% on their deposits with the central bank.

Be the first to comment