The problem is not that renewables are expensive, they’re cheaper than fossil fuels. The problem is that capitalists can’t make huge profits out of them.

Michael Roberts is an Economist in the City of London and a prolific blogger.

Cross-posted from Michael Roberts’ blog

In 2023, it was the first time in recorded history that the global surface temperature of the planet breached 2.0°C above the 1850-1900 IPCC baseline. Also more than 90% of the world’s oceans suffered heatwave conditions, glaciers lost the most ice on record and the extent of Antarctic sea ice fell to by far the lowest levels ever measured.

And last month marked a full year of record-high global temperatures, with May 2024 ranking as the warmest May on record. Earth’s ocean temperatures also set a record high for the 14th month in a row, according to data and scientists from NOAA’s National Centers for Environmental Information. According to NCEI’s Global Annual Temperature Rankings Outlook, there is a 50% chance that 2024 will rank as the warmest year on record and a 100% chance that it will rank in the top five.

The current trend of carbon dioxide emissions (the main cause of global warming and climate change) suggests that the earth’s average surface temperature will easily breach the 1.5C above the baseline target limit set by the 2015 Paris Climate Conference by the end of this decade. Indeed, without much more drastic action, CO2 emissions are heading for at least 1.8C above the baseline by the middle of this century or earlier. UN climate chief Simon Stiell said the planet was on track for a “ruinously high” rise in the global temperature of 2.7C since the industrial era.

What is to be done? There are a host of technologies being proposed to control carbon emissions and even capture existing CO2 and take it out of the atmosphere. Moreover, the drive to ‘phase out’ fossil fuel production and replace it with so-called renewables (wind, solar, hydro etc) is the rallying call from ‘the powers that be’, taken up at the last international climate conference, COP28. And clean energy investment is now nearly double fossil fuels.

But it is still not enough. Fossil fuel production is not being ‘phased out’ quickly enough and renewables are not replacing fossil fuels quickly enough. The International Renewable Energy Agency estimates that an average of 1,000 gigawatts of renewable power capacity needs to be built globally every year until 2030. But the world’s clean energy plans (and they are only plans) still fall almost one-third short of what is needed to reach that figure.

And to reach the necessary level of investment, climate finance will need to increase to about $9tn a year globally by 2030, up from just under $1.3tn in 2021-22, according to the Climate Policy Initiative.

This funding is just not coming. Rich countries finally met their target to deliver a meagre $100bn in climate finance to poorer nations in 2022 – two years later than promised. Moreover, over the past decade, public flows have driven most of the growth in climate-related transfers to poorer countries. Government aid or multilateral development bank finance almost doubled between 2013 and 2022, from $38bn to$83bn in total. But private climate finance was “stubbornly low” at just $21.9bn in 2022, according to the OECD.

And even that public funding was overstated. That is because some of the money has been taken from existing overseas aid budgets, and some of what is counted as climate finance includes funds primarily allocated to development projects such as health and education, with only tangential benefits to the climate. If all these sums are stripped out, then only $21-24.5bn of the $83bn remains as pure climate finance without strings attached, according to Oxfam in its Climate Finance Shadow Report 2023.

Why is the climate target not being met? Why is the necessary finance not forthcoming? It is not the cost price of renewables. Prices of renewables have fallen sharply in the last few years. The problem is that governments are insisting that private investment should lead the drive to renewable power. But private investment only takes place if it is profitable to invest.

Profitability is the problem – in two ways. First, average profitability globally is at low levels and so investment growth in everything has similarly slowed. Second, ironically and contradictorily, lower investment and GDP growth will slow carbon emissions expansion by reducing fossil fuel energy use. A recent study of 18 countries that managed to ‘peak and decline’ their carbon emissions in the period 2002-2015 demonstrated that one key driver of this process – accounting for 36% of the fall in emissions on average – was decreased energy use that resulted in part from ‘low growth in GDP of around 1%’ (Le Quéré et al., 2019: 215). As the GDP growth rate approached zero, absolutely decoupling growth from carbon emissions becomes more feasible (Schroder and Storm, 2020).

But on the other hand, lower renewables prices drags down the profitability of such investments. Solar panel manufacturing is suffering a severe profit squeeze, along with operators of solar farms. This reveals the fundamental contradiction in capitalist investment between reducing costs through higher productivity and slowing investment because of falling profitability.

This is the key message from yet another excellent book by Brett Christophers, The Price is Wrong – why capitalism won’t save the planet. Christophers argues that it is not the price of renewables versus fossil fuel energy that is the obstacle to meeting the investment targets to limit global warming. It is the profitability of renewables compared to fossil fuel production.

“In the case of renewables, the principal decision makers are energy companies, other developers and – in particular – the financial institutions whose decisions about whether or not to advance investment capital, and at what cost, ultimately determine whether solar and wind farm projects proceed or not. What, we might therefore ask, is the overriding question in the minds of such financiers when presented with investment proposals by renewables developers? It is the following: will I get my money back, and with an acceptable level of financial return? The basic answer to this question is, of course: only, generally, if the project is profitable.”

Christophers shows that in a country such as Sweden, wind power can be produced very cheaply. But the very cheapening of the costs also depresses its revenue potential. This contradiction has increased the arguments of fossil fuel companies that oil and gas production cannot be phased out quickly. Peter Martin, Wood Mackenzie’s chief economist, explained it another way: “the increased cost of capital has profound implications for the energy and natural resource industries”, and that higher rates“disproportionately affect renewables and nuclear power because of their high capital intensity and low returns.”

As Christophers points out, the profitability of oil and gas has generally been far higher than that of renewables and that explains why, in the 1980s and 1990s, the oil and gas majors unceremoniously shuttered their first ventures in the renewables almost as soon as they had launched them. “The same comparative calculus equally explains why the same companies are shifting to clean energy at no more than a snail’s pace today”.

Christophers quotes Shell’s CEO Wael Sawan, in response to a question about whether he considered renewables’ lower returns acceptable for his company: “I think on low carbon, let me be, I think, categorical in this. We will drive for strong returns in any business we go into. We cannot justify going for a low return. Our shareholders deserve to see us going after strong returns. If we cannot achieve the double-digit returns in a business, we need to question very hard whether we should continue in that business. Absolutely, we want to continue to go for lower and lower and lower carbon, but it has to be profitable.”

For these reasons, JP Morgan bank economists conclude that “The world needs a “reality check” on its move from fossil fuels to renewable energy, saying it may take “generations” to hit net-zero targets. JPMorgan reckons changing the world’s energy system “is a process that should be measured in decades, or generations, not years”. That’s because investment in renewable energy “currently offers subpar returns”.

The fossil fuel majors hammer this point home. The chief executive of oil producer Chevron told the Financial Times last October. “You can build scenarios, but we live in the real world, and have to allocate capital to meet real world demands.” Four out of five corporate executives considered “the ability to create acceptable returns on projects a main barrier to decarbonization of the energy system.” “We should abandon the fantasy of phasing out oil and gas and, instead, invest in them adequately reflecting realistic demand assumptions,” says Amin Nasser, chief executive of Saudi Aramco. “You can argue green all day and NGOs all day, but those are the facts. I think that message is beginning to resonate.” Liam Mallon, head of ExxonMobil’s upstream business, said.

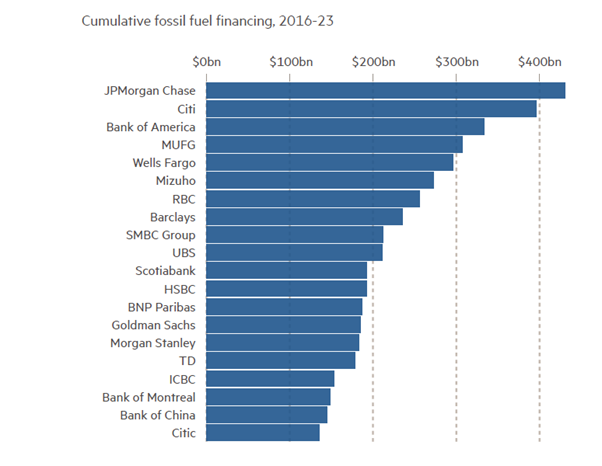

Not surprisingly we find that JPMorgan is a leading financier of fossil fuel projects. The bank underwrote $101bn of fossil fuel deals in 2021 and 2022 compared to $71bn of low-carbon deals. JPMorgan Chase, Mizuho and Bank of America were named as the biggest fossil fuel industry financers last year, in a report by climate campaigners which calculates the world’s biggest banks have provided a total $6.9tn to the sector in the eight years since the Paris climate accord.

Christophers concludes “if private capital, circulating in markets, is still failing to decarbonize global electricity generation sufficiently rapidly even with all the support it has gotten and is getting from governments, and even with technology costs having fallen as far and as fast as they have, it is surely as clear a sign as possible that capital is not designed to do the job.”

Instead, Christophers argues that if we are ever to achieve rapid reductions in carbon emissions, “extensive public ownership of renewable energy assets appears the most viable model.” I would add that must also require public ownership of the fossil fuel producers to ensure any rapid transition.

Meanwhile, the planet continues to heat up at an alarming rate.

Due to the Israeli war crimes in Gaza we have increased our coverage from five to six days a week. We do not have the funds to do this, but felt that it was the only right thing to do. So if you have not already donated for this year, please do so now. To donate please go HERE.

Be the first to comment