If we want to restore shared prosperity to the British economy, understanding how the public finances actually work is a key first step. This understanding flips on its head the popular understanding of the role of taxation and government borrowing, and reveals the fundamental — but understated — role that the government has in the UK monetary system.

Cross-posted from the UCL IIPP Blog

Photo by Towfiqu barbhuiya on Unsplash

The workers of the United Kingdom are once again suffering from falling real wages. This time around, wages are overwhelmed by higher costs of energy, food, and transport prices, while corporate profits are breaking records. The adverse social impact is attenuated by the preceding “lost decade” when the 2007–8 financial crisis was met with austerity policies. The resulting weak economy suppressed real wages, which only recovered their former level by 2020.

A root cause of this policy failure was the prevailing ideas of how public finances operate. Frequently this is framed in terms of a household budget, rooted in Margaret Thatcher’s claim that there is “no public money, only taxpayers’ money”. Such household analogies remain prominent in the national news media, despite the massive fiscal outlay involved with Covid-19 furlough package and health support. For example, when COVID-19 struck, the BBC asserted that the public debt is the government’s “credit card, the national mortgage, everything absolutely maxed out (…) for next few years, there is really no money.”

Two theories of public finance operations

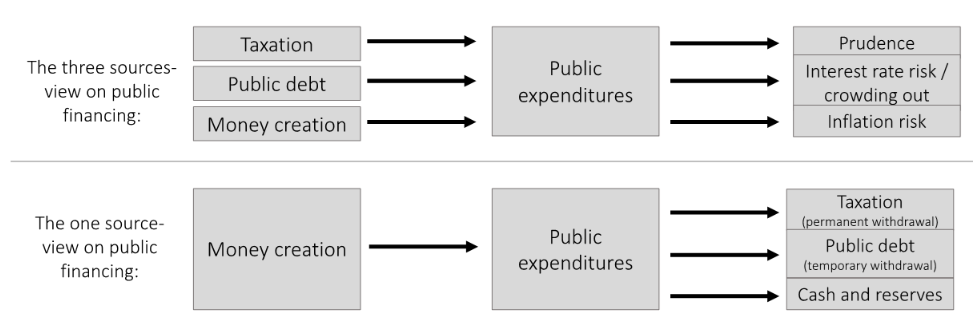

The Thatcherite perspective is reflected in mainstream economic theory’s idea of the Government Budget Constraint (GBC). In this framework, governments can obtain money for spending from three sources: taxation, public debt issuance, or money creation.

Tax financing is seen as prudent. Public debt is considered risky as more debt may lead to higher interest rates and crowd out private investment by draining a limited available pool of ‘loanable funds’. Lastly, money creation is deemed an ill-advised ‘last option’ as doing so would generate inflation (see figure 1).

Figure 1: The three-source and one-source views on the public financing process

While the UK’s economic prosperity has faltered, leading to calls for ‘levelling up’ and ‘taking back control’ with Brexit, no one has taken a deep dive in to how the UK public finances actually operate. Was Thatcher right about taxpayers being the source of UK pounds? Has the persistence of this idea been the fundamental enabler for austerity policies and the lost decade for UK workers?

An alternative perspective, championed by economists known as neo-chartalists or modern monetary theorists (MMT) is that we have gotten the sequencing in the financial system upside-down. They suggest a ‘one-source’ perspective where, after a closer look at the institutional realities, all public spending is financed by money creation.

The money created by spending ends in one of the three pots mentioned above: being permanently withdrawn through taxation; temporarily withdrawn by the issuance of public debt; or remaining in circulation in the economy. This is not an ex-ante budget constraint, but an ex-post outcome.

In our recent working paper, ‘The self-financing state’, we analyse in detail how the UK public finances operate and the government’s role in the sterling monetary system.* Through extensive analysis of legal statutes, public reports, correspondence with authorities, and Freedom of Information requests, we have arrived at a clear conclusion regarding the UK public finances: the government always finances its spending by issuing new money.

This is not an active decision to use monetary finance, as one is led to believe by the Government Budget Constraint theory. On the contrary, it is a straightforward consequence of the way the sterling monetary system has been designed and operated for at least a century and a half.

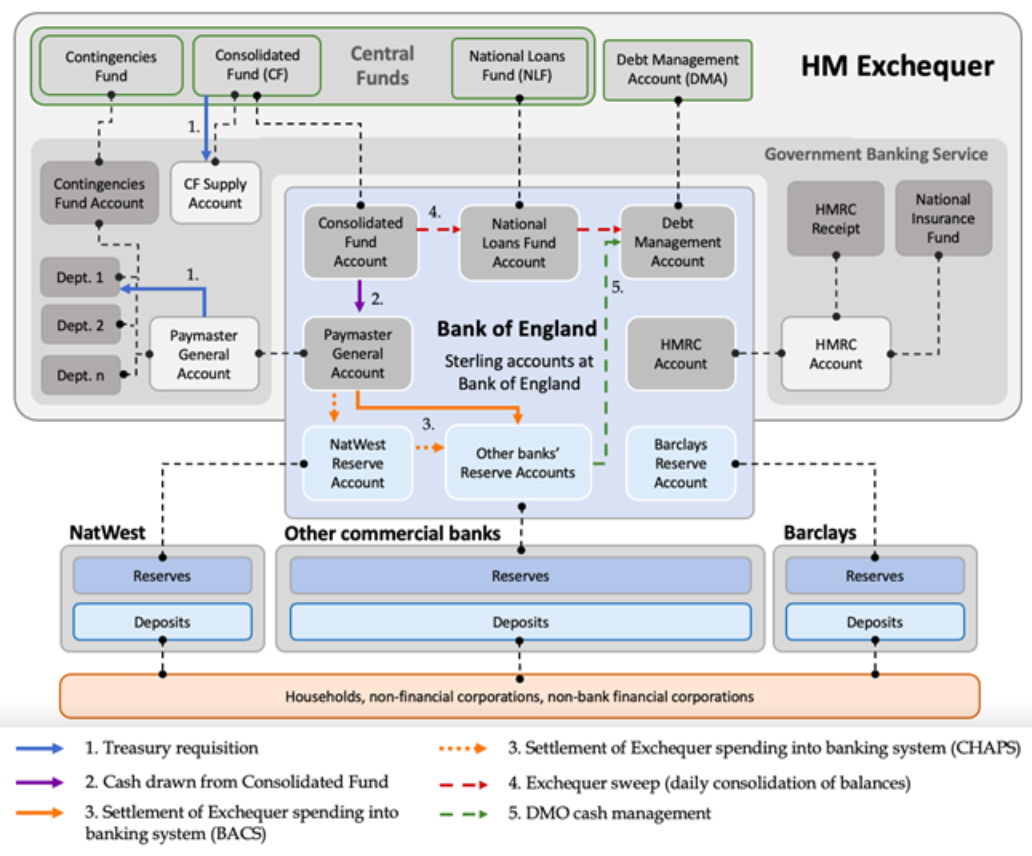

The core entity in this system is not the Bank of England but the government’s Consolidated Fund — a legal and accounting structure which was established in 1787 and is currently governed under an act of Parliament dating from 1866. This accounting entity is the main source of pounds in the UK economy. (This does not neglect that banks create pound-denominated deposits in the act of extending a loan. The Consolidated fund is the source of what is promised in these IOUs.)

How the UK government finances its spending

In this long-established system, it is standard procedure that public spending occurs in three general steps (see figure 2). When public spending is authorised via an act of Parliament, HM Treasury is permitted to lay a claim on the Consolidated Fund. When this request is verified by the Comptroller and Auditor General (an official at the National Audit Office), HM Treasury receives a ‘credit’ on the Consolidated Fund.

Such a credit legally entitles HM Treasury to order the Bank of England to make spendable balances available within an account known as the Paymaster General Supply Account (today administered within the Government Banking Service).

At this point, HM Treasury has sterling balances to spend, while the Bank of England holds a claim on the Consolidated Fund. All UK government spending arises in this manner as mandated by the 1866 Act and related legislation.

Figure 2: Public sector accounting of the expenditure process in the UK

The upshot of these arrangements is that government spending has absolutely no dependence on the existence of positive bank balances, accumulated via prior tax collection or borrowing activities. Indeed, a fundamental design feature of the UK Exchequer is that balances held are minimised and the primary accounts start each day with a balance of zero.

There is therefore never a situation where in the UK government could be said to be in danger of ‘running out of money’ or defaulting on its financial obligations. On the contrary, nothing can prevent government spending which has been authorised by Parliament from occurring, other than the express choice of the government itself.

A better public conversation

So, what does this X-ray of the public finances tell us? By paying attention to the operational realities, we concur with the one-source view of public finances. When the government spends new sterling balances into existence, the new balances remain in the system unless they are permanently taxed away or withdrawn temporarily through public debt issuance, which involves replacing pounds with longer-date debt instruments.

It then becomes immediately clear that taxation and borrowing fulfil different functions to those normally purported in relation to the provisioning of government expenditure. In particular, government debt — ultimately a claim on the Consolidated Fund — is reframed as a fundamental component of the Sterling Monetary Framework. One that is essential to the Bank of England’s monetary operations and balance sheet, an important source of collateral in wholesale money markets, and a robust store of value to pension funds. The reflexive alarmism regarding government debt that is typically observed in mainstream dialogue is severely lacking this crucial context.

There is nothing inherently inflationary in monetary financing. It is normal, and more than a decade of Quantitative Easing has essentially shown what occurs when government deficits are not reflexively matched by debt issuance: rather than consumer prices inevitably spiking and interest rates spiralling out of control, inflation was generally at or below target and interest rates fell (as intended).

From a demand-side perspective on inflation, the most important aspect is the size of the net injections of financial assets that a government deficit provides to the private sector. The income and wealth obtained from such a spending injection may increase demand and may increase prices depending on the prevailing economic context.

But the composition of these additional assets — between sterling and government debt — is a question of monetary policy and not fiscal policy. In the presence of a supply-driven inflation shock, this issue of asset composition is largely irrelevant.

This account of the institutional realities of the sterling monetary system reveals that Thatcher’s assertion about the non-existence of public money was false — and possibly a politically motivated falsehood.

We therefore do not need a return to austerity, a grand monetary reform, or even necessarily a change in how fiscal and monetary authorities interact to increase the fiscal space of the UK Treasury. We simply need a clearheaded public conversation about how to achieve shared prosperity through sustainable investments informed by how the public finances actually operate. Let’s get serious.

Support us and become part of a medium that takes responsibility for society

BRAVE NEW EUROPE is a not-for-profit educational platform for economics, politics, and climate change that brings authors at the cutting edge of progressive thought together with activists and others with articles like this. If you would like to support our work and want to see more writing free of state or corporate media bias and free of charge. To maintain the impetus and impartiality we need fresh funds every month. Three hundred donors, giving £5 or 5 euros a month would bring us close to £1,500 monthly, which is enough to keep us ticking over.

Be the first to comment