A very informative article concerning car sales in Europe, unfortunately once again confirming that car-makers are only concerned with profit maximisation.

By Peter Mock, Uwe Tietge, Sandra Wappelhorst

Cross-posted from the ICCT website

Starting this year, manufacturers in the European Union (EU) must comply with the next phase of mandatory CO2 standards for new vehicle fleets. An average fleet-wide target of 95 grams per kilometer (g/km) applies to 95% of the new passenger cars in 2020, and will apply to the whole new car fleet from 2021.

Looking at the market statistics for 2018 could cause one to fall into despair: The average CO2 emission level was 120 g/km, which is 2 g/km higher than in 2017 and more than 25% higher than the 2021 target. Nevertheless, there is a good chance that vehicle manufacturers will be able to meet their 2020/21 CO2 targets in time and will avoid paying any penalties. As outlined here, three Germany-based manufacturers (BMW, Daimler, and Volkswagen) will likely rely on a number of incremental improvements in their driving resistance and combustion engine technologies. In addition, they will likely take advantage of eco-innovation and super-credit flexibility mechanisms, and roll out an increasing share of vehicles equipped with mild hybrid, plug-in hybrid, or battery electric vehicle technologies. Just a few days ago, the CEO of BMW, Oliver Zipse, confirmed that the company plans to reduce its average EU new car fleet CO2 emission level by 20% in 2020 via a combination of more efficient combustion engine technologies and deploying more electric vehicles.

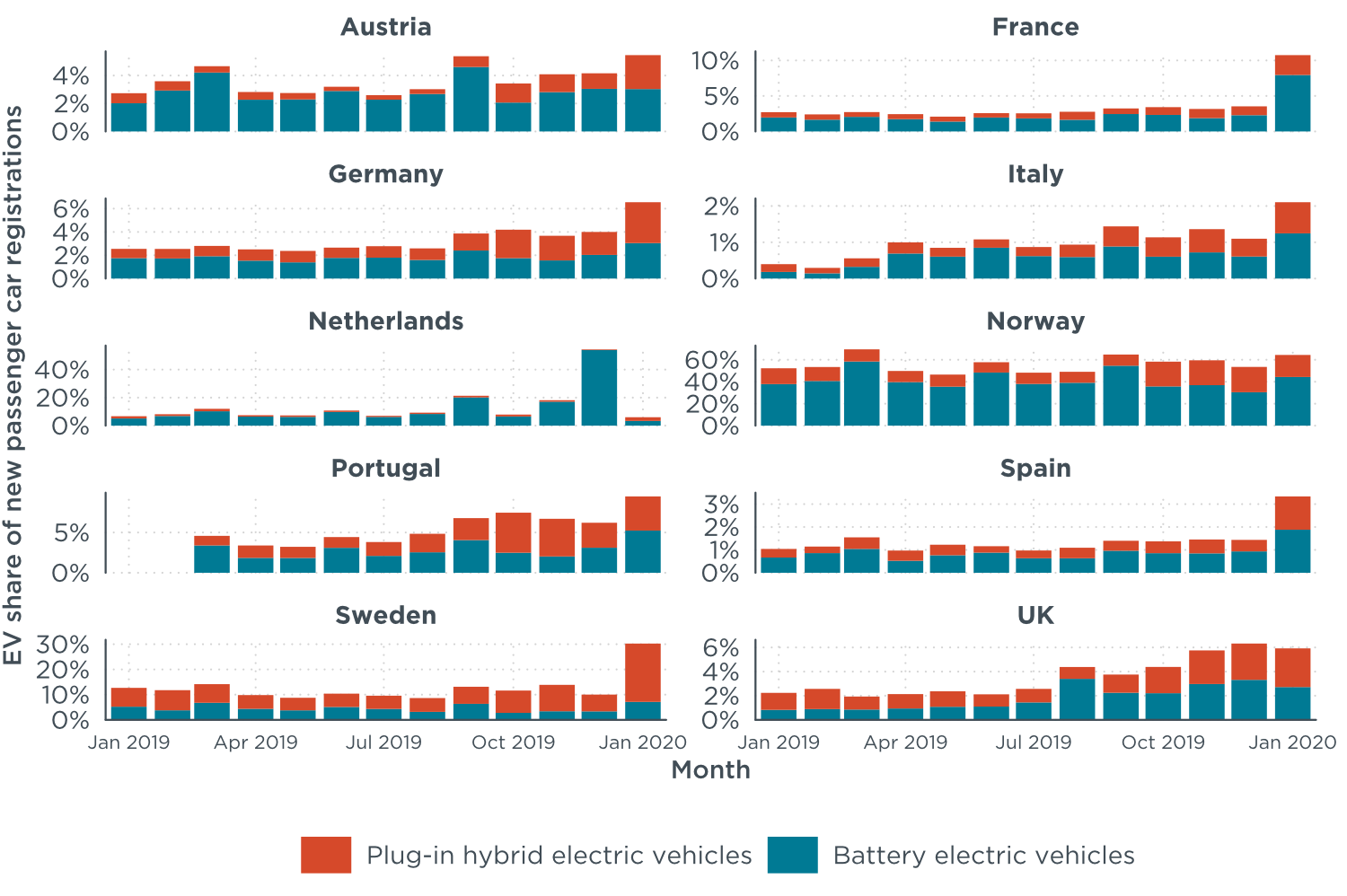

Incoming data for January 2020 seems to support these more optimistic expectations. In France, for example, the average CO2 level of new cars dropped from 113 g/km in December to 96 g/km in January—a 15% improvement within only a month’s time. This comes at a time when the average target level for manufacturers also sharply decreased from 130 g/km in 2019 to 95 g/km in 2020. Unlike in the United States, the EU vehicle CO2 standards do not set interim targets, meaning that through 2019, the 2015 target of 130 g/km for new cars was still in effect. As a result, manufacturers did not have an incentive to comply early. Instead, they could optimize their portfolio to maximize profits by, for example, selling more high-end sport utility vehicles (SUVs) with high CO2 levels in 2019 before transitioning to electric vehicles in 2020. This strategy is aided by the super-credits mechanism built into the EU regulation. In 2020, every low-emission vehicle registered counts twice towards manufacturers’ average CO2 emissions. The effect of super-credits is scaled back in the following years, and the multiplier effect is also capped for each manufacturer. Nevertheless, super-credits could have provided another incentive for manufacturers to hold back deliveries of electric vehicles until January 2020.

Another explanation for the sudden drop in fleet-average CO2 emissions is country-specific. In Europe, vehicle and fuel taxes set by each member state are a key factor in directing consumer purchase behavior, thus shaping the vehicle market. France developed a vehicle taxation system that penalizes high CO2 levels and uses the revenues to incentivize vehicles with low CO2 levels – a system referred to as ‘bonus-malus’ or ‘feebate’ taxation. As part of a reform of the French bonus-malus system, the malus for vehicles with CO2 emission levels of 185 g/km and above was raised to €20,000 starting in January 2020. In parallel, the maximum bonus for battery electric vehicles remained at €6,000. As a result, purchasing a low-emission vehicle, and in particular, a zero-emission vehicle, is now more attractive than ever. In light of these developments, it should not come as a surprise that the market share of electric vehicles increased strongly in France, from 3.5% in December 2019 to 11% in January 2020 (see figure below).

Data source: Monthly statistics from government agencies and vehicle manufacturer associations.

Similar policies to promote electric vehicle sales, which in kind lower fleet-average emissions, are evident in other European markets.

- Norway has implemented a strong vehicle tax based on CO2 and NOx emissions and vehicle weight, in addition to an exemption from VAT for electric vehicles. As a result, the electric vehicle market share remains high in the country and rose from 54% in December 2019 to 64% in January 2020.

- In Sweden, the share of electric vehicles tripled, going from 10% in December 2019 to 30% in January 2020. This is likely a result of the Swedish government transitioning to a bonus-malus-like vehicle taxation system in 2018. From January 2020 onwards, the tax is based on CO2 emission levels as measured under the new WLTP, which finds CO2 levels for combustion engine vehicles are about 20% than what was measured by the previous type-approval test.

- The Netherlands also saw a strong increase in electric vehicles registrations, jumping to a level of 54%, but this occurred in December 2019. Unlike in other countries, the share decreased in January 2020, back to a level of 6%. This is due to the fact that, until December, the taxable income for the private use of battery electric company cars was set at 4% of the vehicle’s purchase price. Starting in January 2020, this rate doubled to 8%. This is still significantly less than the 22% for all other types of cars, but notably less attractive than before.

- In Germany, electric vehicles gained in popularity, increasing from a level of 4% in December 2019 to 6.5% in January 2020. But the increase was lower than what occurred in France and other markets. Although the German government announced an increase in the cash bonus for electric vehicles from €4,000 to €6,000 as of January 2020, administrative delays in the confirmation of the increase may have caused customers to postponed electric vehicle purchases.

While the previous months have not been easy for electric vehicle enthusiasts in Europe, data from January 2020 is promising. It seems as if manufacturers are increasingly revealing their hands, not only showcasing new electric models but also marketing them in large quantities. The data for France indicates that this recent uptake in electric vehicles also has a strong effect on fleet average CO2 emission levels.

Still, the market remains fragile. There are reports about alleged delays in manufacturers’ original product plans, be it due to potential problems with battery supply, as in the case of Daimler, or issues with the battery management software, as in the case of Volkswagen. Some of the rises in sales could also be the result of a backlog of electric vehicle orders from 2019. We will only be able to determine how stable the electric vehicle market uptake really is once we have more data for 2020. So, stay tuned!

Be the first to comment